August 15, 2025

Dear Investor,

In the secure portal, please find the unaudited financial statements, your capital history, unrealized and realized activity report, and capital statements for the second quarter of 2025.

For planning purposes, we expect to do our next capital call in August 2025 for ~10% of committed capital. We are currently on pace to invest in two more companies through the end of Q3 2025 at which point we will be fully deployed out of Fund I.

We made 2 new investments into Framework Automation and ODIN Space in Q2 2025. Details of both companies can be found below.

As a reminder, we have migrated our fund administration to Hanover Park (an AI native fund administrator). Please email us at steelatllas@hanoverpark.com for any fund questions.

Software-defined manufacturing for on-demand knitwear

Highlight: Closed $6.5M seed round. Next Key Milestone: Open LA facility with first two whole-garment looms. Next Expected Round: Series A by Q3 2026.

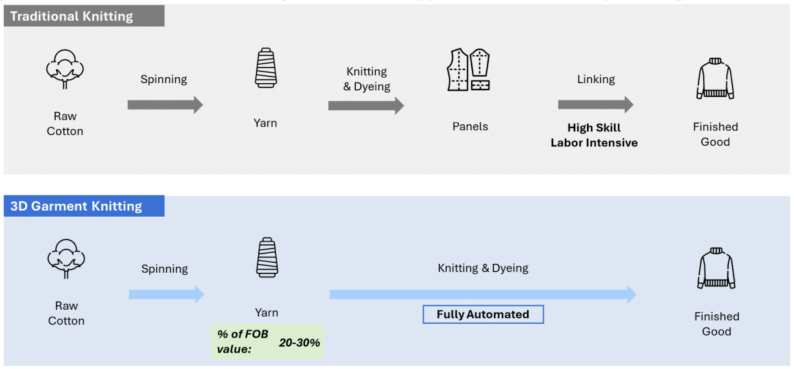

Background: Framework Automation is building America's next great industrial company, reshaping today's $260B knitwear market with a software-defined manufacturing platform that fully automates production. Their platform eliminates inventory and supply chain risk while achieving cost parity with Asia today. The US currently produces most of the world's cotton and polyester. But these raw materials are shipped abroad and made into clothing due to lower labor costs. Using 3D-knitting, Framework is eliminating this labor arbitrage to bring on-demand clothing manufacturing to the US.

Update: We invested $1.25M in Framework's $6.5M seed round alongside Lowercarbon Capital, Valia Ventures, Banter Capital, New Founding, SV Angel, and Discipulus Ventures. The company's defensibility lies in deep systems integration—treating manufacturing, design, and inventory as a unified, closed-loop system optimized for automation. Framework is establishing its first facility in Los Angeles and has secured interest from major brands including Skims, Revolve, Theory, and Ralph Lauren for initial sampling and production runs.

The team has made two key hires: Emily Keller from Tailored Industry to lead Knitwear Production (15+ years with Shima machinery experience) and Mustafa Tornaci as head of Textile & Material Science (former managing director of a Turkish export-focused knitwear mill with a masters in textile engineering). Additional offers are out for BizOps and a Founding Engineer (MechE PhD).

After conducting an extensive location study, Framework decided to establish their v1 factory in Los Angeles for proximity to engineering talent, brand partners, and investors, while planning their first scaled facility outside Austin post-Series A. They've put in bids for three LA locations and are in conversations with Shima Seiki to air freight their first 1-2 machines upon facility completion. The sales pipeline is strong with Skims, Revolve, Bloomingdales, Theory, Cuts, and Azazie ready to begin sampling, plus an upcoming conversation with Ralph Lauren's head of product innovation. Framework's immediate goals include securing their LA lease by August 18th, finalizing key hires, and beginning ERP implementation.

The company addresses one of the largest and most persistent inefficiencies in manufacturing: the time, cost, and rigidity of reconfiguring production lines and apparel supply chains. Framework's model eliminates the labor-intensive linking and sewing steps, allowing raw cotton yarn to be transformed into finished garments in a single automated process. By integrating on-demand dyeing, knitting, warehousing, and fulfillment into a unified system, Framework enables brands to offer unlimited product variety at cost parity with Asia while reducing inventory holding costs by 70 to 80% and cutting lead times from six months to 2-3 days.

The market context is significant. The US apparel market is worth $400B today and is projected to reach $600B by 2035, with knitwear alone accounting for $121B. The US is the largest exporter of high-quality cotton but produces less than 2% of its apparel domestically. The current model sends raw materials abroad for processing in labor-intensive facilities, requiring brands to commit large deposits months in advance, carry heavy inventory, and endure long lead times. Top US apparel retailers hold $45B in inventory on average, with two turns per year. The trade-off between SKU proliferation to capture market share and the capital intensity of stocking every size, color, and style creates a structural ceiling on growth and agility. Framework's model collapses this constraint. By holding fungible raw yarn and converting it into any SKU on demand, brands can proliferate styles without tying up working capital in finished goods. This converts the traditional multiplicative cost equation of styles x sizes x colors x materials into a sub-linear relationship, freeing capital for design and marketing rather than warehousing and markdowns.

The impact for brands is measurable: SKU counts can expand by orders of magnitude, stockouts are minimized, overstock losses are reduced, and working capital requirements fall dramatically.

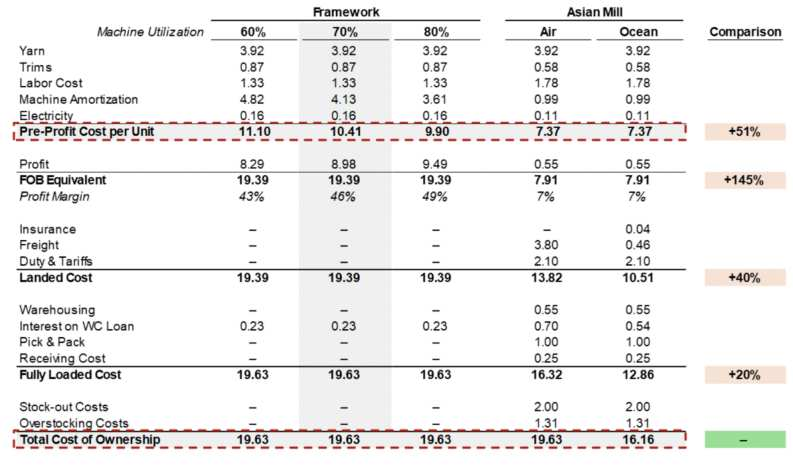

From a cost-physics perspective, Framework benefits from permanent US advantages: $0.80 per pound high-quality cotton, low industrial energy costs (Texas has the lowest in the world), and proximity to the largest consumer market. In knitwear, 70 to 80% of unit cost lies in processing rather than raw materials, making it highly susceptible to automation gains. Framework's use of the latest Shima Seiki 3D knitting machines at 70% or higher utilization achieves near-Bangladesh labor equivalents before factoring in the elimination of duties, tariffs, ocean freight, and long-term carrying costs. Total Cost of Ownership analysis shows Framework delivering equal or better economics than Asian mills today, with a structural cost advantage that widens as machine lease rates fall at scale, utilization rises, and vertical integration into yarn spinning reduces material costs by up to 30%.

The company's software layer is central to its defensibility. Framework is not a factory operator in the traditional sense. It is building a digital orchestration platform that integrates design translation, production scheduling, inventory management, and fulfillment across all processes. The system automatically generates production instructions, optimizes machine utilization, and tracks every garment from yarn selection to delivery. Competitors can acquire similar hardware but cannot easily replicate the software-driven coordination, the systems-level integration of upstream and downstream processes, or the operational data advantages that result. Framework's execution roadmap is clear: expand machine capacity to increase throughput and lower unit costs, integrate yarn spinning to capture more margin, extend the platform's orchestration capabilities, and scale into additional categories. The long-term vision is to own a significant share of the US knitwear manufacturing market by 2035.

Framework Automation is a case study in combining permanent cost-structure advantages with a systems-level rethink of production. By eliminating the traditional trade-off between variety and cost, it enables brands to compete on design and responsiveness rather than on inventory capacity. In doing so, it builds a scalable, defensible position as both a manufacturing backbone and a software platform for the next generation of industrial production.

Orbital debris detection and satellite insurance

Highlight: Won European Space Agency grant. Next Key Milestone: Secure key hire in sales and first contract with satellite operator. Next Expected Round: Series A in Q2 2026.

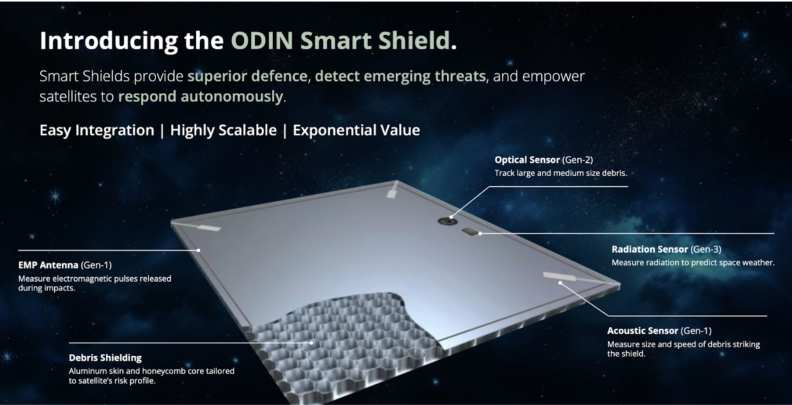

Background: ODIN Space solves the exponentially growing threat of orbital debris, where untrackable materials travel at 10x rifle speeds destroying billion-dollar satellites and constellations. With their proprietary Nano Sensors developed by CEO, Dr. James New during his time at NASA, ODIN detects previously invisible sub-centimeter debris. In partnership with Lloyd's of London, ODIN's sensors are enabling the first data-driven satellite insurance products that are 10-100x cheaper than current alternatives. With only 3-5% of satellites insured today due to high premiums, ODIN is unlocking mass-market satellite insurance, representing a $10B+ annual revenue market opportunity by 2030.

Update: ODIN Space is addressing one of the most critical bottlenecks in the emerging space economy: the lack of affordable, satellite insurance. Today, only 3-5% of satellites are insured because premiums are prohibitively high and all-risk policies bundle unrelated causes of failure into expensive packages. The core driver of these costs is the inability to diagnose and separate debris collision risk from other technical failures. Over 100M pieces of sub-centimeter debris travel at speeds exceeding 20,000 kph, each with enough kinetic energy to cripple or destroy a satellite, yet these fragments are invisible to current tracking systems. This diagnostic gap leaves insurers unable to price coverage accurately, pushing premiums beyond the reach of most operators, particularly in the fast-growing smallsat sector where insurance can consume 20-30% of asset value annually.

ODIN's proprietary Nano Sensors, developed by CEO Dr. James New during his NASA research, detect sub-centimeter debris in real time by capturing plasma, acoustic, and optical signatures of impacts. This capability allows insurers to identify debris-specific failures and offer named-peril collision coverage at a fraction of current prices, in some cases up to 100x cheaper than all-risk policies. A typical policy enabled by ODIN could cost $20,000 annually for $4M in coverage, with ODIN earning an additional $30,000 per satellite per year from hardware, data access, and analytics. By unbundling collision risk, ODIN expands the pool of insurable satellites, attracts insurers back into the market, and starts a compounding data flywheel: each insured satellite generates unique impact data, improving underwriting models, reducing premiums further, and driving more adoption.

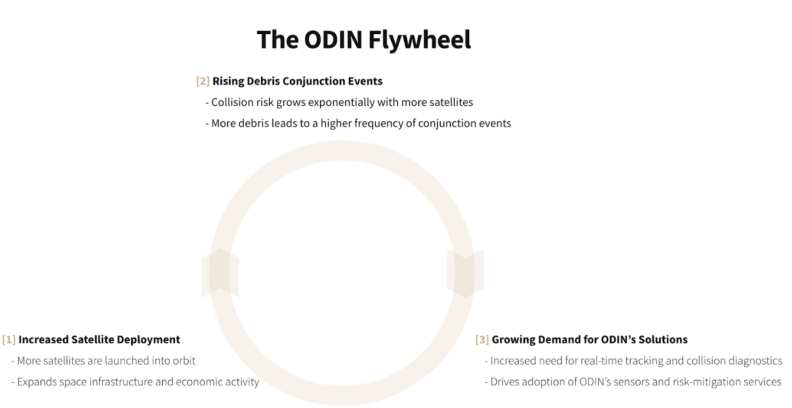

The scalability of ODIN's approach is amplified by its go-to-market model. Rather than selling to individual operators, ODIN targets the roughly 100 satellite manufacturers that collectively produce tens or hundreds of satellites annually. A single OEM integration can create a high-leverage sales cascade, and early discussions with manufacturers such as ICEYE validate demand. Competitive pressure is likely to accelerate adoption across suppliers, as OEMs offering satellites with bundled low-cost insurance gain a sales advantage. Once deployed at scale, ODIN's sensors form a persistent, distributed data network that generates the first orbital debris map inclusive of sub-centimeter objects. This dataset has high multiplayer value, serving not only insurers and operators but also governments and defense customers without additional hardware integration.

The financial potential is significant. At projected deployment rates, global on-orbit satellite asset value will exceed $300B by 2030. Premiums at 2-5% of asset value imply a $6-15B annual market for on-orbit coverage. With 20% market share and conservative pricing, ODIN could generate $300M in annual recurring revenue at approximately 80% gross margin from 10,000 satellite integrations, without relying on megaconstellations like Starlink or OneWeb. The model's operating leverage comes from recurring subscription and data revenue layered on low-CapEx hardware, indexing ODIN to the growth of the entire space economy. Beyond insurance, ODIN has a clear path into high-value defense applications. Its planned Smart Shield product will integrate debris detection with large-object optical sensing, radiation monitoring, and electromagnetic pulse detection. This would allow satellites to respond autonomously to threats, reduce insurance premiums for equipped spacecraft, and attribute impacts to deliberate acts—critical for military and intelligence applications. As space becomes a contested domain, such defense-oriented products could generate hundreds of millions in annual revenue.

ODIN's competitive advantage is reinforced by technical, operational, and market barriers. No competitor offers micro-debris detection tied directly to insurance underwriting. Players such as LeoLabs and Astroscale focus on large debris tracking or active removal, while ODIN owns the wedge that unlocks affordable coverage for the most common but untracked risk. The company's intellectual property around sensor-enabled insurance creates defensibility, while Dr. New's years of work with NASA-level test infrastructure—including high-velocity gas guns for impact simulation—represent a multi-year head start. Partnerships with Lloyd's of London and other insurers further entrench ODIN's position by aligning its technology with the underwriting community's needs from inception.

The team brings complementary strengths. Dr. New is one of the world's leading experts on orbital debris detection, having designed, built, and tested flight-ready sensors for NASA missions. COO Dan Terrett adds operational discipline and cross-functional leadership, with experience managing large-scale restructurings and growth initiatives. Together, they combine deep technical capability, commercial insight, and early traction with insurers and OEMs. The strategic flywheel is powerful: install sensors via OEMs, collect proprietary debris data, lower premiums through better underwriting, drive further adoption, and monetize the dataset across multiple sectors. This cycle is strengthened by the fact that debris risk grows quadratically with satellite density, meaning every new launch increases the probability of collision events, and each collision creates more debris. ODIN's addressable market therefore expands organically alongside the growth of orbital infrastructure.

ODIN is a low-CapEx, high-margin index on the exponential growth of space assets, with a monopoly wedge in micro-debris detection and a direct link to the financial infrastructure that will underpin space commercialization. Just as Lloyd's of London catalyzed maritime trade by making oceanic risk insurable, ODIN can unlock the next phase of the space economy by transforming orbital risk into a priced, hedgeable, and insurable asset class. As the industry moves from exploration toward permanent off-Earth infrastructure—satellites, stations, lunar bases, and eventually Martian settlements—ODIN's technology, data moat, and insurer relationships position it to become the trusted source of truth for orbital safety and the insurance backbone of humanity's expansion beyond Earth.

Real-time supply chain visibility for trucking

Highlight: New CRO revamps GTM and pricing. Next Key Milestone: Hire CFO. Next Expected Round: $20M Series B by Q4 2025.

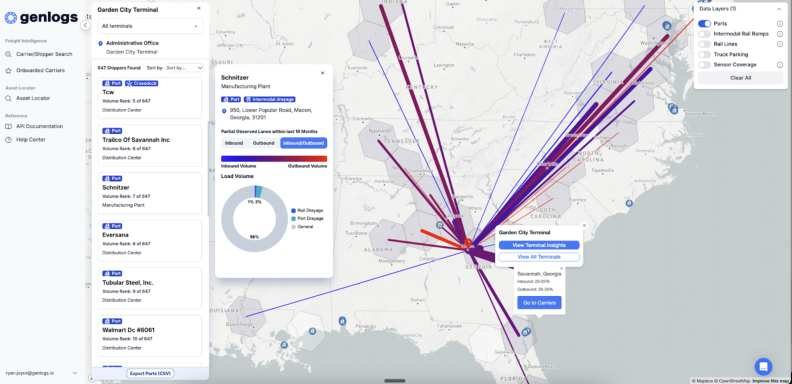

Background: GenLogs is a supply chain & logistics technology company that uses proprietary data + AI to track and analyze US long-haul freight in real-time. In the US, there are 27K brokers tasked with moving $1T of goods each year by placing loads from shippers on one of the 4M trucks operated by 500K individual carriers. Today, brokers attempt this market matching without the single most important piece of data for doing it efficiently: the location of each of these trucks at any point in time. Vast amounts of data are being generated by the trucking industry daily, including mobile-ad-IDs and electronic logging devices. The issue is that this data is anonymized and thus not linked to a specific truck. The same problem applies to satellite imagery and traffic camera data that only reveal the presence of a truck at a certain time and place without identifying the specific vehicle (DOT number, carrier name, etc). GenLogs has developed a proprietary approach for solving this problem scalably and without need for permission from individual truck owners. By deploying sensors across the US to act as virtual gates, GenLogs is able to generate a distinct ID for each truck that passes a sensor that can be used to deanonymize the previously mentioned datasets. This breakthrough allows GenLogs to passively track all trucks in real-time using a fusion of disparate datasets, including satellite data, mobile ad IDs, and public traffic cameras.

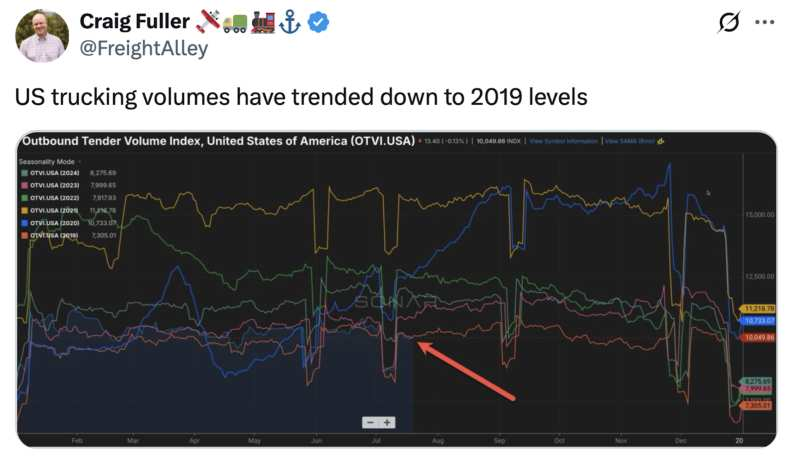

Update: GenLogs continues to grow in one of the most difficult freight markets in recent memory. National trucking volumes have dropped to pre-Covid levels due to reduced consumer spending and ongoing uncertainty around tariffs. Industry narratives had predicted a shakeout, expecting that the Trump administration's English Language Proficiency (ELP) mandate would force out low-cost immigrant drivers and tighten capacity. The mandate took effect on June 25, but rates and capacity remain unchanged. Carriers continue to hang on, and the oversupply of freight remains a persistent pressure on brokers, GenLogs' core customers.

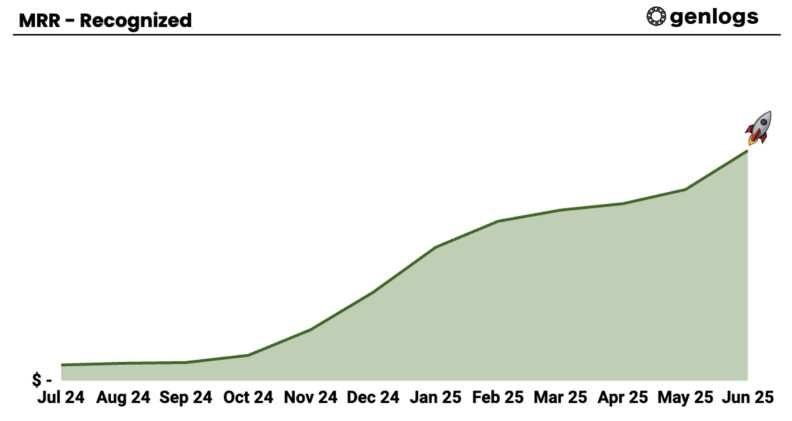

Even in this environment, GenLogs is still performing extraordinarily well. All of the company's first annual customer renewals converted in June with zero churn and 188% net revenue retention. After a deliberate overhaul of its Go-to-Market motion and pricing model, the company saw 23% month-over-month growth in June and is on track for similar results in July. Larger growth is expected later in Q3 and Q4. A notable deal with Amazon, valued at over $1m/year, is in procurement and likely to close by late Q3.

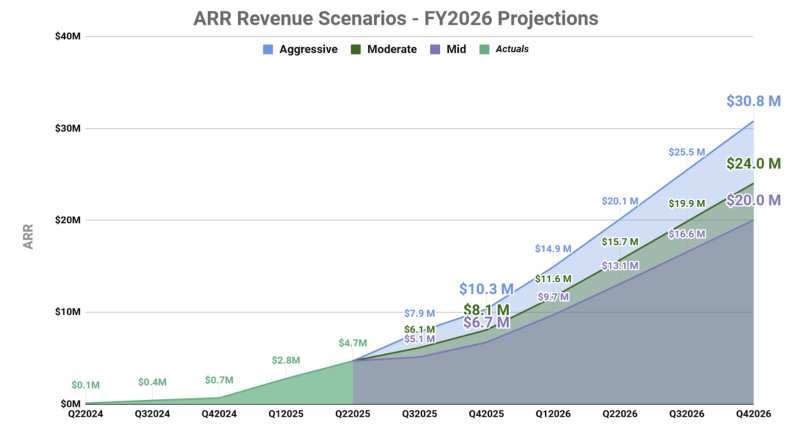

Earlier this year, GenLogs operated with a single enterprise pricing model that offered unlimited seats and searches at a premium price. Many customers experienced sticker shock, even with a risk-free 30-day pilot. The product was unproven, and the frictionless pilot process allowed unqualified customers to enter the funnel. As the market worsened, many pilots ended in indefinite delays, not from lack of product value but due to tightening budgets. GenLogs' refusal to offer modular options made continued adoption difficult. Growth slowed from February through April as prospects paused decisions. In late April, GenLogs hired Chief Revenue Officer Chris Kobus, who led a reset of the sales process. Trials were eliminated on June 1. The company migrated to Salesforce, purged unqualified opportunities, adopted the MEDDIC methodology, and introduced modular pricing to allow customers to start small and grow over time. Head of Customer Success Alex Burlingame built a structured CPQ system with a SKU list to support the new sales motion. With this foundation, GenLogs now operates against a full financial forecast and is targeting $8.1M in run-rate revenue by year-end, with a stretch goal of $10.3M.

As of June , GenLogs had 45 customers on annual contracts totaling $4.4M in ARR, with over $18M in qualified pipeline. Mid-market deals now close in about 45 days, while larger enterprise cycles take closer to 135 days. This dynamic has pulled down the average contract value (ACV) to around $100K. Once the Amazon deal closes, ACV is expected to rebound above $125K. Going forward, the company will report separate ACV metrics for mid-market and enterprise. GenLogs has more late-stage large contracts than ever before , with names like FedEx, GEICO, RXO, Walmart, Uber Freight, Forward Air, P&G, PepsiCo, STG Logistics, and CR England in the pipeline.

The pricing model now includes a base platform fee indexed to the size of the customer, with optional modules in Carrier Intelligence, Shipper Intelligence, and Asset Intelligence. Each module contains advanced SKUs, allowing customers to tailor contracts to their workflows and expand over time. On the product side, GenLogs released two major features in the last month. The first, Port Intelligence, gives insight into shippers using drayage through US ports. Initially developed for the Port of Miami, this feature has attracted significant inbound interest from port operators, freight forwarders, and related firms.

The second feature, Carrier Reports, provides deep insights into motor carriers by extracting FMCSA inspection data, cataloging risk scores, and reverse-engineering metrics previously limited to government use. The result is near-parity with Central Analysis Bureau (CAB), the dominant vendor for commercial auto underwriting. GenLogs believes it can surpass CAB by layering in proprietary network data from its sensors. Already, 20,000 carriers in GenLogs' network have no inspections on record with FMCSA, meaning CAB reports would be blank while GenLogs can provide detailed insights.

As of 15 APR 2025: 195 Sensors (168 GenLogs + 27 Third-Party). As of 22 JUL 2025: 280 Sensors (238 GenLogs + 42 Third-Party). The company's sensor network has grown from 195 to 280 sensors since mid-April, now including 238 GenLogs sensors. Coverage has expanded in Texas and the Pacific Northwest, reaching more than 85% of active for-hire carriers. The field operations team is now fully staffed, supported by three field crews, three bucket trucks, and a centralized HQ in Lufkin, Texas. The company remains on pace to reach 400 deployed Trident sensors by year-end, with an internal target of 600 by mid-2026. Network upgrades are underway, including remote diagnostic systems using Raspberry Pi and dual-SIM support for Verizon and T-Mobile, addressing past network reliability risks.

In the insurance sector, GenLogs closed deals with Progressive and Amwins, with contracts from GEICO and AIPSO expected shortly. CAB remains the incumbent, but customers increasingly acknowledge GenLogs' data superiority. Some are choosing to run both platforms during the transition period. The total underwriting TAM is estimated at $50M ARR, with another $50M possible through add-on services such as lead generation, continuous monitoring, and claims intelligence. The company is hiring additional product and sales personnel to support continued expansion into this vertical. Public sector adoption is increasing, though contracting remains slow. The number of active government pilots has more than doubled since the last update, now at 27, with over 200 active users across agencies. GenLogs is investing in long-term relationship-building with state DOTs and law enforcement groups, studying public sector contracting strategies used by peers, and working to shift sensor deployment CAPEX from GenLogs to government partners.

Advanced nuclear fuel and waste transmutation

Highlight: Operated high-powered cyclotron autonomously with AI. Next Key Milestone: Sign agreement for first-of-a-kind. Next Expected Round: $30M Series B by Q4 2025.

Background: Transmutex, founded in 2019 in Geneva, is reinventing nuclear energy for a safer, cleaner future. Transmutex's innovative approach addresses the core concerns associated with nuclear energy, notably waste, safety, and proliferation. Transmutex's technology is a significant advancement in carbon-free energy generation that is deployable around the world. Unlike traditional fission systems, Transmutex's system can use multiple types of fuels, including thorium, by using a particle accelerator to drive a safer, non-self-sustaining reaction. Applications of this technology are extensive including; efficiently breeding new fuel to replace uranium enrichment, enabling a new thorium-based fuel cycle for national security, burning the existing stockpile of long-lived nuclear waste to lower long term costs, and scalably producing medical radio-isotopes for cancer treatments. Transmutex has also developed simulation software with applications beyond nuclear energy.

Update: In Q2 2025, Transmutex advanced across technical validation, strategic partnerships, and deployment planning, strengthening its position as a global leader in nuclear waste transmutation. Between April 28 and May 8, the company's reinforcement learning agent operated the Paul Scherrer Institute (PSI) Injector 2 cyclotron (72 MeV), tuning 14 actuators in real time. Within four days, the AI surpassed expert performance , delivering faster tuning, improved beam quality, and zero interlocks. It ran autonomously for multiple 12-hour periods, adapted to varied resonator configurations, and consistently reduced beam losses without triggering safety shutdowns. Experts from CERN and Los Alamos National Laboratory (LANL) praised the achievement, and PSI is considering the approach for its 590 MeV cyclotron in 2026.

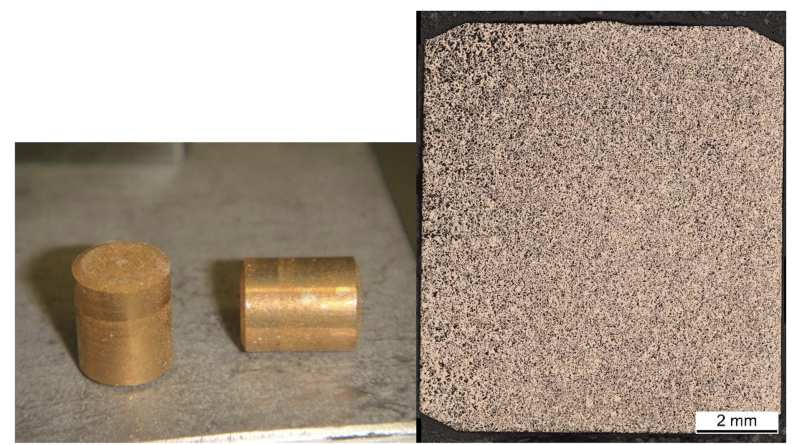

At the same time, the PSI fuel team led by Dr. Franz Strohmer validated an industrializable process for porous metal fuel pellets using tin and brass. The design enhances thermal stability in fast neutron environments by accommodating swelling and improving heat transfer. Thorium shipments from the US, delayed by customs, are expected imminently, enabling the first thorium-based pellets.

Transmutex has formally proposed installing a small-scale, fully functional START prototype at PSI during its 2027 long shutdown, integrating a proton beam, a liquid lead target, and the company's fuel for a complete spallation-based transmutation cycle. Operational in 2029, this would be the first demonstration of its kind and a critical step in staged deployment. PSI leadership has reacted positively. Internationally, progress continues toward a potential India-Switzerland nuclear cooperation agreement. NITI Aayog has indicated plans to formally approach the Swiss Ambassador, with Swiss ministries already supportive. The framework would enable thorium and transuranic fuel testing in India's fast reactors and create a path to a full START system. In the US, LANL's Accelerator and Nuclear Engineering & Non-Proliferation Divisions have expressed strong interest in hosting a full START system under a Cooperative Research and Development Agreement (CRADA). The Nuclear Engineering Division has requested internal approval to begin technical due diligence. In parallel, Transmutex is working in the US with TechSource and D-PACE on ion source development, identifying a lower-cost path for near-term deployment while assembling a global expert consortium.

In Germany, follow-up discussions are underway with the Bavarian government, RWE, and SPRIN-D to site a cyclotron at the decommissioned Gundremmingen nuclear facility. The location offers cost savings of 30-40% versus greenfield, existing infrastructure, and skilled labor. RWE may have financial incentives to support commercial reuse of the site. An MOU is targeted for Fall 2025, with Bavaria publicly endorsing the concept. Jean-Pierre Revol has also advanced outreach in northern Germany, presenting at Kiel University and addressing stakeholder questions on the role of transmutation alongside geological disposal. In Switzerland, CHUV, the country's largest nuclear medicine facility, is exploring a dedicated nuclear medicine center co-located with a cyclotron to produce advanced alpha-emitter isotopes. CHUV has issued a letter of support for a specialized facility in Germany, building on CERN and PSI research.

Transmutex's proprietary AI platform, TCortex, is now operational as a secure Swiss-hosted knowledge engine for automated literature review and internal information retrieval. New modules under development include licensing document generation, core design optimization, predictive maintenance, and fault detection. Urenco, Europe's largest enriched uranium supplier, has requested an MOU to explore collaboration on HALEU supply, U-233 fuel production using uranium tails, and potential use of TCortex and cyclotron-derived AI agents for process control in enrichment facilities.

Critical-mineral-free potassium-ion batteries

Highlight: Produced over 5,000 potassium-ion batteries across multiple form factors. Next Key Milestone: Sign first LOIs for uninterruptible power systems. Next Expected Round: Series A by Q4 2025 or Bridge Q3 2025.

Background: Group1 is commercializing potassium-ion batteries (KIBs) which are poised to become a significant player in the energy transition, offering an attractive alternative to lithium-ion batteries due to their cost-effectiveness, resource availability, and environmental benefits. Unlike traditional lithium-ion batteries, which rely on critical minerals sourced from regions of geopolitical instability, KIBs utilize potassium, a more abundant and cheaper alternative. This reduces supply chain vulnerabilities. Group1's KIBs are critical-mineral-free and "drop-in" compatible with existing LIB infrastructure, ensuring a capital efficient path to scale. KIBs are on path to having energy density on par with LFP-based LIBs, comparable cycle life, faster charging, and superior low-temperature performance.

Update: In Q2 2025, Group1 completed a transformation from a battery chemistry R&D company into a full-stack battery systems manufacturer. Since inception, the company has achieved what most new battery chemistry ventures require $50M+ to build on just $6M raised, producing over 5,000 potassium-ion (K-ion) batteries across multiple form factors, developing the complete stack from material to cell, pack, and cabinet, and engaging commercially with major datacenter and defense players.

The pivot, executed after a $1M bridge in December 2024, redirected Group1 from a chemistry platform to a product-driven business focused on uninterruptible power supply (UPS) systems for AI data centers. Deliverables since include MVP specifications for the K-Pack and K-Cabinet, and renewed engagement with top-tier commercial partners. Commercial engagement has accelerated. CBRE, a global real asset investment firm operating more than 100 data centers, is in active discussions for edge data center pilots. Orbia has entered Phase 2 of a paid joint development agreement. Scharf Energy, the company's commercialization consulting partner, is jointly pursuing opportunities with more than 10 companies across the datacenter value chain. Schneider Electric, a top-three systems integrator in the sector, has re-engaged to evaluate K-Pack and K-Cabinet. EVE Energy, a top-five Asian cell manufacturer, has begun a contract manufacturing partnership, with 400+ dry 18650 cells scheduled for August delivery to enable pilot builds, partner sampling, and safety validation.

The near-term technical milestones are EVE dry cell delivery in August, K-Pack builds and partner sampling in September, UL certification submission in Q4, and pilot deployments in Q1-Q2 2026. A key catalyst for the next round of funding will be Group1's spotlight address at the Reindustrialize Conference in July, a high-visibility forum connecting investors, policymakers, and technologists focused on reindustrialization, AI-driven energy demand, domestic manufacturing, and federal defense and DOE priorities. However, in order to raise a Series A, Group1 needs to demonstrate material commercial traction for their datacenter products. Further bridge funding could be required to get them to that point.

AI-powered structural engineering automation

Highlight: Self-serve design concepting tool launched. Next Key Milestone: Winning skyscraper bids in Texas representing first major commercial high-rise project. Next Expected Round: $15M Series A by Q1 2026.

Background: Hedral is an AI structural engineering firm based in New York that enables real estate developers to build faster, cheaper, and with lower environmental impact. Today, Hedral is already the most efficient structural engineering firm in the world, delivering stamped drawings and 3D building models to developers 10x faster than legacy firms. Hedral's core technology automates the creation of the drawings and models that takes traditional firms weeks to months to produce manually. This is positioning Hedral to roll-up the fragmented, multi-hundred-billion-dollar market for construction design and engineering.

Update: In Q2 2025, Hedral accelerated technical productization, strengthened its engineering core, and deepened traction in defense and critical infrastructure while navigating a sharp slowdown in commercial real estate. The most significant internal change was a decisive team restructuring. The company phased out its India-based engineering contingent, retaining only a senior Autodesk alumnus, and concentrated development around a smaller group of high-output specialists. This shift was triggered by a sprint in which two senior engineers replicated 2.5 months of prior work in 5 days, exposing inefficiencies and validating the case for a leaner, more senior-heavy team.

The reorganized product group now centers on a persistence layer that ensures structural geometry is saved and indexed for AI computation without reliance on 3rd party kernels. This foundation links three major modules: a concepting tool, detailed design automation, and downstream integration for structural and MEP systems. On the structural side, they have resolved long-standing solver issues in weeks by adding compliance scoring and automated code-check output. On the MEP side, AI-based cable routing will enter field trials within weeks. All work now runs on a tightly planned eight-week cycle with day-by-day ticketing.

Hedral launched its first self-serve concepting product, designed for rapid massing and structural shell generation before detailed engineering. A hyperscale data center operator has agreed to license the tool at $20K ARR, but the strategic value lies in reducing project onboarding friction. Once a client begins in Hedral's system, they can progress to detailed engineering in two clicks, bypassing traditional hand-offs. Defense emerged as a primary growth vector. The US Navy identified multiple facility types for Hedral application, including admin buildings, barracks, parking structures, and shipbuilding infrastructure. A live pipeline includes a $1.2M Navy contract and a pending $14M US Air Force opportunity. The head of Air Force construction has championed the technology internally. Hedral also bid on its first 60-story skyscraper in Houston and is pursuing a similar opportunity in Austin, each with potential value near $500K ARR.

Commercial real estate, by contrast, experienced a pronounced freeze over the summer. Longtime partner Lowney Architects saw 16 multifamily proposals on the West Coast stall without decision for over 3 months. Despite this, Hedral's overall pipeline expanded more than any previous quarter, driven by a distributed network of part-time business development specialists targeting regional markets such as Phoenix, New Jersey, and New York. These operators have produced introductions to senior executives at Fisher Brothers, Toll Brothers, and other large developers.

Product execution now operates under dual leadership: head of product directs core product logic with a team of structural and MEP engineer-programmers, while 2 AI engineers lead AI development. The software group will expand with young, high-throughput engineers skilled in computational geometry. Onboarding of high-profile industry talent continues, including senior figures from leading architecture-engineering firms and a Unity expert to advance Hedral's front-end.

The quarter's second strategic priority was building a defensible margin narrative ahead of the Series A. With sufficient project volume developing, Hedral is building proxies for unit economics based on reductions in labor hours relative to industry benchmarks. Time-tracking software now measures engineering hours against established cost models, producing data that can be referenced with prospective clients and partners. For key projects such as the Adams program, the company will show both client cost reduction and internal productivity gains. Looking forward, Hedral aims to drive repeatable volume in sectors with fast procurement cycles and high structural complexity, with defense and advanced industrial projects as near-term priorities. Nuclear infrastructure work has emerged as a complementary niche, with multiple operators exploring Hedral's design automation for specialized medical and industrial facilities.

Next-generation nuclear reactors and synthetic fuels

Highlight: Co-authored four Executive Orders for nuclear development with the Trump administration. Next Key Milestone: Break ground on a facility in Utah. Next Expected Round: $50M Series A by early Q3 2025. (Although the term sheet was signed in Q2 for $50M at $250M post-money valuation, this round will end up closing in Q3.)

Background: Valar Atomics is pioneering a breakthrough in energy by combining proven High-Temperature Gas Reactor (HTGR) technology with a novel business model to create synthetic, net-zero fuels. Led by Isaiah Taylor, an autodidact and serial entrepreneur, and supported by Chief Nuclear Officer Mark Mitchell, a leading expert in TRISO-fueled reactor design, Valar's integrated approach removes traditional barriers to large reactor-deployments via a business model that enables single-sites with hundreds of reactors. With the potential to disrupt both energy and industrial sectors in need of high temperature heat, Valar is poised to deliver clean, competitively priced synthetic fuels at scale, unlocking a trillion-dollar opportunity in the global energy market.

Update: On April 7, Valar Atomics filed a lawsuit against the US Nuclear Regulatory Commission (NRC), challenging what it argues is excessive federal overreach in licensing small modular reactors. The group includes the states of Texas, Utah, Louisiana, Florida, and Arizona, together with nuclear developers Last Energy and Deep Fission. Valar's position is that Congress never intended for all reactor types to be subject to the same stringent framework designed for large, utility-scale plants, and that certain lower-risk designs should be regulated at the state level. The suit is both a direct attempt to open a faster licensing pathway for its own technology and a broader move to create precedent for the sector.

Momentum continued in mid-May when Utah's Office of Energy Development signed a memorandum of understanding with Valar to evaluate the development of an advanced nuclear test reactor and a TRISO fuel fabrication facility at the state-owned San Rafael Energy Research Center in Emery County. This agreement gives Valar site access and state-level partnership without requiring significant upfront state funding. We expect Valar to break ground on this facility in Q3. This would make it one of the fastest commercial developments of any nuclear company in history. Governor Spencer Cox and Valar founder Isaiah Taylor publicly announced the MOU, setting an ambitious target to have the test reactor operational by July 4, 2026, coinciding with the US's 250th anniversary. This aligns with the federal administration's recently issued executive orders to fast-track nuclear deployment and fits into Utah's broader "Operation Gigawatt" initiative to bring new nuclear capacity online.

In late May 2025, Valar Atomics was directly linked to one of the most significant pro-nuclear policy shifts in decades: a package of four executive orders signed by President Trump to accelerate nuclear reactor deployment and overhaul what the administration called the "overly risk-averse culture" of the NRC. These orders set an 18-month deadline for NRC approval of new reactors, called for the construction of 10 large reactors by 2030, expanded US uranium and nuclear fuel capacity, and directed the Department of Energy and Department of Defense to enable reactor projects on federal lands. The public alignment between Valar's litigation, its Utah project timeline, and the administration's reform agenda underscores the company's growing influence in the national nuclear policy conversation. By pairing high-visibility projects with a willingness to challenge federal processes, Valar has positioned itself to capitalize quickly on these new timelines and siting flexibilities, potentially compressing years of licensing friction into a development cycle that matches private-sector speed. Valar is not just riding a favorable policy wave. It has helped shape the current pro-nuclear posture and is moving aggressively to convert that environment into near-term operational milestones.

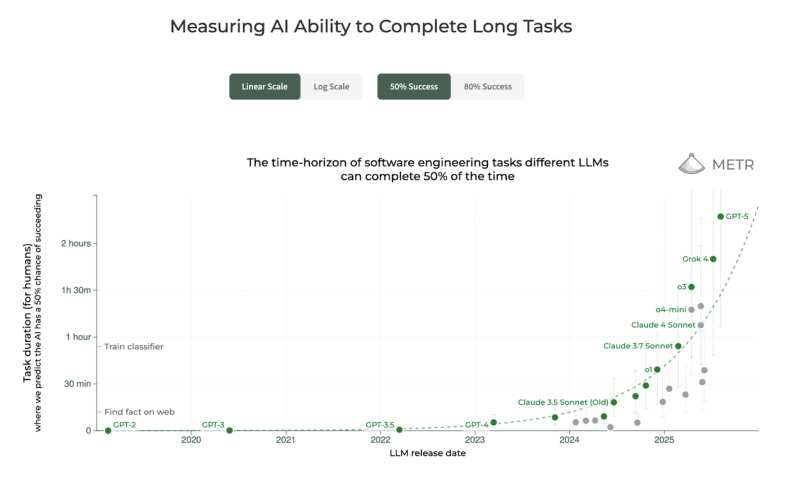

Since the release of ChatGPT (enabled by GPT 3.5), the default narrative has been one of AI takeoff. The imagined scenario is one where a leading AI lab develops a recursively self-improving model. In doing so, there is an intelligence explosion. That leading lab (and the nation behind it) then uses that model to diverge from the rest of the market to become strictly dominant across domains. AI 2027 is the canonical piece exploring (and supporting) this type of scenario. Evidence for this can be found in charts like the one below from METR (a leading independent model evaluation group). With the GPT-5 release last week, it looks like we are taking off...

There are important, observable political and capital allocation implications to this being the "default" view. For example, under the Biden administration, this drove proposals to constrain model development and curtail chip exports to adversaries to gain a one time advantage in race to super intelligence, instead of selling Nvidia chip designs openly to ensure foreign models remain reliant on US technology in the long run. Many of these approaches have continued under Trump, although recent policy announcements indicate the tide is shifting. Whether or not you believe (and believe others believe) we are headed towards a divergent or convergent future of model performance, is core to any forward looking assessments of technology or politics. Thus what we found most significant about the release of GPT-5 is that, despite its impressive performance, it gave some of the best evidence for a convergent future of AI (based on current model architectures).

In a convergent scenario, instead of seeing a widening gap between the top frontier model and the rest, we would expect to see frequent swaps at the top of leaderboards with frontier performance clustering as step-ups become more and more incremental. Historically, when OpenAI releases a new frontier model, they have dominated across the benchmarks. With GPT-5, they did not.

Whether or not you adopt the belief that foundation model performance is converging, at the very least you should re-weight your expectations. We have.

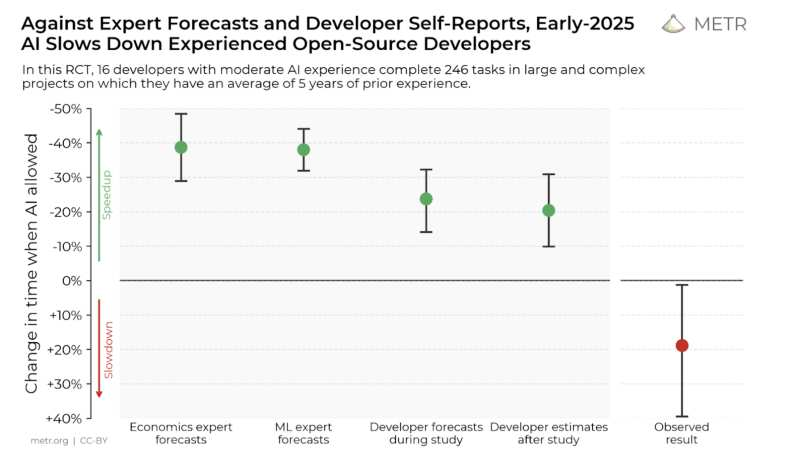

Once you cross the chasm from divergence to convergence, you begin to see a much longer journey to AI integration across workflows. Although even the existing abilities of foundation models have created a massive "product overhang" in terms of getting these capabilities in the hands of businesses, converting these capabilities into measurable outcomes is actually hard. Take coding, a domain where these models apparently excel. According to a randomized control trial by METR in early 2025 (the same group that released the breakout looking chart at the beginning), AI coding tools made experienced open source developers 19% slower in solving large, complex engineering tasks. This is despite the fact that these same developers believed both before and after trial that AI coding tools would speed them up by over 20%. How crazy is that!

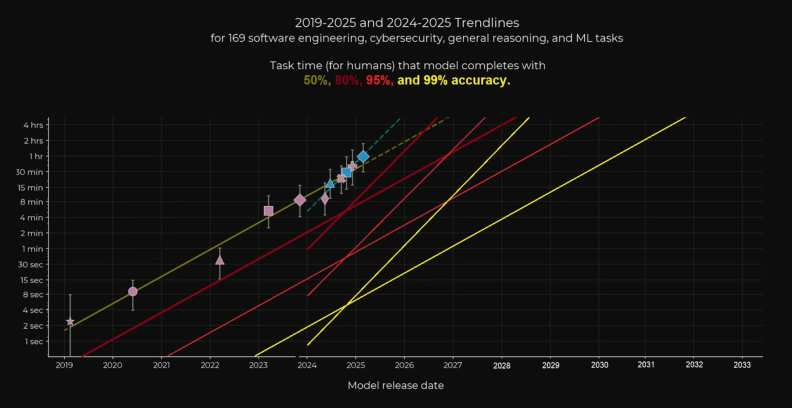

We believe there are two drivers of this phenomenon. The first driver is psychological. People really want to believe these models make them better because they allow them to be lazy. Instead of having to think hard, you can queue up a bunch of tasks that agents execute on your behalf. While they are executing you "productively do other work" (or just scroll something) and then come back to evaluate / integrate the outputs. Verification is the lazy man's execution. This leads to the second technological driver. The models are not reliable enough over long periods of time. Once again based on METR's research, the chart below shows the length of time a task can take and still be reliably executed by an agent at a given threshold (from 50% and extrapolating to 99%). The problem is in enterprises (especially industrials), AI agents need 95% or even 99% accuracy. Not 80% and certainly not 50%.

The fact that extracting measurable enterprise value from these models is more difficult than the market seems to have expected makes investing in AI-enabled products more attractive to us. As Balaji Srinivasan (ex a16z / CTO of Coinbase) eloquently put it, these models are "middle to middle" not "end to end". Not only do they show near zero ability to establish their objectives, but they require heavy prompting (one end) and verification (the other end) to be useful. This is precisely the opportunity for investing at the application layer of AI. Thus, the quality of the product/services these vertical AI companies develop around the foundation models matters deeply to delivering outcomes to enterprises. It is not as simple as winning the AI land grab by being a first mover (although that can produce advantages). It requires solving the context dependent AI reliability problem and doing so in a manner that does not rely on run-away token consumption that erodes long-term business model viability. Given that, we have identified a particular company archetype that we are excited to back.

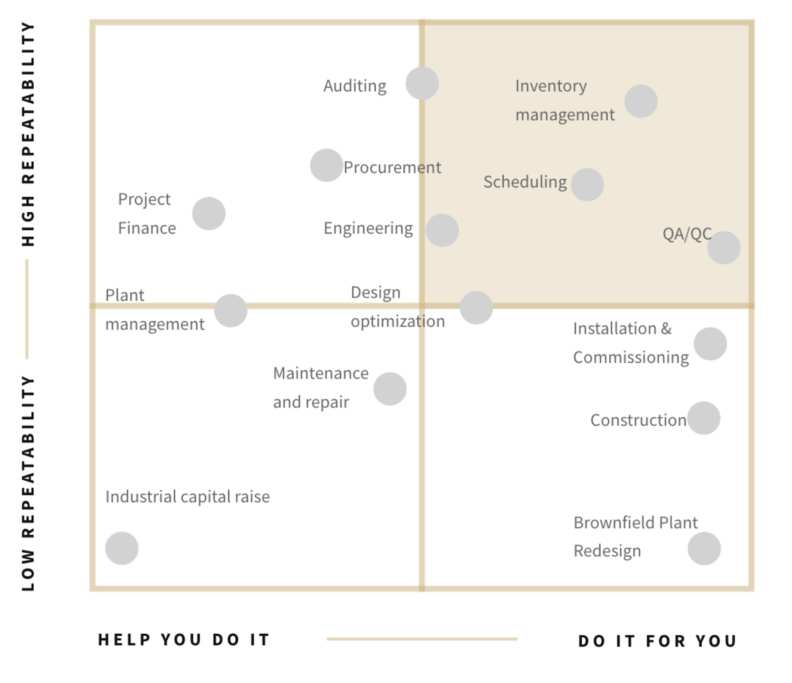

In our latest essay, Embedded Advantage, we argue that the right way to build in industrials is to lead with services, not software. Industrial companies buy results, not features. They have lived with low software penetration because "mostly works" breaks real operations. Their goal is to outsource operational risk to best in-class service providers. A services model earns trust by standing in the flow of work, taking responsibility for outcomes, and learning the local realities of each site/installation. Once that reliability is proven, the repeatable pieces can be productized into software and partially automated internally with foundation models (i.e. without exposing them directly to customers). As shown below, there are a wide variety of services that can be tackled with this approach.

In June, the well known podcaster and AI commentator, Dwarkesh Patel, wrote a piece titled, "Why I don't think AGI is right around the corner." The crux of the piece is that the lack of continual learning (the ability to retain and compound firm-specific feedback like human employees) blocks the use of AI in many real workflows (including his own). He argues current LLMs don't "get better" with you. This is precisely what the services approach solves for. A services company can continually learn at the firm level to ensure reliable outcomes, while internally optimizing operations with AI models. Eventually, if internal AI enabled tooling exceeds greater than 99%+ reliability, it can be sold as a SaaS product. The feather in the cap for the services approach is that it avoids the economic Achilles heel of vertical AI solutions. That Achilles heel is selling raw tokens. Many vertical AI products fix their price and then allow their customer to variably consume tokens. In these cases, the more users lean on top-tier models, write longer prompts, and click "run again," the faster your margins collapse. Your best customers become your downfall. This was exemplified by the acquisition of the AI coding platform, Windsurf. At roughly ~$80M ARR, usage of expensive frontier models pushed gross margins negative (at least for some customers). After the $3B OpenAI deal collapsed, Google executed a $2.4B license-and-talent pickup, and Cognition acquired the remaining business for ~$250M (including $100M in cash on hand). That's an $80M ARR company acquired for a 2x multiple. A services model avoids the trap. When you sell a service, you charge for the result, not the API call. By internalizing model usage, you control your cost structure. Ideally you even use platforms like Cline to provide an abstraction layer between you and the foundation models. This gives your business a cost and capability tailwind. When an inference provider lowers prices due to competition, every Cline user gets a cheaper product. When a new frontier model comes out, every Cline user immediately gets a better product. Simply put, as the general purpose technology improves and competition due to convergence drives prices down, your business improves too. Like with our investment in Hedral in the structural engineering space, we plan to identify more companies using this approach.

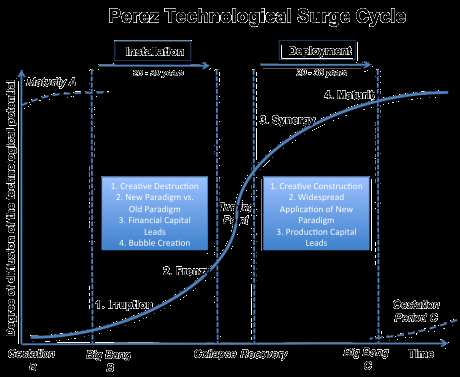

Instead of exponential takeoff (divergence), we see increasing evidence for the diffusion of transformer based AI models to follow Carlota Perez's canonical chart (convergence). We may still be in the frenzy, but there are signs (lack of reliability, lack of measurable performance improvements, shaky economics), that indicate that getting AI models used in the workplace will require high quality teams designing high quality products and services around their (incredible) abilities and limitations.

This has important implications across policy and our portfolio. Here are few key ones:

1. Energy — we believe we are likely over-estimating near-term energy demands from AI while still underestimating our long-term needs. In the near-term this will directly benefit our companies bringing their systems to market like Valar's reactors, Transmutex's waste/fuel products, and Group1's uninterruptible power systems. However, as we look to Fund II, we must be cautious as to what a correction could look like.

2. Chip Policy — to date, US chip policy toward China has been predicated on "AI take-off" panic. Instead, with take-off less likely, we believe we should focus on preserving US long-run leverage. This means selling China advanced US chips and allowing Chinese fabrication at TSMC, but banning all semiconductor manufacturing equipment exports. This will channel demand to US products / platforms, keeps China dependent on allied supply chains, and lowers China's incentive to build a rival stack or escalate over Taiwan.

3. Jobs — despite all of the progress with foundation models, they still require humans in loop. They require humans to provide sufficient context and direction to operate effectively. They also require verification and repeated use to deliver reliably. This means that as long as we avoid take-off towards AGI, job loss due to AI is likely overhyped. Rather, as with all general purpose technologies, those that use it best will stand to gain / replace those that do not.

In the end, we are incredibly excited about the period we are entering. As discussed in our last quarterly letter, we firmly believe we are entering a new techno-industrial paradigm (enabled by AI). It just turns out that unlocking this transition will require talented builders tackling hard problems (not just basic wrappers around foundation models). And this is exactly where Steel Atlas thrives.

Onwards and upwards,

Cameron & Talal