November 27, 2024

Dear Investor,

In the secure portal, please find the unaudited financial statements, your capital history, unrealized and realized activity report, and capital statements for the 3rd quarter of 2024. This and past quarterly updates were completed on 60-day reporting timelines. Going forward, we plan to move to 30-day reporting.

For planning purposes, we expect to do our next capital call near the end of this month (December 2024) for ~15% of committed capital. We are currently on pace to invest in three more companies through Q2 2025 at which point we will be fully deployed out Fund I. This update also includes information on our latest investment, Valar Atomics.

Finally, we hosted our Annual General Meeting virtually for our Limited Partners to meet the portfolio companies and reflect on our first full year together. We discussed the fund's performance, strategic direction, and other critical matters. A video recording of the full AGM is available here.

Please note that the numbers reflected in this update are different than what was presented in the AGM (hosted in Q4) as this is Q3 reporting.

Real-Time Freight Intelligence

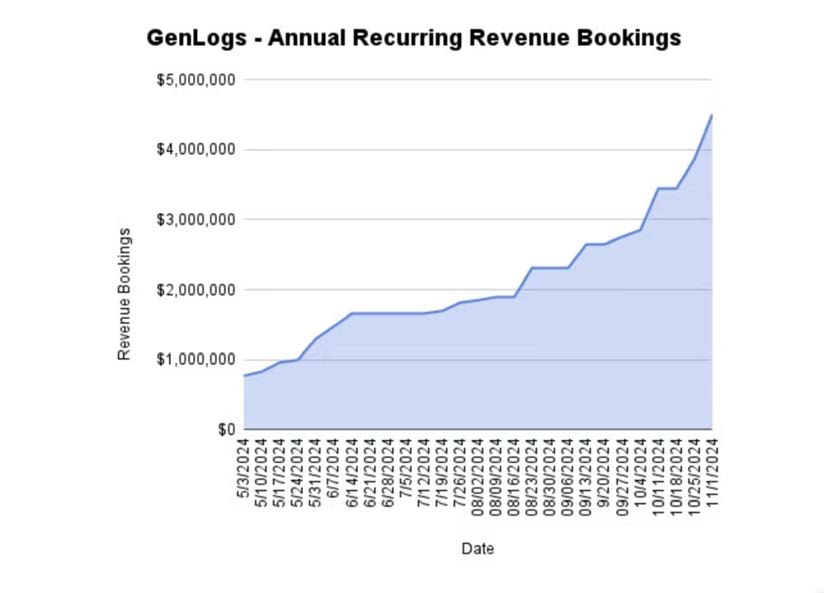

Highlight: $2.75M in booked ARR + 100% pilot customers converted to paid.

Next Key Milestone: Open the waitlist to customers and capture pent up demand ($1M in inbound pipeline per week) + close $10M Series A.

Next Expected Round: $20M Series B by Q1 2026.

Background: GenLogs is a supply chain & logistics technology company that uses proprietary data + AI to track and analyze US long-haul freight in real-time. In the US, there are 27K brokers tasked with moving $1T of goods each year by placing loads from shippers on one of the 4M trucks operated by 500K individual carriers. Today, brokers attempt this market matching without the single most important piece of data for doing it efficiently: the location of each of these trucks at any point in time. Vast amounts of data are being generated by the trucking industry daily, including mobile-ad-IDs and electronic logging devices. The issue is that this data is anonymized and thus not linked to a specific truck. The same problem applies to satellite imagery and traffic camera data that only reveal the presence of a truck at a certain time and place without identifying the specific vehicle (DOT number, carrier name, etc). GenLogs has developed a proprietary approach for solving this problem scalably and without need for permission from individual truck owners. By deploying only sensors across the US to act as virtual gates, GenLogs is able to generate a distinct ID for each truck that passes a sensor that can be used to deanonymize the previously mentioned datasets.

This breakthrough allows GenLogs to passively track all trucks in real-time using a fusion of disparate datasets, including satellite data, mobile ad IDs, and public traffic cameras. Using this data, GenLogs is developing best in class tools for the trucking industry.

Update: As of the end of Q3 (September 30th), GenLogs booked $2.75M in ARR across 14 customers with an average contract value (ACV) of $120K. These bookings were all a part of GenLogs' pilot release that capped the number of customers to ensure product quality before opening the product up to their growing waitlist of customers. Every single pilot customer converted to a paid contract upon renewal. Thirteen customers are still in the waitlist waiting to be onboarded. There is new pipeline of $8.5M with ACVs of $124K also waiting to be serviced. This inbound continues to be strong with zero dollars spent on marketing. They will hire a Head of Sales, Kris Forrest, to help Ryan service the heavy inbound. GenLogs onboarded 50 initial freight brokerage users from 10 pilot customers in the last week of July. GenLogs has since grown the number of users within those pilot customers by over 10x within six weeks. Over 38% are daily active users with average session times over 12 minutes multiple times per user per day. This is driving high Net Promoter Scores. Given the usage, all pilot customers immediately converted to annual contracts.

GenLogs' roster of customers with signed contracts and LOIs continues to grow each week with some of the top companies in the freight supply chain. Werner's CIO recently gave the platform high praise and many have said it's like brokering freight "in god-mode." As for the sensor deployment, GenLogs has already paid down 70% of their Phase I Trident sensors (140 sensors). Their internal financial model has GenLogs with no projected out-of-cash date. Chief Strategy and Product Officer Blake Balch has hired a full Sensor Deployment Team to focus on securing key real estate for the sensors. This includes a field technician crew (with another onboarding in next quarter). Head of Product, Heather Holcomb (ex-PayPal) completed preparation for the integration of the GenLogs API with transport management systems (TMS). This is designed to provide the power of Freight Intelligence Platform directly within customer workflows and internal systems. We believe the greatest lift here is the ability to seamlessly access carrier and shipper recommendations within their TMS and CRM systems. Lastly, GenLogs quietly and quickly closed a highly competitive Series A for $10M. We will discuss this in greater length during our Q4 update.

Reinventing Nuclear Energy

Highlight: German Federal Government Pre-empting Series B.

Next Key Milestone: Sign binding agreement for first-of-a-kind.

Next Expected Round: $30M Series B by Q1 2025.

Background: Transmutex, founded in 2019 in Geneva, is reinventing nuclear energy for a safer, cleaner future. Transmutex's innovative approach addresses the core concerns associated with nuclear energy, notably waste, safety, and proliferation. Transmutex's technology is a significant advancement in carbon-free energy generation that is deployable around the world. Unlike traditional fission systems, Transmutex's system can use multiple types of fuels, including thorium, by using a particle accelerator to drive a safer, non-self-sustaining reaction. Applications of this technology are extensive including; efficiently breeding new fuel to replace uranium enrichment, enabling a new thorium-based fuel cycle for national security, burning the existing stockpile of long-lived nuclear waste to lower long term costs, and scalably producing medical radio-isotopes for cancer treatments. Transmutex has also developed simulation software with applications beyond nuclear energy.

Update: During this past quarter, Belgium's federal particle accelerator programs, MYRRHA, signed an LOI to deploy Transmutex's system using their existing infrastructure and licensing. This follows intense dialogue with Canada's equivalent program, TRIUMF. Transmutex has spent several weeks working out the details of the LOI with TRIUMF. It will entail a demonstration of the irradiation of their fuel in a lead-cooled system using a particle accelerator.

This is key because TRIUMF operates the second most powerful cyclotron in the world after the Paul Scherrer Institute (PSI) in Switzerland (Transmutex's design partner). This agreement is important because Canada is a nuclear nation. TRIUMF is a fully licensed nuclear facility in which we could build a scaled down but fully functional version of our system for $150–250M. TRIUMF stated this could happen by the end of 2029 as they don't foresee the need for a full nuclear license since the system is sub-critical.

The German Agency for Disruptive Innovation, SPRIND, is paying Transmutex €200K for a techno-economic study of nuclear waste transmutation in Germany. Their partners in the study are the Technical University of Munich Business School for economic analysis and the Industrial Safety Agency of northern Germany, TÜV NORD, for the technology evaluation. Transmutex will provide the technical performance data, as well as a profile of the nature of the waste that has been stored on location in the ISSAR nuclear plant (now decommissioned). Nuclear waste is always evolving due to elements spontaneously transforming themselves through radioactive decay. Determining the evolution of the matter in the waste over time and the resulting concentration of the different radio-toxic elements are essential for any techno-economic analysis. Transmutex's analysis systems and software are game-changer for countries like Germany that are trying to assess their nuclear waste management needs. In conjunction with this study, SPRIND has decided to invest at least €5M in equity and agreed to be a reference for any other interested party. SPRIND can invest outside of Germany if there is an industrial interest for their country, which is the case here via the waste study mentioned. They invest €250M annually and financed fusion companies for €60M last year. We expect SPRIND to be strong partner in funding the Transmutex going forward.

Additionally, ARPA-E published a $40M request for proposal for "Nuclear Energy Waste Transmutation Optimized Now (NEWTON)". Transmutex successfully submitted and received pre-approval. With this, Transmutex is in the process of partnering with US national labs, universities, and companies to submit the full approval. Transmutex had submitted a response to ARPA-E's request for information last year, and the NEWTON proposal is very closely related to Transmutex's priorities: accelerator reliability, target material, and the business case for the system. The Swiss government will also officially sponsor Transmutex for the IAEA review of their system to designate them as non-proliferant. Transmutex would be the only nuclear reactor company in the world to do so. Additionally, Transmutex has signed with the PSI in Switzerland for the fabrication of Thorium fuel pellets using a novel and patentable technique which could dramatically reduce the price of fuel and ensure its non-proliferance.

Critical Mineral-Free Batteries

Highlight: Generated sample requests from over 20 major companies.

Next Key Milestone: 18650 sample cell performance validated by potential customers.

Next Expected Round: $10M-20M Series A by Q4 2025.

Background: Group1 is commercializing potassium-ion batteries (KIBs) which are poised to become a significant player in the energy transition, offering an attractive alternative to lithium-ion batteries due to their cost-effectiveness, resource availability, and environmental benefits. Unlike traditional lithium-ion batteries, which rely on critical minerals sourced from regions of geopolitical instability, KIBs utilize potassium, a more abundant and cheaper alternative that, reducing supply chain vulnerabilities. Group1's KIBs are critical-mineral-free and "drop-in" compatible with existing LIB infrastructure, ensuring a capital efficient path to scale. KIBs are on path to having energy density on par with LFP-based LIBs, comparable cycle life, faster charging, and superior low-temperature performance.

Update: The product release has sparked a strong increase in customer engagement across multiple sectors. Group1 is now actively collaborating with several key OEMs and cell manufacturers, with a focus on power tools, powersports, and automotive markets. These engagements demonstrate the growing demand for KIB technology and underline our potential to become a key player in the battery industry. This increased engagement comes from two Tier 1 cell manufacturers (ATL and Samsung SDI) and three leading OEMs in beachhead markets (power tools and powersports from Yamaha Motors, Stanley Black & Decker, and TTI). They have also attracted significant attention from legacy automotive OEMs (Stellantis, Ford, Daimler) looking for electrification solutions. Group1 has also completed Phase 1 of a multi-phase joint development agreement (JDA) with Orbia Fluor and Energy Materials, showcasing KIB's role in a resilient domestic supply chain. They also completed an NSF SBIR/STTR Phase 1 grant in partnership with UT-Austin and are transitioning into Phase 2 ($1.25M) over the next 12 months. They are engaging UT-Austin's Discovery to Impact team for support through their "UT bridge to Phase 2 Support Grant." If successful, this will result in $30,000 to make their SBIR Phase 2 proposals more competitive. Letters of support from key customers like Ford, Stellantis, Siemens, ATL, Samsung SDI, Yamaha, and more will be critical for future commercial agreements and validating their market position.

AI-Enabled Structural Engineering

Highlight: Crossed $800K in booked revenue.

Next Key Milestone: Repeatable sales playbook and funnel in data center and logistics space.

Next Expected Round: $10M-15M Series A by Q1 2026.

Background: Hedral is an AI structural engineering firm based in New York that enables real estate developers to build faster, cheaper, and with lower environmental impact. Today, Hedral is already the most efficient structural engineering firm in the world, delivering stamped drawings and 3D building models to developers 10x faster than legacy firms. Hedral's core technology automates the creation of the drawings and models that takes traditional firms weeks to months to produce manually. This is positioning Hedral to roll-up the fragmented, multi-hundred-billion-dollar market for construction design and engineering.

Update: Hedral has further established its position as a leader in automating design and construction processes. Hedral has now refined its product to address a specific growing segment in the market (data centers and logistics facilities) where their automations provide the most leverage. The company's tech-enabled service model has proven effective in an industry historically resistant to automation. Hedral's ability to rapidly iterate on design constraints and generate build-ready outputs has caught the attention of data center developers and the DOD. Furthermore, the product itself has seen substantial advancements, moving from partial automation (~30-40%) to a level that includes fine-grained engineering details such as rebar mesh configuration. This jump enables Hedral to tackle traditionally labor-intensive tasks in minutes rather than weeks. This evolution positions Hedral to capitalize on increasing demand for efficiency in construction while significantly reducing costs and timelines. This is driving their bookings of $800K in revenue as of the end of Q3.

Net-Zero Fuels via High-Temperature Gas Reactors

Highlight: Signing agreement with the Philippines for a JV.

Next Key Milestone: Demonstration of thermal reactor for sulfur-iodine cycle by Q2 2025.

Next Expected Round: $30M+ Series A by Q3 2025

Background: Valar Atomics is pioneering a breakthrough in energy by combining proven High-Temperature Gas Reactor (HTGR) technology with a novel business model to create synthetic, net-zero fuels. Led by Isaiah Taylor, an autodidact and serial entrepreneur, and supported by Chief Nuclear Officer Mark Mitchell, a leading expert in TRISO-fueled reactor design, Valar's integrated approach removes traditional barriers to large reactor-deployments via a business model that enables single-sites with hundreds of reactors. With the potential to disrupt both energy and industrial sectors in need of high temperature heat, Valar is poised to deliver clean, competitively priced synthetic fuels at scale — unlocking a trillion-dollar opportunity in the global energy market.

Update: Valar Atomics is leveraging High-Temperature Gas Reactors (HTGRs) to create cost-effective, carbon-neutral fuels and industrial processes. Their model bypasses traditional nuclear barriers by integrating reactor manufacturing and synthetic fuel production within single industrial "Gigasites." This centralized approach minimizes regulatory complexity, reduces costs, and positions Valar to supply net-zero fuels at prices competitive with fossil fuels. By targeting high-temperature industrial heat and synthetic fuel markets, Valar aims to decarbonize hard-to-electrify sectors such as steel, cement, and petrochemicals, which contribute nearly a third of global emissions.

The company's reactor design uses TRISO fuel and proven HTGR technology to produce heat exceeding 850°C, crucial for hydrogen production and industrial processes. This heat enables hydrogen production via thermolysis using the sulfur-iodine (SI) cycle. At scale, Valar will be able to reach unprecedentedly low costs for hydrogen at under $1/kg. This clean hydrogen can then be combined with captured CO₂ and used as inputs to the Fischer-Tropsch process to produce net-zero synthetic fuels (diesel, jet fuel, and gasoline). These fuels offer superior performance and environmental benefits compared to fossil fuels, while remaining cost competitive.

Valar's vertically integrated business model avoids the common pitfalls of selling nuclear reactors to third parties, such as utilities, which face entrenched preferences for established light water reactor designs. Instead, Valar plans to scale reactor production within its own facilities, reducing licensing overhead by concentrating reactor deployments to sell fuel at scale on the open market. This strategy mirrors successful integrated models like SpaceX's where instead of selling rockets, SpaceX sells payload capacity and internet access. Furthermore, Valar's modular scaling and "power uprates" approach allow gradual development and testing, reducing risks associated with reactor design, process integration, and licensing.

The company's leadership team is led by Isaiah Taylor and nuclear expert Mark Mitchell. Taylor's clear vision and drive combined with Mitchell's expertise in HTGR and TRISO fuel design provide the foundation for Valar's technical and operational success. Their joint venture in the Philippines exemplifies their global ambitions and ability to navigate the regulatory challenges inherent to the nuclear industry. We believe that they will be the fastest company to get a nuclear reactor online. Valar's technology, market strategy, and leadership collectively position the company to redefine energy production and industrial decarbonization. With a potential to disrupt trillion-dollar markets and mitigate climate change, Valar represents a significant opportunity for investors. Its scalable Gigasite model, coupled with advancements in reactor technology and synthetic fuel production, offers a pathway to sustainable and profitable energy solutions on a global scale.

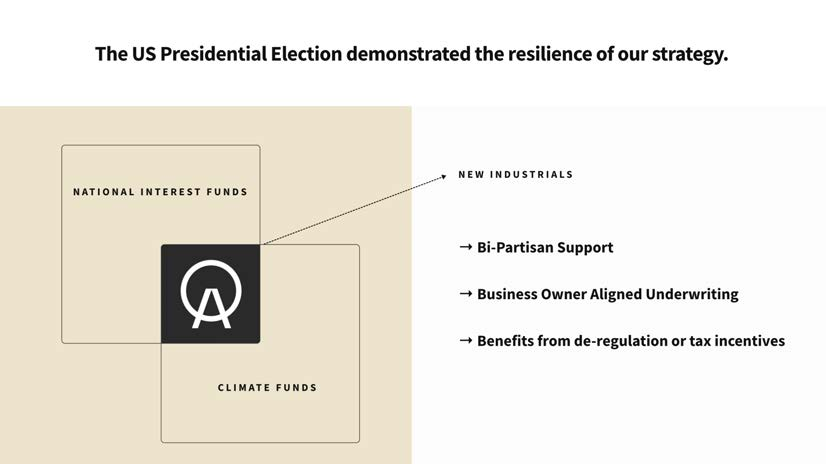

A Contrarian Approach

In our recent AGM where we dove deep on the fund's best in class performance, heard from the CEOs where they shared why they chose Steel Atlas over multibillion-dollar AUM firms, analyzed why our strategy is anti-fragile in shifting political environments, and announced our Fund II, we want to use this section to share our most contrarian learnings as fund. Given we covered a lot of topics we would normally write about here during the AGM, we instead want to focus on sharing the answer to a question we recently received from an LP because it highlights how Steel Atlas is structured to drive outperformance. The question was, "what contrarian views do you have on running a VC fund that very few other people share?"

Before answering what our contrarian beliefs on running a VC fund are, we need to clarify why being contrarian is (potentially) valuable. You do not want to be unnecessarily reinventing the wheel. Rather, where you choose to operate differently from the market needs to be driven by a testable hypothesis that doing so will directly drive differentiated performance. With this fund, we had the following hypotheses:

Contrarian Hypotheses

1/ Funds are over-diversified. If you believe in the quality of your picking and your ability to affect the outcomes of your investments, you should only invest in 8-12 companies per fund at the seed stage. It has been shown that increasing your portfolio size from 10 to 20 companies only increases your probability of returning a 5x fund by 0.3% (from 9%) and comes at the cost of less time and resources to both identify / underwrite investments and support portfolio companies once those investments are made. If you have high conviction, you should concentrate.

2/ Large, "bottom-heavy" and "platform-wide" teams are overrated. Small teams are better positioned to make strategy changes as the market evolves (like a speed boat vs cargo ship). Furthermore, if you need to hire junior investors to write investment memos or to reach conviction as a partner, you should not be investing in that company. Finally, partners should have direct relationships with founders, using their network to support portfolio companies versus outsourcing that to less experienced and well networked platform teams.

3/ Being exclusive and private with your theses is underrated. As blogs and social media grew in popularity over the last decade, VC firms have used these platforms to build audiences and share where they are investing publicly. We write a lot but share most of it privately. We believe it's better to have the 100 most important people in your sector read what you write every time than have an audience of 100,000 lower quality followers. Sharing our theses privately makes them more valuable to those 100 people that matter most. They will then reciprocate by sharing private information and opportunities with us.

4/ Share your investment memos with founders and other VCs. Most funds keep their investment memos private (which is somewhat ironic given (3)). We believe you should write long-form, in-depth investment memos even when you are not leading because it helps you win deals (not necessarily because it improves underwriting). By sharing investment memos with the founder prior to investing, it allows them to send it to other VCs. Not only does this demonstrate our expertise to founders, it ingratiates them to us when other investors use our memo to invest. This is especially notable when the memo is of higher quality than the lead or much larger firms.

We are excited to report that these initial hypotheses are being validated as we speak. Below is some of the evidence:

Evidence for Hypotheses

1/ Funds are over-diversified. Our concentrated approach has allowed us to maintain a slower pace of investment (one per quarter) than most funds, which enables more thorough, research driven underwriting. Not only does this underwriting lead to higher quality decisions it also directly supports (4). Furthermore, due to our concentration of Fund 1, with positions representing ~12% of the total fund size, we are quickly driving outperformance relative to the market with our markups.

2/ Large, "bottom-heavy" and "platform-wide" teams are overrated. VC is a relationship business and people prefer interacting with general partners rather than junior team members, whether on the investment or platform side of the business. For example, we have been able to drive outcomes with government bodies like the Saudi Ministry of Energy, even though we are a team of two. Furthermore, we are able to pivot our focus quickly when needed to capitalize on emerging opportunities, whether that is into magnet manufacturing or steel making. Communication and execution is fast and seamless.

3/ Being exclusive and private with your theses is underrated. We believe in quality over quantity. Sharing our research exclusively first (even if we open it up to a broader group later), has enabled us to develop close relationships with GPs at "Tier 1" funds like USV where we co-led a round last year in Transmutex.

4/ Share your investment memos with founders and other VCs. Our most recent investment in Valar Atomics is the perfect case study here. If you have not already, please watch this testimonial from the CEO of Valar Atomics where he outlines why he chose us over other firms and how he was surprised to see "Tier 1" funds relying on our investment memo to make their decisions.

We believe it is only through the judicious and iterative process of developing and testing these contrarian hypotheses that we can build a firm whose differentiation drives durable outperformance. As we continue to build and grow Steel Atlas, expect us to share more of these learnings. Thank you as always for your support on this journey.

Onwards and upwards,

Cameron & Talal

Steel Atlas General Partners