August 30, 2024

Dear Investor,

In the secure portal, please find the unaudited financial statements, your capital history, unrealized and realized activity report, and capital statements for the 2nd quarter of 2024. For this and all future quarterly reports, we will be following a 60-day reporting timeline.

We expect to do our next capital call at end of this month (August 2024) for ~15% of committed capital. We are currently on pace to invest in two to three more companies over the course of 2024.

We plan on hosting our Annual General Meeting virtually for our Limited Partners to meet each other, the team, and the portfolio companies. We expect this to take place on the 14th or 22nd of November 2024 to discuss the fund's performance, strategic direction, SPVs, and other notable developments. We will be sharing a save the date in the coming weeks with a detailed agenda to follow.

In reading the following portfolio company updates, please take note of the opportunity to secure your allocation in our SPVs for GenLogs and Transmutex. As our LPs, we are giving you preference before the outside interest we have received. If you would like to learn more about either of these opportunities, please reach out to Talal or Cameron directly.

Freight Intelligence Product Launch + SPV Opportunity

Highlight: Launching two full products with ~$1.6M in booked ARR in just the closed pilot phase with a growing waitlist.

Next Key Milestone: Opening Freight Intelligence Platform to the growing waitlist with opportunity to close $1M in ARR per month by onboarding 10 customers.

Next Expected Round: $10-20M Series A by Q1 2025

Background: GenLogs is a supply chain & logistics technology company that uses proprietary data + AI to track and analyze US long-haul freight in real-time. In the US, there are 27K brokers tasked with moving $1T of goods each year by placing loads from shippers on one of the 4M trucks operated by 500K individual carriers. Today, brokers attempt this market matching without the single most important piece of data for doing it efficiently: the location of each of these trucks at any point in time. Vast amounts of data are being generated by the trucking industry daily, including mobile-ad-IDs and electronic logging devices. The issue is that this data is anonymized and thus not linked to a specific truck. The same problem applies to satellite imagery and traffic camera data that only reveal the presence of a truck at a certain time and place without identifying the specific vehicle (DOT number, carrier name, etc). GenLogs has developed a proprietary approach for solving this problem scalably and without need for permission from individual truck owners. By deploying only sensors across the US to act as virtual gates, GenLogs is able to generate a distinct ID for each truck that passes a sensor that can be used to deanonymize the previously mentioned datasets. This breakthrough allows GenLogs to passively track all trucks in real-time using a fusion of disparate datasets, including satellite data, mobile ad IDs, and public traffic cameras. Using this data, GenLogs is developing best in class tools for the trucking industry.

Update: As of the end of Q2, GenLogs booked $1.6M in ARR across 14 customers with an average contract value (ACV) of $118K. These bookings were all a part of GenLogs pilot release that capped the number of customers to ensure product quality before opening the product up to their growing waitlist of customers. Their top contract is with Knight-Swift Transportation, the largest full truckload carrier service in the US, at $300K per year. GenLogs' now counts 4 of the Top 20 US truck carriers as customers as well as the 7th largest freight brokerage. GenLogs has also continued to expand its team with high quality recruits. To keep up with growing demand, GenLogs hired a head of product to speed up development - Heather Holcomb, ex-Head of Product at PayPal. They have been able to secure high quality talent at below market rates for equity compensation. Candidates have had a strong desire to join the company due to its high quality performance. With this, GenLogs was able to release two products during this quarter.

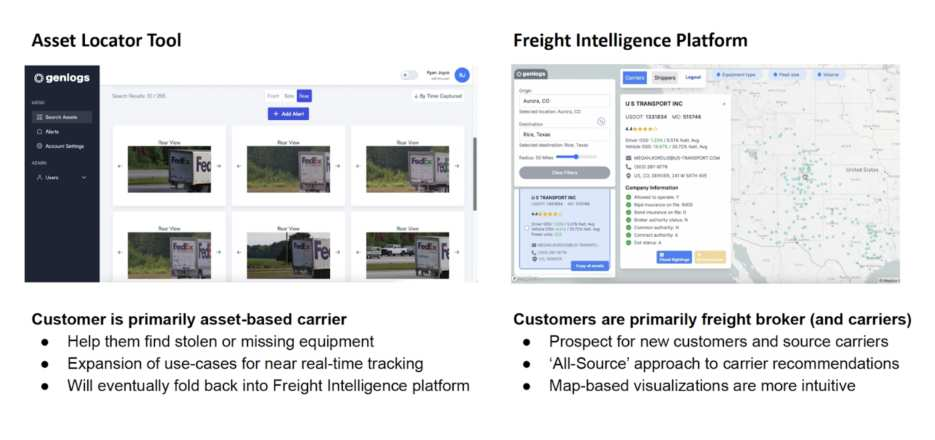

By breaking their originally planned Freight Intelligence Platform into two products, Asset Locator and Freight Intelligence, GenLogs has been able to recognize more revenue sooner and increase product pricing. The lower price Asset Locator that carriers can use to quickly identify missing and stolen equipment serves as an instant way to demonstrate the power of GenLogs' data. Within two weeks of releasing the Asset Locator, GenLogs located 36 lost or stolen trailers accounting for $1.44M of equipment. One customer has since gone on to recover $5M worth of stolen and missing equipment.

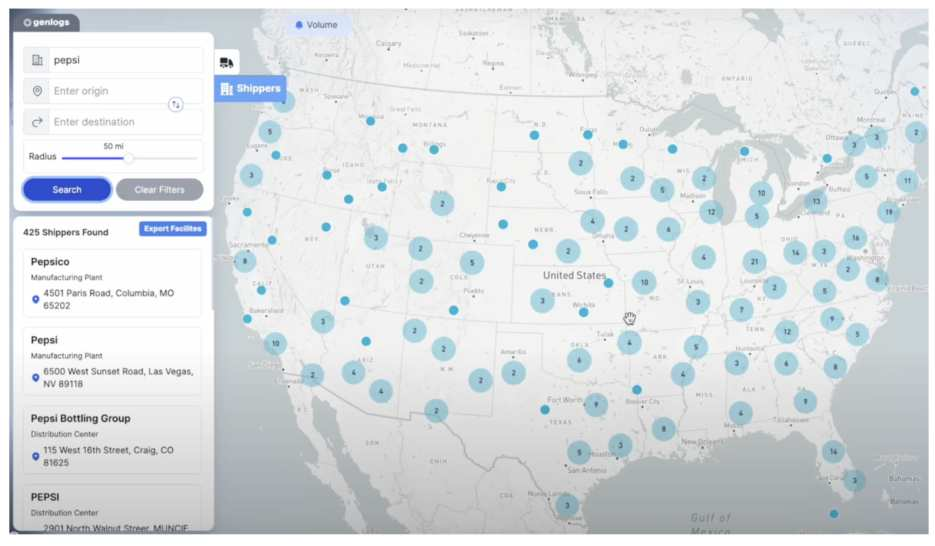

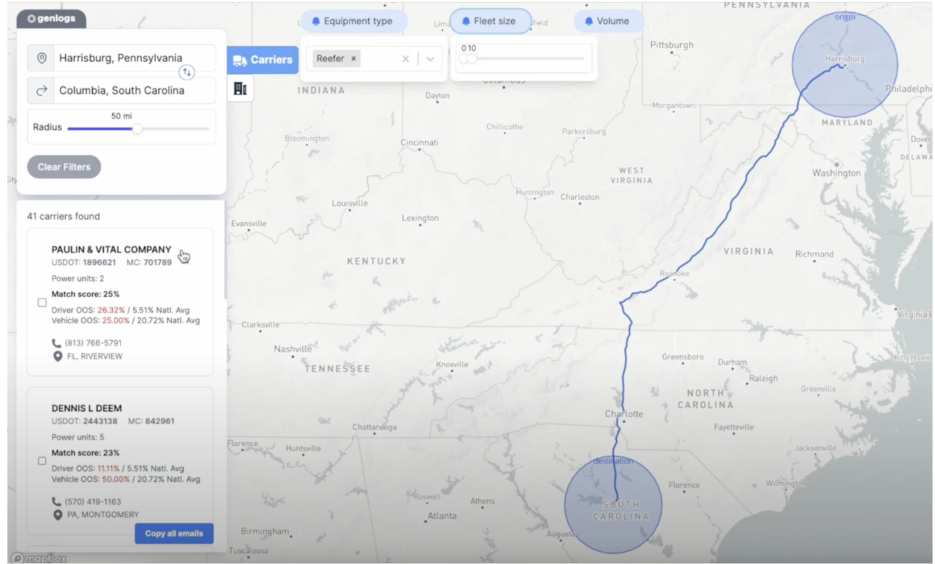

Seeing the power of GenLogs data in Asset Locator makes customers willing to quickly convert to the premium, ~$118K ACV Freight Intelligence Platform. We highly recommend watching a demo of the GenLogs Freight Intelligence Platform to understand the impact of the product. Despite leading GenLogs seed round less than a year ago, the company is already demonstrating breakout performance. Initial customer feedback shows that we should preempt the Series A raise with a term sheet to accelerate hiring and scale the product and features. GenLogs has enormous growth potential once they begin onboarding customers from their waitlist. We see a clear path for them to close $1M in ARR per month based on current ACVs and accelerate even faster the following year as they grow their sales team.

We at Steel Atlas have received immense interest from external investors and family offices to facilitate a direct investment into GenLogs. As Fund I LPs, we would like to give you priority for this Special Purpose Vehicle (SPV). If you are interested in participating, please contact Cameron or Talal immediately to secure an allocation.

Saudi Delegation Visits Geneva & LOIs with Belgium + Canada

Highlight: Signing LOI for a nuclear site in Belgium for a first-of-a-kind system potentially saving years in licensing time if final agreement is reached.

Next Key Milestone: Sign binding agreement for first-of-a-kind.

Next Expected Round: $50-200M Series B by Q2 2025

Background: Transmutex, founded in 2019 in Geneva, is reinventing nuclear energy for a safer, cleaner future. Transmutex's innovative approach addresses the core concerns associated with nuclear energy, notably waste, safety, and proliferation. Transmutex's technology is a significant advancement in carbon-free energy generation that is deployable around the world. Unlike traditional fission systems, Transmutex's system can use multiple types of fuels, including thorium, by using a particle accelerator to drive a safer, non-self-sustaining reaction. Applications of this technology are extensive including; efficiently breeding new fuel to replace uranium enrichment, enabling a new thorium-based fuel cycle for national security, burning the existing stockpile of long-lived nuclear waste to lower long term costs, and scalably producing medical radio-isotopes for cancer treatments. Transmutex has also developed simulation software with applications beyond nuclear energy.

Update: Transmutex's primary focus is securing a government commitment to lead the construction of their first-of-a-kind system (FOAK). With that, we at Steel Atlas have worked to bring Saudi Arabia to the table as a potential partner. Transmutex has been simultaneously engaging Belgium, Canada, India, and others. With these efforts, we hope to create a competitive process for the FOAK to ensure Transmutex receives the best terms possible for the system. This July, Talal led a delegation of nuclear scientists from the Saudi Ministry of Energy on a visit to Transmutex in Geneva. Transmutex's non-proliferant system is uniquely positioned to bring nuclear power to Saudi Arabia as the country has traditionally been held back by the US due to the proliferant nature of the traditional uranium fuel cycle. The delegation included the Head of Saudi Nuclear Planning, Dr. Mohammed Garwan, from the King Abdullah City for Atomic and Renewable Energy (K.A. CARE). This is the government body tasked with developing civilian nuclear energy in Saudi Arabia.

During this past quarter, Belgium's and Canada's federal particle accelerator programs (MYRRHA in Belgium, TRIUMF in Canada) LOIs to deploy Transmutex's system using their existing infrastructure and licensing. Assuming, these LOIs move forward to binding agreements under the expected terms, these would be a huge win for three key reasons:

Accelerated Licensing: The sites in Belgium and Canada are already licensed for nuclear systems. This would mean accelerating Transmutex's timeline by at least two years.

Shared Costs: These partnerships would enable for shared development costs, lowering the amount of equity financing Transmutex needs to raise.

Reusable Infrastructure: In Belgium, MYRRHA has already broken ground on the first portion of the particle accelerator. In Canada, TRIUMF already has an operational cyclotron. Both of these components can be used by Transmutex to build and test their system faster.

To fund these efforts, Transmutex plans to raise a Series B in the next 6-9 months. We are also considering a small Special Purpose Vehicle to continue to accelerate Transmutex's transition to this commercialization phase of the business. If you are interested in learning more, please reach out to Cameron or Talal.

World's First Potassium Ion 18650 Cells Delivered

Highlight: Announcing the world's first 18650 potassium ion cells with performance on track to exceed LFP cells.

Next Key Milestone: 18650 sample cell performance validated by potential customers.

Next Expected Round: $10-20M Series A by Q4 2025

Background: Group1 is commercializing potassium-ion batteries (KIBs) which are poised to become a significant player in the energy transition, offering an attractive alternative to lithium-ion batteries due to their cost-effectiveness, resource availability, and environmental benefits. Unlike traditional lithium-ion batteries, which rely on critical minerals sourced from regions of geopolitical instability, KIBs utilize potassium, a more abundant and cheaper alternative. This reduces supply chain vulnerabilities. Group1's KIBs are critical-mineral-free and "drop-in" compatible with existing LIB infrastructure, ensuring a capital efficient path to scale. KIBs are on path to having energy density on par with LFP-based LIBs, comparable cycle life, faster charging, and superior low- temperature performance.

Update: Increasing battery performance will remain the top priority for Group1. However, with Group1's announcement of the world's first18650-sized potassium-ion battery (KIB), they will begin introducing their cells to customers. Group1 expects that the initial product will be well-received by customers with supply chain concerns around lithium and a desire for improved low-temperature performance. One example of this customer type is Lockheed Martin.

Customers will be charged for these initial samples. This approach ensures that only serious inquiries are pursued, encouraging commitment to subsequent stages of collaboration. These initial contracts will allow Group1 to continue to improve cell performance while scaling their manufacturing capabilities, which is currently at 1 ton of cathode material per year. This incremental process is needed to meet the requirements of the large automotive OEMs. Group1 announced the world's first 18650 KIB cell at one of the marquee battery conferences called "Beyond Lithium", hosted for the 14th time by Oak Ridge National Labs. Per Alexander Girau, CEO of Group1, "this innovation represents years of dedicated research and product development. By distributing samples to our partners among Tier 1 OEMs and cell manufacturers, we are paving the way for widespread adoption of this transformative technology."

The 18650 form factor is the most widely used cell format. Group1's new 18650 batteries use commercially available graphite anodes, separators, and electrolyte formulations, enabling an easier path to scale relative to other chemistries, such as sodium-ion. Group1's cells offer superior cycle life and excellent discharge capability, operating at 3.7V. This release exceeds our initial performance expectations and demonstrates a practical path to achieving a gravimetric energy density of 160-180 Wh/kg, which is standard for LFP-LIB used by the automotive industry. In our last quarterly update, we indicated that Group1 would be pursuing a $20M Series A. After an initial set of conversations with investors, this process has been put on hold so that Group1 can demonstrate the commercial viability of its cells.

Wins Grant from US Department of Defense

Highlight: Winning a $175K grant competition within the US Department of Defense and thus securing sole source contracting capabilities for key Navy construction projects.

Next Key Milestone: Close multiple contracts for Type 2 structures including from the DoD.

Next Expected Round: $10M+ Series A by Q3-Q4 2025

Background: Hedral is an AI structural engineering firm based in New York that enables real estate developers to build faster, cheaper, and with lower environmental impact. Today, Hedral is already the most efficient structural engineering firm in the world, delivering stamped drawings and 3D building models to developers 10x faster than legacy firms. Hedral's core technology automates the creation of the drawings and models that takes traditional firms weeks to months to produce manually. This is positioning Hedral to roll-up the fragmented, multi-hundred billion dollar market for construction design and engineering.

Update: After closing an oversubscribed Seed round led by Silicon Valley veteran, Vinod Khosla of Khosla Ventures, Hedral has made product development improvements and begun negotiating contracts with the US Department of Defense (DOD). The DOD is looking for AI-driven solutions to optimize building design across disciplines, codes, and site conditions to save time and money for their domestic base build outs. The US DOD's National Security Innovation Network (NSIN) recently held a competition to identify potential technology providers. Not only did Hedral win first prize and $175,000, Hedral will now be able to win sole-source contracts (i.e. contracts without a bidding process) from the DOD. From the NSIN announcement:

Hedral's solution edged out the others with an approach based on generative AI and advanced computational geometry and physics. The solution not only automates design work while optimizing cost and constructability — taking into account the metrics required by the challenge — but also produces more accurate cost models. This approach delivers unprecedented productivity while minimizing costly mistakes and requests for information and change orders that can emerge downstream in the design process. The goal is be able to execute real-time adjustments across multiple disciplines—foundation, architecture, structural, mechanical, and electrical engineering—by considering factors like local codes, site conditions, and historical designs to expedite design exploration, develop optimized design solutions in terms of cost, schedule, and performance, and produce more accurate cost models," explained Mark Edelson, Program Executive Officer for Industrial Infrastructure.

Going forward, Hedral will negotiate sole source contracts from the US Navy through the Program Executive Officer for Industrial Infrastructure (PEO II). PEO II is the executive responsible for cost, schedule, and performance of the Navy's $21B effort to integrate facilities, utilities, and industrial plant equipment investments to meet nuclear fleet maintenance requirements. This represents a significant long-term revenue opportunity for Hedral. Hedral plans to focus on Type 2 structures, also known as non-combustible construction. Type 2 structures are often used for simple but expensive builds like data centers, warehouses, and government buildings. Although this is where Hedral has seen the most success to date, they also recently booked projects retrofitting offices into hotels and designing large complex skyscrapers in the Middle East. Until now, Hedral has been operating in stealth (without marketing their services or technology). However, with the DOD announcement Hedral is already receiving enough inbound that they are preparing a self-serve version of their internal tooling. The first tool will allow potential customers to immediately get an estimate of Hedral's work to see the massive cost difference between them and legacy players. We expect this to expedite Hedral's sales process going forward.

This quarter, we took a significant step forward in growing the presence of Steel Atlas within the industrial technology ecosystem. We not only received exclusive press coverage of our Fund I announcement in the Wall Street Journal, we were also featured live on Bloomberg TV and had a long form interview with Forbes.

Furthermore, we grew the team for the first time since inception by bringing on two venture partners from top funds in climate and industrials to expand our footprint to the West Coast (SF / LA) and Europe. On the West Coast, Alex Laplaza was a Partner and the first-hire at Lowercarbon Capital where he raised and deployed $2 billion into clean energy. In Europe, Brett Bivens joins us having most recently been the Head of Research at Daniel Ek's (CEO & Founder of Spotify) billion dollar European industrial incubation firm, Prima Materia.

Although these venture partners have brought increased qualified deal flow to the firm, we did not deploy capital into any new investments this quarter. There are several reasons for this. First, we believe in being patient capital given the long-term nature of venture investing. Second, given our high level of concentration (total number of investments per fund) compared to other investors at our stage, our investments decisions carry an outsized level of conviction relative to our peers. Third, we believe in constantly raising the bar and our top portfolio companies are setting a high standard. However, given the strength of our current pipeline, we expect to make at least one new investment in Q3 and overall remain on pace in terms of deployment for Fund I.

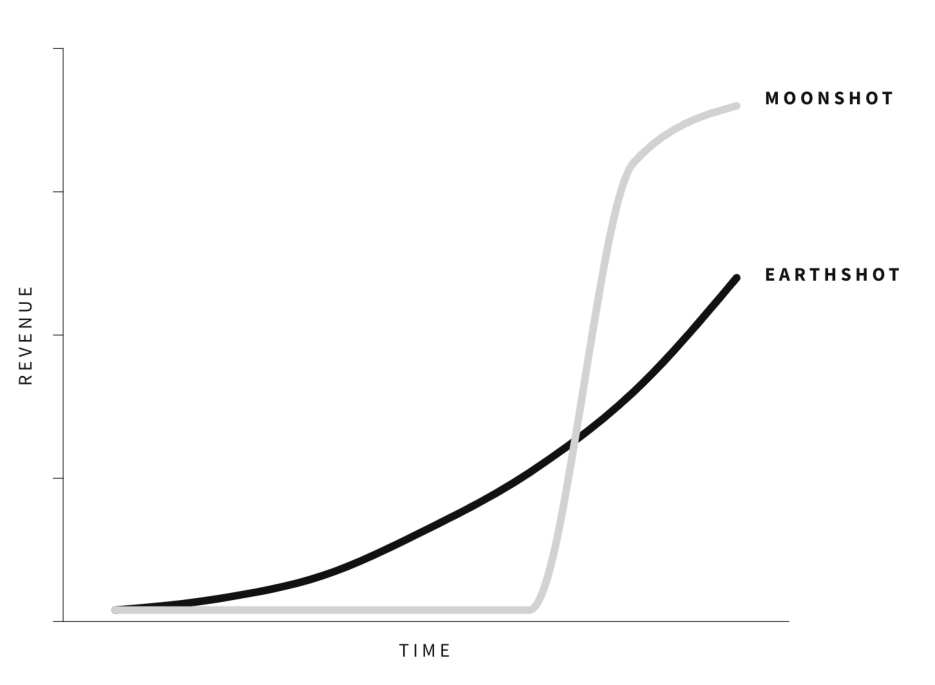

As per the individual company updates above, we are pleased to see how the portfolio is maturing and we believe it is beginning to validate our portfolio construction thesis. We are already seeing the benefits of portfolio concentration. Given GenLogs' strong traction and our large position in the company (12.68% of the total fund), we believe that with the coming Series A, we will make significant progress towards the ~8x multiple required for our unrealized gains in GenLogs to exceed our total fund size. We recognize that there is still a long journey ahead to realize those gains. However, near-term progress in "Earthshot" companies like GenLogs gives us the confidence to make bold investments in "Moonshot" companies, like Transmutex. These Moonshots have the potential to drive long-term outlier performance for the fund. With this, we are excited to continue to pursue a balanced portfolio of these two types of business, one of the core tenants of our portfolio construction strategy. To dive deeper, please read our memo on Earthshots and Moonshots.

Whether it is an Earthshot or Moonshot, when we identify a breakout company in the portfolio, it is our goal to create opportunities for you to continue to participate via SPVs. In the next two quarters, we expect to make the first of these SPV opportunities available to you for GenLogs and Transmutex. Beyond giving you access to competitive deals via our pro-rata, executing on these SPVs allows us to bring in new strategic capital from our network to support our portfolio companies as well as continue to maintain a strong voice with the company as it grows. We believe that the strong relationships fostered via this strategy with later stage founders will have ancillary benefits for the firm. Not only do these founders become deal flow attractors for the firm, strong association with them further positions us as experts in our domain. We saw this first hand with Transmutex this quarter where we were invited for a live interview on Bloomberg to discuss the effects of the 2024 US Presidential Election on nuclear energy deployments.

As discussed in the interview, we maintain that nuclear energy will continue to see strong bipartisan support as demonstrated by the passing of the ADVANCE Act. However, the nature of that support will vary depending on whether Trump or Harris is elected. We expect a Trump administration to prefer deregulation whereas a Harris administration would likely increase incentives for nuclear investment. Taking a step back, the effect of the US Election on nuclear energy provides an archetype for how we try to position our investments with regard to macro political events. Our top priority is to get the major trend right. These are trends that play out on decade-long time scales and see support from both ends of the political spectrum even if that support takes different forms (deregulation vs incentivization). The redeployment of nuclear energy at scale is just one example of this. Another major trend is the friend-shoring of critical mineral supply chains. The long term bipartisan support for these trends helps to insulate investments in these spaces from macro political shocks. We also find that the intersection of these trends can be fertile ground for seemingly contrarian investment opportunities. One example of this is carbon negative/neutral hydrocarbon fuel synthesis. Climate awareness and acceptance of climate change is monotonically increasing. At the same time, we continue to exceed "peak oil" predictions. Although it may seem counterintuitive, we expect both of these trends to remain in place.

OPEC sees no peak oil demand on horizon, more crude needed to fuel global economy. Climate change is an increasingly significant source of volatility that will drive support for decarbonization. A natural assumption would be that decarbonization will go hand in hand with electrification, thus leading to peak oil. We disagree with that. Long-chain hydrocarbons are exceptional at moving energy through time and space (even relative to our most advanced batteries). With trillions of dollars of infrastructure and markets already established for hydrocarbons, we expect continued global growth to lead to increased demand for hydrocarbons even as electrification moves forward. Given that, we see an enormous opportunity in finding a way to produce long-chain hydrocarbons cheaper than with fossil fuels without contributing to (and ideally while negating) greenhouse gas emissions. Excitingly, we believe there are companies today combining nuclear energy with hydrogen synthesis, carbon capture, and fuel production that could unlock this trillion dollar opportunity. We look forward to sharing more on this and other opportunities emerging from the major trends shaping our world in the coming quarters.

Onwards and upwards,

Cameron & Talal

Steel Atlas General Partners