May 15, 2025

Dear Investor,

In the secure portal, please find the unaudited financial statements, your capital history, unrealized and realized activity report, and capital statements for the 1st quarter of 2025. For all future quarterly reports, we will be following a 45-day reporting timeline from the end of each quarter.

For planning purposes, we expect to do our next capital call mid June 2025 for ~12.5% of committed capital. We are currently on pace to invest in 1 more companies through the end of Q3 2025 at which point we will be fully deployed out Fund I. We expect to begin deployment out of Fund II, a $50M vehicle starting in Q4 2025.

As a reminder, we have migrated our fund administration to Hanover Park (an AI native fund administrator). Our goal with this move is to continue to improve the firm while minimizing operating costs to ensure as much committed capital as possible flows into investments. Please email us at steelatlas@hanoverpark.com for any fund questions.

Supply chain & logistics technology company

Highlight: $10.2M in Annual Recurring Revenue (ARR) bookings

Next Key Milestone: Service larger commercial auto insurance market.

Next Expected Round: $20M+ Series B by Q4 2025.

Background: GenLogs is a supply chain & logistics technology company that uses proprietary data + AI to track and analyze US long-haul freight in real-time. In the US, there are 27K brokers tasked with moving $1T of goods each year by placing loads from shippers on one of the 4M trucks operated by 500K individual carriers. Today, brokers attempt this market matching without the single most important piece of data for doing it efficiently: the location of each of these trucks at any point in time. Vast amounts of data are being generated by the trucking industry daily, including mobile-ad-IDs and electronic logging devices. The issue is that this data is anonymized and thus not linked to a specific truck. The same problem applies to satellite imagery and traffic camera data that only reveal the presence of a truck at a certain time and place without identifying the specific vehicle (DOT number, carrier name, etc).

GenLogs has developed a proprietary approach for solving this problem scalably and without need for permission from individual truck owners. By deploying only sensors across the US to act as virtual gates, GenLogs is able to generate a distinct ID for each truck that passes a sensor that can be used to deanonymize the previously mentioned datasets. This breakthrough allows GenLogs to passively track all trucks in real-time using a fusion of disparate datasets, including satellite data, mobile ad IDs, and public traffic cameras. Using this data, GenLogs is developing best in class tools for the trucking industry.

Update: As of April 2025, GenLogs has surpassed $10.2M in ARR bookings – up from just $7M at the end of Q4 2024 – all without deploying a formal marketing budget. Average contract value now sits at $127K, and the company has 80 customers across contract, pilot, and advanced pipeline stages. While the freight market continues to contract given pressures from tariffs and trade negotiations, this has pushed GenLogs to accelerate expansion into more resilient verticals, particularly insurance and public sector, where product-market fit is emerging even faster than expected.

In commercial auto insurance, GenLogs is positioning itself as a modern replacement for the Central Analysis Bureau (CAB), which has long dominated the market using only publicly available FMCSA data. At the recent MCIEF conference, GenLogs' VIN-level intelligence generated immediate traction, with prospective customers noting the platform surfaced risk signals unavailable through legacy tools. Progressive has already called GenLogs' data "the best we've ever seen," and a customer waitlist has begun to form. GenLogs is taking a pragmatic approach to pricing: undercutting CAB by 25% in year one based on invoice data, with plans to increase pricing as value is demonstrated. This wedge into underwriting and claims workflows could unlock a large and underserved market.

The public sector is also becoming a breakout opportunity. GenLogs now has 13 active pilots with federal, state, and local agencies, supported by the formal buildout of a dedicated public sector team. Early traction is strongest in law enforcement, where GenLogs is delivering data and capabilities not available from $7.5B-valued incumbents like Flock Safety. In states like Florida and Texas, GenLogs is working directly with agencies such as FDOT and DPS, which has enabled sensor installations on public infrastructure and dramatically accelerated footprint growth. The company is executing a playbook that could be replicated nationally and is expected to mature into federal-level contracts beginning in FY27.

Sensor deployment has grown 32% over the past quarter, from 127 units in January to 195 by mid-April. Of these, 168 are proprietary GenLogs units and 27 are sourced through third-party agreements. GenLogs now captures data on over 75% of all active for-hire FMCSA carriers (trucking companies), far exceeding the reach of competitors like Samsara. The company has invested in fleet expansion, hardware upgrades, and resilience measures to ensure sensor uptime keeps pace with network scale. While international expansion into Mexico remains a challenge due to limited data infrastructure, GenLogs continues to explore backhaul solutions to unlock that market.

On the talent front, GenLogs has added a Head of Public Sector, a new Customer Success Manager, and a Deputy Sensor Deployment Coordinator. More importantly, the company will also onboard a new CRO from project44, with a mandate to drive $10M in additional ARR bookings by year-end. This hire is expected to significantly accelerate traction with shippers, a segment that remains relatively untapped but represents ~80% of U.S. freight contracts. GenLogs is also evaluating a shift toward per-seat pricing to complement its enterprise contracts. With 8,700 unique user logins and an effective price of ~$97/month, there is a clear opportunity to offer a "GenLogs Basic" tier (stripped of premium features) to drive product-led growth. If executed well, even partial penetration of the freight brokerage employee base could result in substantial upside, and this will be a near-term focus for the new CRO.

GenLogs' unique ability to collect and own first-party data continues to differentiate the platform as competitors increasingly rely on permissioned or indirect data sources. Lastly, the team is focused on the rollout of "GenLogs 2.0," which marks a transition from USDOT-level data to VIN-level data. This enhancement allows for the tracking of individual trucks within a fleet, enabling deeper compliance insights and analytics not currently available from competitors like Highway and DAT.

Nuclear energy technology company

Highlight: €10M convertible loan from SPRIND unlocked + $4M ARPA-E award secured.

Next Key Milestone: Sign binding agreement for first-of-a-kind (Los Alamos) + Execute two-week AI-driven cyclotron trial at PSI (April 2025).

Next Expected Round: $30M+ Series B by Q4 2025.

Background: Transmutex, founded in 2019 in Geneva, is reinventing nuclear energy for a safer, cleaner future. Transmutex's innovative approach addresses the core concerns associated with nuclear energy, notably waste, safety, and proliferation. Transmutex's technology is a significant advancement in carbon-free energy generation that is deployable around the world. Unlike traditional fission systems, Transmutex's system can use multiple types of fuels, including thorium, by using a particle accelerator to drive a safer, non-self-sustaining reaction. Applications of this technology are extensive including; efficiently breeding new fuel to replace uranium enrichment, enabling a new thorium-based fuel cycle for national security, burning the existing stockpile of long-lived nuclear waste to lower long term costs, and scalably producing medical radio-isotopes for cancer treatments. Transmutex has also developed simulation software with applications beyond nuclear energy.

Update: In Q1 2025 Transmutex locked in more than €10M of capital through a Convertible Loan Agreement with SPRIND, Germany's Federal Agency for Disruptive Innovation. The €7M tranche from SPRIND was unlocked by closing €3M of matching capital from external climate-focused investors, furnishing the company with resources to progress cyclotron procurement, licensing studies, and early site-development work.

Across the Atlantic, the US Department of Energy's ARPA-E awarded Transmutex $4.3M under the NEWTON program - the cohort's second-largest grant - to prove the viability of accelerator-driven transmutation for the nation's spent-fuel stockpile. The project, launching this quarter, aligns Transmutex with Los Alamos National Laboratory, the University of Maryland, Viam, and TechSource and will fund hardware and reliability experiments over the next 18 months. Under the NEWTON award, Transmutex is scoping a Cooperative Research and Development Agreement (CRADA) that would place its high-power cyclotron at Los Alamos National Laboratory as a modern, lower-cost alternative to the laboratory's kilometer-long LANSCE accelerator, an 800 MeV proton machine first commissioned in 1972 and now regularly forced to "turn away key mission deliverables" because of capacity limits. LANL's recent National Security Science feature, "Advancing accelerators," details the urgent need to replace or upgrade particle accelerators to sustain national-security experiments. By supplying a drop-in accelerator that can generate immediate research beam time without any nuclear-licensing component, Transmutex would unlock its first equipment revenue well ahead of full reactor deployment while giving Los Alamos a faster, more reliable path to meeting its mission requirements.

Government interest continues to deepen. SPRIND publicly released a six-month study prepared with Transmutex, TU Munich and TÜV Nord that names accelerator-based neutron sources the most cost-effective path for managing Germany's long-lived waste, drawing national press coverage and sparking a policy round-table in Berlin with Transmutex leadership. A Federal government coalition based solely on CDU and SPD is the best case for Transmutex in Germany since CDU publicly expressed support for Transmutation in their political platform and the SPD is not stringently anti-nuclear like the Greens would have been. Additionally, in January Dr. V. K. Saraswat, science adviser to India's Prime Minister, received the team in New Delhi to explore deployment scenarios for thorium-fuel systems in India's energy transition.

On the technical front, Transmutex rolled out TCortex, an internal large-language-model interface that lets engineers query proprietary data and streamline literature reviews, with future extensions planned for regulatory submissions. The Paul Scherrer Institute has granted an unprecedented two-week beam window in April to train AI agents that autonomously tune cyclotron parameters, while new pressing and sintering equipment is being commissioned to manufacture thorium fuel pellets on-site.

Strengthening the leadership bench, Transmutex appointed Craig Kelly as Chief Financial Officer; he previously served eight years as CFO at Terminal Investment Limited (MSC subsidiary) and earlier CFO at Oryx Petroleum from inception to IPO, bringing extensive project-finance and capital-markets expertise to guide the company's next phase.

Potassium-ion battery technology company

Highlight: Secured domestic prototyping capacity via BEACONS @ UT Dallas.

Next Key Milestone: Expand into data center applications via Uninterruptible Power Supply applications.

Next Expected Round: $10M Series A by Q4 2025.

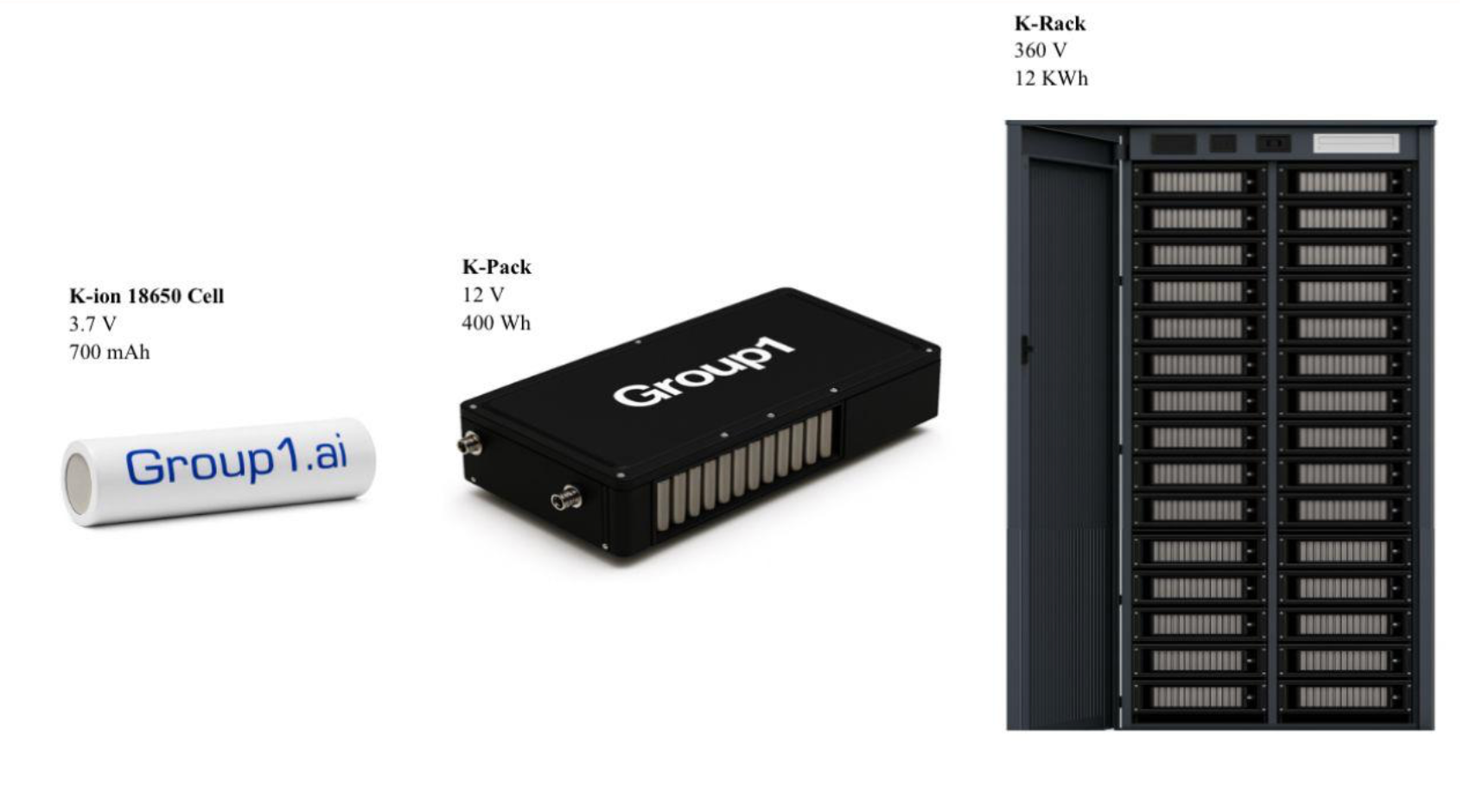

Background: Group1 is commercializing potassium-ion batteries (KIBs) which are poised to become a significant player in the energy transition, offering an attractive alternative to lithium-ion batteries due to their cost-effectiveness, resource availability, and environmental benefits. Unlike traditional lithium-ion batteries, which rely on critical minerals sourced from regions of geopolitical instability, KIBs utilize potassium, a more abundant and cheaper alternative. This reduces supply chain vulnerabilities. Group1's KIBs are critical-mineral-free and "drop-in" compatible with existing LIB infrastructure, ensuring a capital efficient path to scale. KIBs are on path to having energy density on par with LFP-based LIBs, comparable cycle life, faster charging, and superior low-temperature performance.

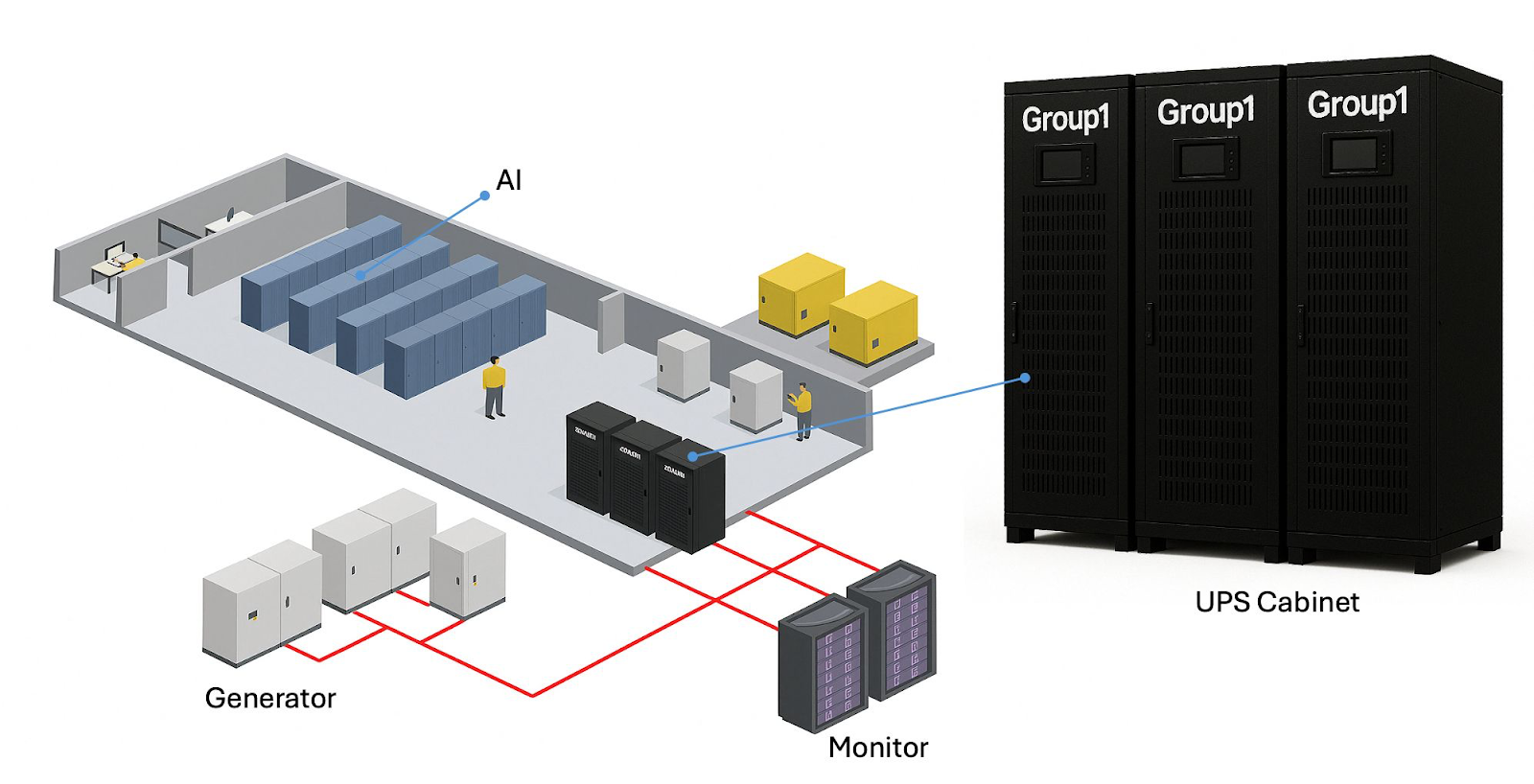

Update: Q1 2025 marked a major inflection point for Group1 as the company shifted decisively from R&D to productization. With strong macro tailwinds driven by U.S. reindustrialization, critical mineral constraints, and explosive growth in AI-driven data infrastructure, Group1's potassium-ion battery (KIB) platform is gaining momentum as a commercially viable, domestically sourced alternative to lithium-ion chemistries. The company's primary focus is now on Uninterruptible Power Supply (UPS) applications for data centers - an ideal first market given KIB's superior safety, supply chain resilience, and regulatory fit. Texas, home to over 20% of U.S. data center capacity, remains a focal geography for this effort.

Over the past quarter, Group1 completed key technical and strategic milestones. The company's 18650-format KIB cells are undergoing final validation, and the integrated MVP pack and cabinet system is on track for preliminary completion by mid-April. The product has demonstrated 20C discharge capability (well above typical UPS requirements) and is being optimized for thermal stability and safety using non-flammable electrolytes. This positions Group1 to deliver a differentiated solution in a market that is cost-tolerant but deeply risk-averse. With lithium-ion systems still posing meaningful thermal risk, KIB's inherent safety profile is becoming a central selling point in hyperscale procurement conversations.

Group1 has fully pivoted from a "technology push" model (focused on chemistry licensing) to a "market pull" approach, building and delivering complete battery systems tailored to end-user needs. Engagements are underway with leading hyperscale cloud providers (Amazon, Microsoft, Google) and critical power infrastructure players like Schneider Electric. This full-stack strategy allows Group1 to accelerate market feedback cycles, preserve IP, and control quality and supply chain execution. The company's ARPA-E and EAR99 compliance requirements have also necessitated U.S.-based cell finishing and integration, which Group1 has embraced as a strategic advantage. To that end, the company has secured domestic prototyping capacity through BEACONS and will leverage EVE Energy to supply dry, unfilled 18650 cells. These will be finalized in the U.S. by Group1 - qualifying as "substantial transformation" under export law. This hybrid approach balances speed, cost, and compliance as the company scales up.

In parallel, Phase 2 of Group1's Joint Development Agreement with Orbia has progressed, securing advanced electrolyte materials and integrating recycled graphite, which improves both manufacturability and environmental profile. The broader geopolitical environment has reinforced the urgency of domestic battery manufacturing. While Group1's direct exposure to China tariffs remains limited, second-order effects have increased material costs by 15–20%. Despite this, the company remains confident in its ability to manage costs through domestic supplier development and expects material quality to improve as domestic battery manufacturing scales. In the near term, many target applications exceed performance requirements, providing flexibility in material selection.

Commercially, Group1 made the strategic decision to pause engagement with ATL, a large Chinese cell manufacturer, after they raised performance thresholds mid-discussion and introduced export complications. This decision aligns with Group1's broader thesis: the U.S. battery ecosystem will need fully domestic solutions not only for compliance, but for long-term reliability and energy security. Group1's IP, which avoids lithium, cobalt, and nickel, is particularly well-suited for this moment, and the company is positioning itself as a key enabler of the U.S. energy transition and AI infrastructure buildout. Group1 continues to nurture long-term relationships with automotive OEMs, including Stellantis, but has prioritized the UPS/data center segment for near-term commercialization. With hyperscale demand booming and federal policy increasingly aligned with domestically manufactured, critical-mineral-free battery solutions, Group1 is positioned to become a foundational player in the next generation of U.S. energy infrastructure.

AI structural engineering firm

Highlight: Crossed $2M in booked revenue (up from $800K in Q3).

Next Key Milestone: Secure US Army contracts for bases via OTAs.

Next Expected Round: $10M Series A by Q4 2025.

Background: Hedral is an AI structural engineering firm based in New York that enables real estate developers to build faster, cheaper, and with lower environmental impact. Today, Hedral is already the most efficient structural engineering firm in the world, delivering stamped drawings and 3D building models to developers 10x faster than legacy firms. Hedral's core technology automates the creation of the drawings and models that takes traditional firms weeks to months to produce manually. This is positioning Hedral to roll-up the fragmented, multi-hundred-billion-dollar market for construction design and engineering.

Update: The Hedral product engineering team has achieved a breakthrough in autonomous value engineering capabilities, marking a significant evolution in their core technology. The system now independently optimizes building designs and structural elements, running complex simulations to identify cost-saving opportunities in construction processes. This advancement extends to automated optimization of rebar cross-sections and concrete columns, demonstrating their platform's growing sophistication. A major New Jersey-based client has validated this capability, committing to a long-term partnership for multiple tower projects after witnessing a successful demonstration in Q1.

Q1 demonstrated strong commercial traction with a $1.2M US Navy contract secured through sole-source procurement. The company continues to expand its government partnerships, with an ongoing US Air Force SBIR Phase I project showing promising signs of Phase II conversion as described in our last update. Notable follow-on investors in a small extension included Eric Schmidt and Valor Equity Partners, supporting a monthly burn rate of $160,000 as they invest in growth.

The company has grown to approximately 20 team members, strategically expanding beyond their initial focus on structural engineering. Current hiring efforts are concentrated on MEP (Mechanical, Electrical, and Plumbing) engineering capabilities, which is necessary to build a comprehensive automated design solution. This team growth comes as they navigate a complex sales environment with a volatile US economy. Despite these headwinds, the team has maintained focus on product development and sales pipeline building, though closing times have extended and project delays are impacting earnout expectations. This environment has reinforced the importance of Hedral's diversified approach to both government and commercial contracts.

Nuclear energy and synthetic fuels company

Highlight: Thermal reactor demonstration complete in record time.

Next Key Milestone: The first Gen IV reactor startup to split atoms.

Next Expected Round: $30M+ Series A by Q3 2025

Background: Valar Atomics is pioneering a breakthrough in energy by combining proven High-Temperature Gas Reactor (HTGR) technology with a novel business model to create synthetic, net-zero fuels. Led by Isaiah Taylor, an autodidact and serial entrepreneur, and supported by Chief Nuclear Officer Mark Mitchell, a leading expert in TRISO-fueled reactor design, Valar's integrated approach removes traditional barriers to large reactor-deployments via a business model that enables single-sites with hundreds of reactors. With the potential to disrupt both energy and industrial sectors in need of high temperature heat, Valar is poised to deliver clean, competitively priced synthetic fuels at scale — unlocking a trillion-dollar opportunity in the global energy market.

Update: Valar Atomics announced their seed round and capped the quarter by running Ward Zero through a thermal demonstration at its El Segundo factory. This is its first reactor prototype, using silicon carbide instead of uranium in the core. This test strategy will allow the company to play through disaster scenarios and collect real data before creating a uranium prototype. This proof-of-heat clears the last engineering hurdle before first criticality and positions the company to "split atoms" later this year, a step that will anchor the $30M Series A planned for Q3 2025.

While the factory team put the reactor through its paces in California, Valar formally launched the Valar Atomics Research Institute (VARI) in Manila alongside US Ambassador MaryKay Carlson, State Department Non-Proliferation Deputy Ann Ganzer and Philippine Assistant Secretary of Foreign Affairs Jose Chan-Gonzaga. VARI's first mandate is to deploy Ward One in partnership with the Philippine Nuclear Research Institute, expanding on the PRR-1 SATER program and operating under the 2024 US–Philippines civil-nuclear cooperation framework.

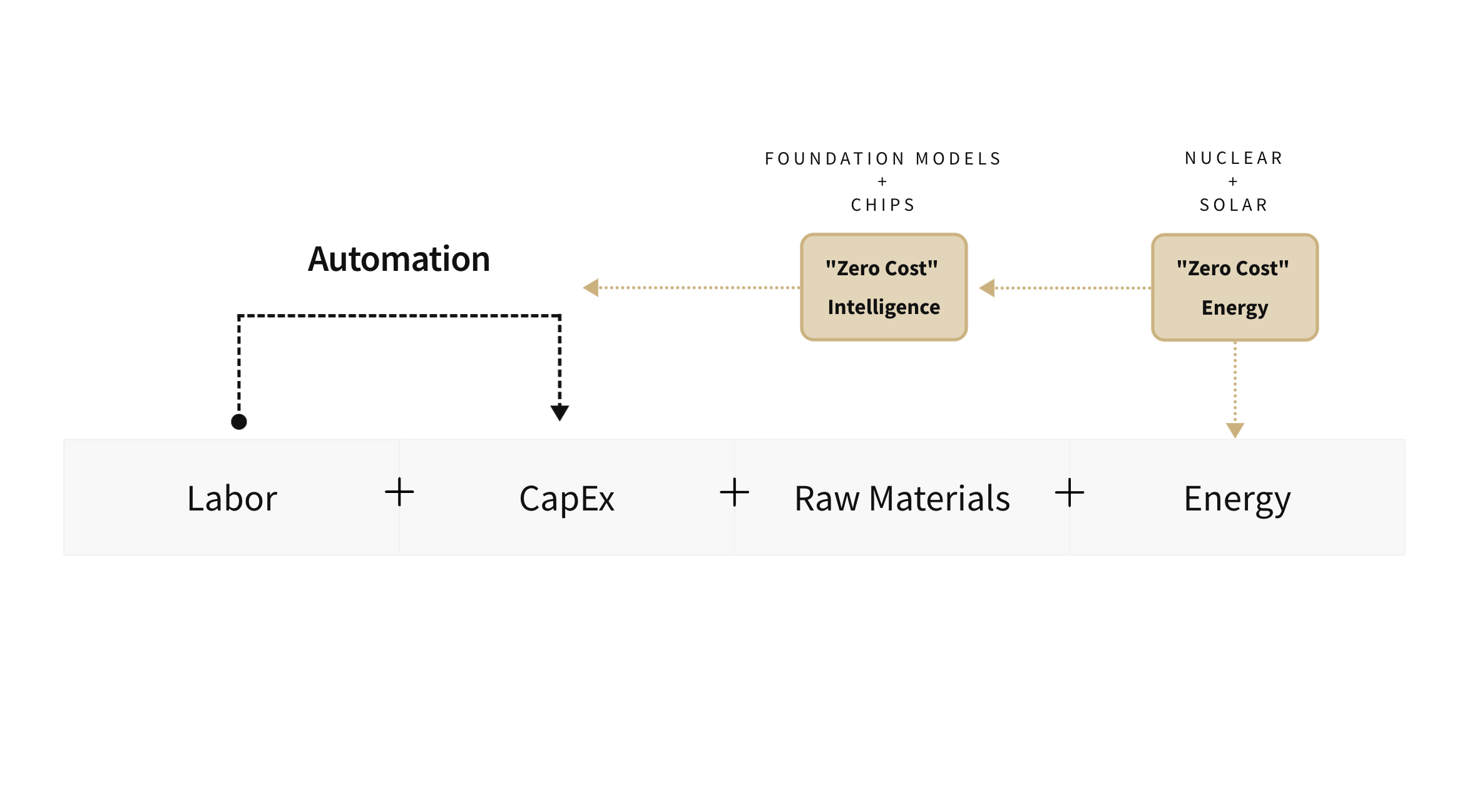

We are witnessing a foundational shift in the global industrial order. Where labor cost arbitrage once necessitated the international fragmentation of supply chains, automation — powered by zero-cost intelligence and declining clean energy costs — is reallocating the underlying cost structure of industrial processes. In this new configuration, the West and its allies can emerge as primary beneficiaries. We at Steel Atlas exist to catalyze and capture the generational value this transition is creating by becoming the leasing early stage industrial technology fund.

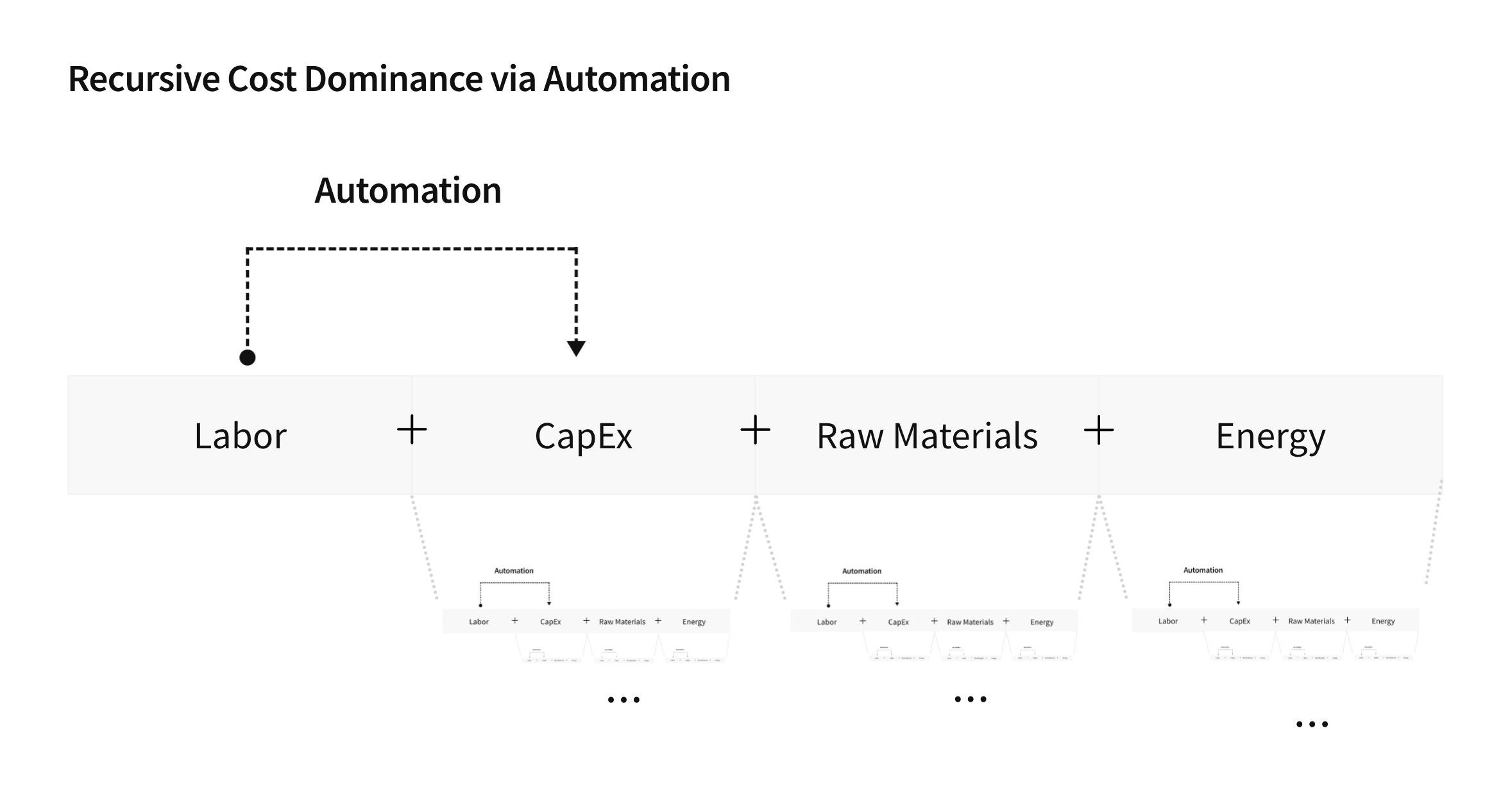

Every industrial process is defined by four fundamental cost components: labor, capital expenditure (CapEx), raw materials, and energy. Understanding how technology, policy, and capital flows act on these vectors — either reducing, reallocating, or amplifying them — is essential to forecasting where new industrial value will be created.

Labor — Direct human input, including wages, benefits, and supervisory overhead. Historically the dominant term in the cost stack, particularly in labor-intensive sectors.

CapEx — The total cost of equipment, facilities, and infrastructure over time, encompassing initial investment, financing amortization, maintenance, and depreciation.

Raw Materials — Input costs beyond labor, capital, and energy, including base materials, logistics, storage, packaging, and waste disposal. This encompasses the complete cost of sourcing and delivering inputs to production.

Energy — Power required throughout the production process—primarily electricity, but also heating, cooling, and process energy.

Today, we are living through a historic re-allocation of cost structure across these components. Understanding and enabling this evolution is core to our strategy.

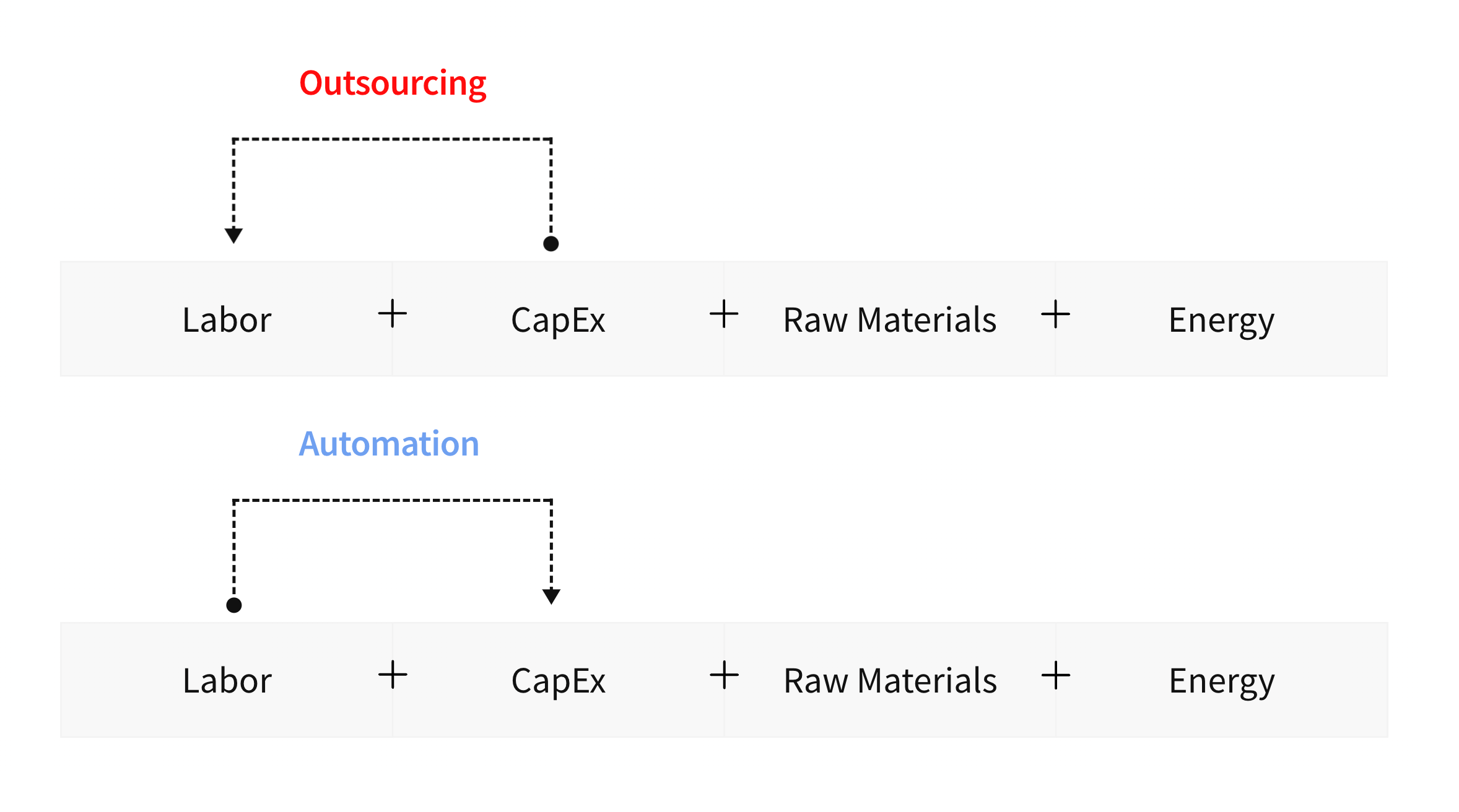

From the 1970s onward, industrial globalization followed a coherent, cost-driven pattern. Firms exploited wage differentials by offshoring labor-intensive production to jurisdictions with low regulatory burdens. Distance-based frictions — logistics, latency, and coordination — were gradually minimized through containerization, software coordination, and trade liberalization. This model, while effective for decades, has become increasingly fragile. Pandemic disruptions, geopolitical tensions, and logistical instability have revealed its vulnerabilities. More importantly, automation, artificial intelligence, and clean energy are actively reweighting the industrial cost stack. Robotic systems now perform high-dexterity, variable-tolerance tasks once confined to human labor. Vision systems and force-feedback loops have closed capability gaps in assembly, inspection, and handling. Simultaneously, foundation models provide scalable, ambient intelligence that coordinates production, scheduling, and quality assurance at near-zero marginal cost. The rapid decline in AI inference costs has made it viable to replace not only labor, but also entire coordination layers. These developments are made scalable by access to abundant, low-cost clean energy. Solar power now sits at the low end of the cost curve; advanced nuclear reactors and CCS-enabled gas provide stable, long-duration baseload capacity. Cheap cognition, powered by cheap electrons, are redefining the economics of Western industrial production.

We see four foundational trends shaping the recomposition of costs in industrial processes.

Labor is becoming CapEx: Vertically integrated automation and AI reduce labor variability, enhance quality, and compress lead times. Labor is no longer a fixed constraint but a variable replaced by machines and models.

CapEx is becoming modular and financeable: U.S. capital markets, combined with industrial policy tools — tax credits, accelerated depreciation, offtake guarantees — are enabling the rapid rollout of production assets. Alongside that, companies are developing "containerized" processes for everything from nuclear energy to mineral refining, smoothing scaling and easing financing.

Energy costs are declining: Falling LCOEs for solar, the emergence of clean baseload from SMRs, and favorable policies for CCS are giving the U.S. a systemic energy advantage. Texas is a global leader in energy cost and reliability.

Local feedstock is coming online: From cotton and timber to rare earths and synthetics, U.S. access to critical materials reduces geopolitical exposure and cost.

As these vectors shift, site selection logic is recalibrated. Where firms once optimized for labor arbitrage, they now optimize for access to capital, energy costs, and supply chain simplicity. The West has a renewed opportunity to reassert leadership in global industrial capacity. Furthermore, since the construction of industrial facilities, extraction of raw materials, and production of energy are industrial process themselves, a positive feedback loop is created. As these trends like automation lower the costs in primary processes (construction, extraction, and energy production), downstream processes cost structure will collapse further.

Industries that historically depended on low-cost labor, high energy input, or proximity to feedstock are now ripe for reshoring. Just as textile production was among the first industries offshored, we believe textiles will be among the first to be reshored as these trends take hold. Once emblematic of globalization, textile manufacturing is undergoing transformation. Whole-garment 3D knitting eliminates multiple manual stages. Coupled with AI-driven design and just-in-time dyeing, labor becomes CapEx. As energy and materials take over the cost stack, the U.S. — with cheap power and dominance in cotton and polyester — can reassert itself. A new techno-industrial champions can emerge.

Other sectors aligned with the reshoring thesis include:

Precision Metal Components: Driven by CNC automation, additive manufacturing, and defense demand.

Advanced Electronics and PCB Manufacturing: Reinforced by CHIPS Act investment and the modularity of SMT processes.

Rare Earth Magnets and Critical Mineral Processing: Enabled by domestic feedstock and strategic imperatives.

Green Ammonia and Fertilizer Synthesis: Supported by surplus renewables, CCS-enabled gas, and hydrogen localization.

Continuous Biomanufacturing: Powered by modular micro-reactors and a national imperative for pharmaceutical resilience.

These sectors are not speculative. The technology is ready, policy support is active, and the economics are aligning. They are investable today.

Steel Atlas was founded on the belief that technology and policy alignment would open a once-in-a-generation opportunity in industrials. That transformation is now underway and reflected in the early performance of Fund I. But our ambitions go further. With Fund II, we will continue investing in founders who can translate automation, energy advantage, and modularity into durable industrial platforms. The companies we back today will be tomorrow's techno-industrial incumbents. We are living through an historical land grab to own the future of industrial capacity. More importantly, we are optimally positioned to enable and capitalize on it.

Onwards and upwards,

Cameron & Talal

Steel Atlas General Partners