January 15, 2025

Dear Investor,

In the secure portal, please find the unaudited financial statements, your capital history, unrealized and realized activity report, and capital statements for the 4th quarter of 2024. For all future quarterly reports, we will be following a 30-day reporting timeline from the end of each quarter.

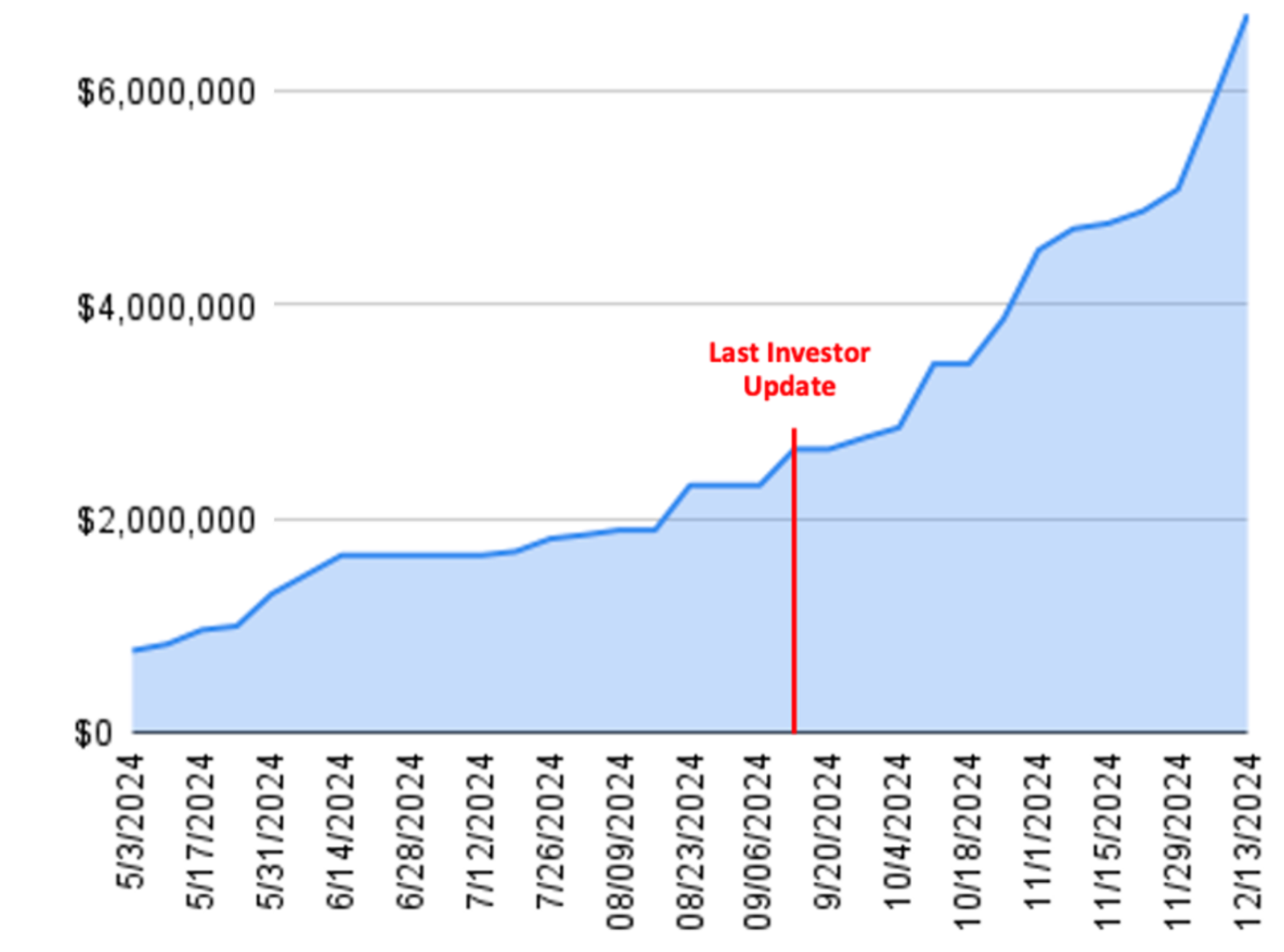

We are extremely proud to report that, due to our GenLogs markup, we are now sitting at 2.17x TVPI. This is considered better than the top 5% of venture capital funds in our vintage. More details to specifics below, but we are nonetheless humbled by the marking of early outperformance that most funds wish to have.

For planning purposes, we expect to do our next capital call near the end of March 2025 for ~12.5% of committed capital. We are currently on pace to invest in three more companies through the end of Q2 2025 at which point we will be fully deployed out Fund I.

Starting Q1 2025, we will also be migrating our fund administration from Aduro Advisors to Hanover Park (an AI native fund administrator). Our goal with this move is to continue to improve the firm while minimizing operating costs to ensure as much committed capital as possible flows into investments.

Finally, we are expecting Transmutex to raise a Series B in Q2 2025. Like with GenLogs, we will be making our pro-rata available to our LP base. Although we are not requesting commitments at this moment, we would like to ensure you have ample time for consideration.

A supply chain & logistics technology company using proprietary data + AI to track and analyze US long-haul freight in real-time.

Highlight: $7M in booked ARR (up from $2.5M in Q3) + $14M @ $100M valuation Series A.

Next Key Milestone: Service the $22M in pipeline + launch real-time carrier tracking feature.

Next Expected Round: $20M Series B by Q1 2026.

In the US, there are 27K brokers tasked with moving $1T of goods each year by placing loads from shippers on one of the 4M trucks operated by 500K individual carriers. Today, brokers attempt this market matching without the single most important piece of data for doing it efficiently: the location of each of these trucks at any point in time. Vast amounts of data are being generated by the trucking industry daily, including mobile-ad-IDs and electronic logging devices. The issue is that this data is anonymized and thus not linked to a specific truck. The same problem applies to satellite imagery and traffic camera data that only reveal the presence of a truck at a certain time and place without identifying the specific vehicle (DOT number, carrier name, etc).

GenLogs has developed a proprietary approach for solving this problem scalably and without need for permission from individual truck owners. By deploying sensors across the US to act as virtual gates, GenLogs is able to generate a distinct ID for each truck that passes a sensor that can be used to deanonymize the previously mentioned datasets. This breakthrough allows GenLogs to passively track all trucks in real-time using a fusion of disparate datasets, including satellite data, mobile ad IDs, and public traffic cameras. Using this data, GenLogs is developing best in class tools for the trucking industry.

Update: As of the end of Q4 (December 31st), GenLogs booked $7M in ARR (up 280% from $2.5M at the end of Q3). In Q4, GenLogs had the following growth metrics:

- Employees 95% increase

- Customers 167% increase

- Users on Platform 591% increase

- Sensors Deployed 137% increase

While the GenLogs had not planned to raise a Series A until Q1 2025, a number of preemptive offers on top of strong traction and exuberant user feedback caused us to reconsider this course of action. The day before Thanksgiving, we closed GenLogs' Series A. The round was led by Venrock and HOF Capital at a $100M post-money valuation. This is a large markup from our initial investment leading the seed round at a $12M post and our follow-on at $25M post. Averaged out, we are now at 5.5x on our position in GenLogs. Our concentrated portfolio construction strategy means that this performance generates significant lift in our total fund multiple which sits at 2.25x at the end of Q4 2024.

Throughout 2024, GenLogs had been largely operating in stealth mode. This changed the week of Thanksgiving when it was announced that GenLogs would help recover all stolen/missing assets for the entire freight industry for free (with the caveat that GenLogs could market the results/logos of users). Over the last four months, GenLogs has helped recover over 400 assets for massive companies like DB Schenker, Knight-Swift, Werner, and Pepsi. A combination of news articles and podcasts helped their active pipeline swell to over $22M with accelerating bookings. They still have put $0 into growth marketing and yet just crossed $7M of revenue booking. GenLogs is on track to be cash-flow positive in Q2 2025. Sales cycles are still below 30 days and ACVs have risen to $140K.

To finish Q4 2024, GenLogs signed two of the largest shippers in the United States (Walmart & Pepsi) as well as the largest commercial auto insurers (Progressive & GEICO). This validated that the TAM for GenLogs is much larger than the $100B+ freight brokerage industry. In total, GenLogs has 50 signed enterprise customers.

GenLogs is Series A capital to build a sales team, expand engineering, and accelerate sensor deployment. There are a finite number of locations that are ideally suited for truck-tracking sensors. GenLogs' is snatching them up on exclusive decades-long leases. GenLogs will 4x their number of sensors over this next year as they also expand into Mexico. The firm is also hiring a small team to begin servicing DoD and other Federal customers. Their data is poised to combat the trafficking of guns, fentanyl, and humans. On that last point, the team is partnering with Polaris to leverage GenLogs' data to combat human trafficking in the trucking industry.

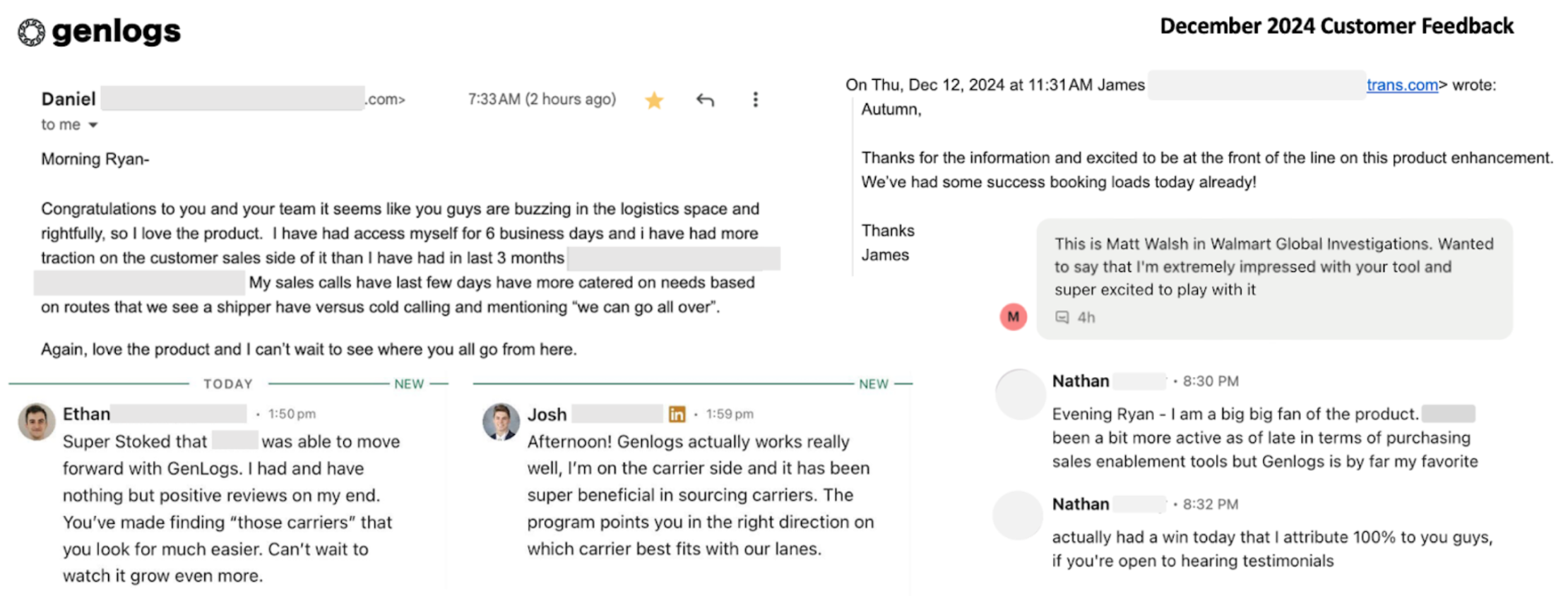

While their Net Promoter Score (NPS) remains high, the explosive growth has resulted in a deluge of user-generated feature requests which has pushed their Customer Success and Product teams to the limit. Their Engineering team has had to balance platform stabilization and maturation with prioritization of key 'must have' features. GenLogs biggest challenge is filling roles in engineering and data science fast enough in order to meet these requests. That being said, customers are excited as shown below:

It goes without saying, 2024 was a breakout year for GenLogs. Given that, we wanted to pass along some words directly from GenLogs CEO, Ryan Joyce:

"We end this year having surpassed $7M in sales.

- We have signed 50 customers to our platform, with an ACV of over $140K.

- We have expanded beyond freight brokers to service shippers, carriers, and insurers.

- Our nationwide sensor network now collects 40K images of trucks every 5 minutes.

- Our team grew from 3 to 30+ employees.

- We closed a Series A this month valuing the company at $100M.

These are impressive metrics for any first-year SaaS company, but for a hardware-enabled SaaS company, they are almost unheard of. GenLogs now operates the largest sensor network in the world that exclusively tracks commercial vehicle patterns. In a recent memo, Steel Atlas wrote about 'data gusher' businesses made possible via AI and sensors – and GenLogs is leading the vanguard. We have coined the term 'high-margin hardware' to explain the role that our sensors play in collecting valuable data, which we further refine with our native AI to deliver extraordinary value to our customers. The scale of data we are collecting is staggering.

As the leading IoT and fleet tracking provider to the commercial vehicle industry, Samsara has a $25 billion market cap – yet only has 7% market share. This means that they are only tracking about 23,000 trucking fleets – and their privacy policy prevents the attributable sale of this data. On the other hand, GenLogs has now collected data on over 200,000 trucking fleets and we have full unrestricted use of the data. Samsara's relatively small market share is emblematic of a larger trend in the transportation industry: extreme fragmentation."

Reinventing nuclear energy for a safer, cleaner future by transmuting nuclear waste.

Highlight: LOI & MOU signed with Los Alamos National Lab and Tata Consulting Engineering respectively.

Next Key Milestone: Sign binding agreement for first-of-a-kind + close Series B.

Next Expected Round: $30M Series B by Q3 2025

Transmutex, founded in 2019 in Geneva, is reinventing nuclear energy for a safer, cleaner future. Transmutex's innovative approach addresses the core concerns associated with nuclear energy, notably waste, safety, and proliferation. Transmutex's technology is a significant advancement in carbon-free energy generation that is deployable around the world. Unlike traditional fission systems, Transmutex's system can use multiple types of fuels, including thorium, by using a particle accelerator to drive a safer, non-self-sustaining reaction. Applications of this technology are extensive including; efficiently breeding new fuel to replace uranium enrichment, enabling a new thorium-based fuel cycle for national security, burning the existing stockpile of long-lived nuclear waste to lower long term costs, and scalably producing medical radio-isotopes for cancer treatments. Transmutex has also developed simulation software with applications beyond nuclear energy.

Update: In our last update, we described the $40M ARPA-E request for proposal for "Nuclear Energy Waste Transmutation Optimized Now (NEWTON)". Transmutex successfully submitted their proposal in collaboration with the renowned Los Alamos National Laboratory (made famous by the Manhattan Project / Robert Oppenheimer). This proposal is to transmute the US nuclear waste stockpile within 30 years. This ARPA-E proposal specifically mentions subcritical systems using proton accelerators like Transmutex's design. Our contacts at Los Alamos wrote to us that they were unaware of any "credible company" in the US focusing on the transmutation of waste.

To secure the relationship with Los Alamos, Transmutex has established a U.S. subsidiary. This subsidiary will enable Transmutex to win ARPA-E funding as well Department of Defense contracts. Although we cannot reveal too much at this time, we recommend reading a recent article in the NY Times on the $1.7 trillion project for renewing the US nuclear strategic arsenal. The plutonium from US nuclear war heads is waste that requires remediation. We expect to receive confirmation on ARPA-E funding for Transmutex in Q1 2025.

Furthermore, we believe the US will sign a collaboration agreement with India on nuclear technology, freeing the way for full cooperation. This would be a major breakthrough for Transmutex as its work to kick start the thorium fuel cycle in India gains momentum. Similarly we believe Saudi Arabia will reach a nuclear agreement of some kind with the US under the Trump administration sometime in 2026, and as you know, we are very well positioned there.

With this, Transmutex signed an MOU with Tata Engineering Consultancy in India (TCE), making them the first advanced reactor company to do so. The Indian Department of Atomic Energy recommended their partnership. For context, Tata is the EPC for all of India's nuclear reactors. India's goal is to 30x nuclear energy to 300 GWe, which would require 30GWe of TMX START systems to fuel their heavy-water reactors with Transmutex's U233. The reason for this is that India has no sovereign enriched uranium fuel supply. The areas of work with TCE are studies on the fuel cycle, site selection and evaluation, experimental planning, and engineering developments. TCE has proposed to seek funding from international organizations, such as the World Bank, or the Asian Investment banks, for some of their planned early studies.

In Germany, the report commissioned by SPRIN-D (German federal innovation arm) on German nuclear waste, done together with the Technical University of Munich, will be published on Feb 18th, a week before the German government elections. With this, it is looking more and more likely that Transmutex will be the key to restarting German nuclear energy.

In Canada, Transmutex is expected to have a full technical meeting at the federal research lab for nuclear and particle physics, TRIUMF, by mid-March, to plan for a scale down demonstrator that would be operational by 2029. The new federal elections in Canada will probably bring the conservatives in power which will be positive for nuclear and therefore also for Transmutex's project.

Commercializing potassium-ion batteries, a critical-mineral-free alternative to lithium-ion batteries.

Highlight: Generated sample requests from over 20 major companies.

Next Key Milestone: 18650 sample cell performance validated by large potential customers.

Next Expected Round: $10-20M Series A by Q4 2025

Group1 is commercializing potassium-ion batteries (KIBs) which are poised to become a significant player in the energy transition, offering an attractive alternative to lithium-ion batteries due to their cost-effectiveness, resource availability, and environmental benefits. Unlike traditional lithium-ion batteries, which rely on critical minerals sourced from regions of geopolitical instability, KIBs utilize potassium, a more abundant and cheaper alternative. This reduces supply chain vulnerabilities. Group1's KIBs are critical-mineral-free and "drop-in" compatible with existing LIB infrastructure, ensuring a capital efficient path to scale. KIBs are on path to having energy density on par with LFP-based LIBs, comparable cycle life, faster charging, and superior low-temperature performance.

Update: Current conversations with customers are progressing through the technical validation phase. ATL, the world's largest cell manufacturer by volume and the maker of all iPhone batteries, has become deeply interested in Group1's IP. They are conducting internal testing and evaluation of the 18650 KiB cells with the following three options upon successful evaluation:

- Direct investment.

- JDA to make KIBs with Group1 supplying them with KPW (cathode material).

- JV in the US to make KIBs and Group1 supplies the KPW to the JV.

While testing began in Nov 2024, we expect to receive the earliest results from their evaluation by the end of Q1 2025. Following our last update on Group1's JDA with Orbia, one of the largest battery material suppliers in the US (electrolyte materials), Group1 received $100k in revenue from the Phase 1 with the goal of establishing a domestic supply-chain for electrolyte and graphite towards KIB. Group1 and Orbia are currently defining the scope for Phase 2 of the JDA that should amount to $200k in revenue. We expect this to also occur by the end of Q1 2025.

Group1 is also in talks with Eve (third largest cell manufacturer in China) for a JDA/contract. They are currently negotiating the terms for testing and validating the cells. The outcomes of these successful evaluations match those for ATL. The key gating factor here is safety in the production process and during disposal of the KIB cells. Lastly, Stellantis, the world's fourth largest auto OEM, is interested in finding a joint project to match KIB with one of their automotive platforms. We are aiming for an MOU with Stellantis by the end of Q2 2025.

Overall, Group1 has continued to exceed their technical milestones for cell performance. However, the company needs to secure at least one of the previously mentioned large customers in Q1/Q2 2025 to put the company in a strong position to raise a Series A.

An AI structural engineering firm enabling real estate developers to build faster, cheaper, and with lower environmental impact.

Highlight: Crossed $2M in booked revenue (up from $800K in Q3).

Next Key Milestone: Secure US Army contracts for bases via OTAs.

Next Expected Round: $10M Series A by Q4 2025.

Hedral is an AI structural engineering firm based in New York that enables real estate developers to build faster, cheaper, and with lower environmental impact. Today, Hedral is already the most efficient structural engineering firm in the world, delivering stamped drawings and 3D building models to developers 10x faster than legacy firms. Hedral's core technology automates the creation of the drawings and models that takes traditional firms weeks to months to produce manually. This is positioning Hedral to roll-up the fragmented, multi-hundred billion dollar market for construction design and engineering.

Update: Hedral secured a US Navy contract alongside another Air Force contract via Phase I SBIRs. This is in addition to the marine base design contract first discussed in Q3. Arjo (CEO) is leading his team to form a coalition for sole source contracts through Other Transaction Authorities (OTAs). An OTA is a procurement authority that allows federal agencies to enter into agreements with non-traditional defense contractors, such as small businesses. OTAs allow agencies to bypass certain Federal Acquisition Regulation (FAR) requirements to speed up the acquisition process and make it more flexible.

Additionally, Hedral has secured its first Middle Eastern contract through a large developer in the UAE. There are several other non-DoD opportunities in the US that have converted into bookings such as an upstate New York developer as well as several data center opportunities that match Hedral's target building characteristics. These datacenter projects have been supported by co-investors like Khosla and Valar. Hedral has a strong cash position to last them another 20 months at current burn.

Pioneering a breakthrough in energy by combining proven HTGR technology with a novel business model to create synthetic, net-zero fuels.

Highlight: Signing agreement with the Philippines for a JV.

Next Key Milestone: Demonstration of thermal reactor for sulfur-iodine cycle end of Q1 2025.

Next Expected Round: $30M+ Series A by Q3 2025

Valar Atomics is pioneering a breakthrough in energy by combining proven High-Temperature Gas Reactor (HTGR) technology with a novel business model to create synthetic, net-zero fuels. Led by Isaiah Taylor, an autodidact and serial entrepreneur, and supported by Chief Nuclear Officer Mark Mitchell, a leading expert in TRISO-fueled reactor design, Valar's integrated approach removes traditional barriers to large reactor-deployments via a business model that enables single-sites with hundreds of reactors. With the potential to disrupt both energy and industrial sectors in need of high temperature heat, Valar is poised to deliver clean, competitively priced synthetic fuels at scale — unlocking a trillion-dollar opportunity in the global energy market.

Update: The next key milestone for Valar Atomics is demonstrating the non-nuclear version (called Ward Zero) by the end of Q1 2025. As such, the team has been heads down building their first thermal reactor at their new facility in El-Segundo, CA. Valar Atomics goal is to be the world's fastest company to bring a nuclear reactor online. They are currently targeting 2026 for their Ward One reactor. To achieve this, they have secured a strong partner in the Filipino government. Valar has signed a Coordinated Research Project (CRP) this year to begin licensing and site selection, as well as engaging with potential Gigasite customers. They are also in talks with the Philippine Nuclear Research Institute (PNRI) and stakeholders in the legislature to create a TRISO fuel fabrication facility for their reactors.

In parallel with rapid development in the Philippines, we have begun to approach potential commercial and regulatory partners in the United States. Valar is currently in dialogue with the Chief of Staff of the Air Force about procurement pathways for a 5MW system capable of producing JP-8 (jet fuel) at forward deployed locations.

Valar is also under NDA with Dominion Energy about a potential Gigasite buildout at Mount Storm, WV. The government of West Virginia is actively supporting their efforts to find favorable Gigasite locations due to a large volume of carbon from coal plants. Finally, West Virginia University is considering Valar's proposal to co-develop Navatar One, the world's first commercial Sulfur-Iodine cycle for hydrogen production.

In 2015, Philip Tetlock and Dan Gardner released a book called Superforecasting: The Art and Science of Predicting the Future. I (Cameron) read this book when I was a pro-soccer player in MLS trying to figure out what big trends I should bet my next career on. Like most people who read the book, I wanted to learn how to become better at predicting the future like the "superforecasters" it follows — ordinary people who, through skillful habits and rigorous methodology, achieve extraordinary accuracy in their predictions. If I could predict the future, I could plan the optimal long-term career move.

Despite this book's popularity, what I actually learned is that it should be titled Superforecasting: Lessons On Making Useless Predictions. The reason for this is simple: the book claimed that predicting the "big picture", broad and long-term trends, was not feasible because of deep, unknowable, variables. Thus these superforecasters (none of which were great investors) focused entirely on one week to one year predictions with quantifiable outcomes. Although at the time of reading, I could at best be called a 22 year old novice investor, one thing was clear to me — a common characteristic of great investors is that they invest on longer time horizons than their peers. See the below quote from Warren Buffet on using no less than a five year time horizon …

Thus the real gripe I have with this book is that it pushes its readers to fall into a trap that I see many of our peers falling into — focusing on predicting the waves and not the tide. Early stage venture capital is a long term game with decadal time horizons. The short-term quantifiable predictions are waves on the surface of water: individually interesting but in isolation ultimately inconsequential. What you really want to know is the direction of the tide. The tide is made up of many waves that in aggregate will ultimately determine if you get pulled out to sea or end up happily on the beach. Although many things have changed since I was sitting in the locker room reading this book to figure out my future career, one thing has definitely remained — I am far more interested in the tide than the waves.

So how do you get a feel for the tide (especially in these times of increasing volatility)? One of our favorite techniques for pulling the tidal signal from the noise is bringing together a diverse set of intelligent individuals and using them as human wind (tide?) vanes. To do this, we host dinners where to attend a guest must provide a set of relative predictions (ie. rank a list of predictions from most likely to least likely). The rest of the dinner is spent debating the predictions.

To kick off the year, we travelled LA and SF to host a series of dinners with some of our favorite human wind vanes. Attendees included representatives from some of the world's top family offices (Emerson Collective aka Steve Jobs FO / Franklin Templeton FO), sovereign wealth funds (Sanabil / PIF), mega-venture-funds (a16z / Lightspeed), deep tech funds (Cantos), climate funds (Voyager), founders, and political actors (ie. advisors to the Trump transition team). We asked these leaders to rank the following from most likely to least likely to occur in 2025:

Rank these from most likely to least likely to occur in 2025 …

• A peace treaty ending the war in Ukraine

• A new hot war involving US troops breaks out

• A top AI company (OpenAI, Anthropic, X AI, etc) raises a down round

• A top AI company releases model the market deems AGI

• Israel and Saudi Arabia normalize relations

• A new reactor design is licensed by the NRC

• Alphabet's market cap is larger than Apple's

• Bitcoin ends the year above $100K

• Waymo market share exceeds Uber in SF

The rules of these dinners precludes us from revealing the specific predictions of individuals, however, we want share a few insights that demonstrate how relative prediction ranking and can reveal the underlying tides of the time. What will happen with AI?

By including multiple contradictory predictions regarding the same topic (a top AI company raises a down round vs a model is deemed AGI), we are able to gain a more nuanced view of the tides (after all it takes two points to make a line). In this case, there was significant divergence across the attendees on AI. People were reluctant to believe that a top AI company would raise a down round this year, however this was because "structure" could be added to deals to ensure valuations were maintained. It was recognized that the ability for companies to distill models (eg. DeepSeek style) and serve them cheaply posed a threat to the longterm commercial viability of foundation model companies' current spend on new model development. The sustained valuations for OpenAI, Anthropic, X AI is ultimately predicated on the belief that AGI is possible with unfathomably large upside for those that get their first due "take off" where models recursively self-improve using synthetic data. Across the board, Apple's was expected to remain a winner by avoiding the high capex of making models while capturing the value of them via their proprietary distribution on iPhone, iPads, etc.

The Tide – The definition of AGI is a moving goal post that market still views as achievable. AGI will not be defined by a specific metric on a test but rather as a moment in time when models pose a credible threat to US labor en masse. There is light undercurrent of skepticism that AGI is achievable (including one large investor provocatively claiming OpenAI is a zero). The key trend is that access to intelligence will get cheaper and more energy will be required to make it possible as more people will want access to cheaper and better intelligence, regardless of whether it is considered AGI.

Should you buy bitcoin today?

Bitcoin ending the year above $100K was among the most common most likely predictions. This was predicated on the possibility of a federal Bitcoin reserve. However, we see reason for pessimism. Although, everyone predicted it above $100K, no one admitted to buying Bitcoin today despite their optimism. The natural question should be, "who is the marginal buyer?"

The Tide – Bitcoin has gone mainstream. The next domino to fall is the US government formally taking a position. If this does not occur in the next year, expect this market cycle to unwind.

Should you short Uber?

Of all the predictions, whether Waymo would exceed Uber's market share in downtown SF was the most popular point of conversation. If you removed the "in 2025" portion of the portion of the prediction and extended it to ~2027, there was near unanimous agreement that Waymo would exceed Uber (so much so that a 10 year Uber employee recently sold all of their vested shares this year). However, attendees from LA were more bullish on Waymo's near term prospects than those that lived in SF. This was driven by geographic constraints and rate fleet scaling (both factors that we believed are solvable).

The Tide – Autonomous vehicles are coming, meaning ~7% of US jobs are in the cross hairs. We believe an under-discussed implication of this is what happens to auto insurance markets. Will this be the canary in the coal mine for insurance markets broadly as AI and robotics touch more industries?

Are we on the precipice of peace?

People view Trump as the president for peace. Nearly universally, a new hot war involving US troops was ranked as the one of the least likely predictions. Economic implications led many to predict a normalization of Isreal and Saudi relations. However, it is more likely this occurs in 2026 when this could provide a big win for Trump just prior to the US mid-term elections

The Tide – Expect the resolution of existing conflicts and de-escalation of the remaining (despite potential trade wars and extreme rhetoric). Business considerations will dominate foreign policy.

Are new US nuclear reactors coming?

There was a divergence in views between those that have invested in or founded nuclear reactors companies and those that have not. The fascinating aspect of the divergence was that those with the least experience in the space were most bullish on a new reactor being licensed in 2025. The practical aspect of changing regulatory policy and licensing regimes kept experienced attendees cautious about 2025 but extremely bullish in the years to come. We will have some exciting news to announce soon on a legal challenge to the US Nuclear Regulatory Commission that we have supported over the past year.

The Tide – The nuclear energy winter is over and support is becoming mainstream. We will see more nuclear companies get funded despite the fact that the best investments will have already been made over the last three years when this trade was not obvious.

The above is just one of our methods for doing our job as early stage investors — that is avoiding being distracted by all the waves in order to ride the tide of new technologies, capturing value via our investments. As Elad Gil noted in 2020, many of the best venture investments are "indexes" on these technological tides. SpaceX indexes the value of all space companies via launch. Coinbase indexes the value of all crypto companies via market making. Our portfolio already consists of companies that we think have the potential to index some of the most important tides of today. Transmutex can provide fuel and manage waste for all nuclear reactors. GenLogs can provide a source of truth for the entire freight-industry. As we round out Fund I, expect more companies that ride the tide and index its value.

Onwards and upwards,

Cameron & Talal

Steel Atlas General Partners