November 14, 2025

Dear Investor,

November 14th, 2025 RE: Steel Atlas Fund I LLC, (the "Fund") – 3rd Quarter 2025 Report

In the secure portal, please find the unaudited financial statements, your capital history, unrealized and realized activity report, and capital statements for the third quarter of 2025.

For planning purposes, we expect our next capital calls to be sent quarterly for trailing fees of the fund. Our last capital call invested our final check of the portfolio totalling 10 companies, leaving only management fees remaining to be called for the rest of the fund life.

We made 1 new investment into Substrate Industries in Q3 2025.

As a reminder, we have migrated our fund administration to Hanover Park (an AI native fund administrator). Please email us and steelatlas@hanoverpark.com for any fund-related questions.

Onwards and upwards,

Cameron & Talal

I (Cameron) have visited both of these trees. They are both more than 500 years old. They both give me a sense of awe. And they both have taught me a lot about how to grow a firm. There is conformity that comes with size, as if the laws of nature impinge on your existence ever more strongly. In the smallness though there is a freedom to defy that gravity. You can twist and turn into novelty, growing into areas that others would never explore. You become a beautiful alchemical combination of intentionality and serendipity that no one else can hope to reproduce.

For this reason, I love things that are grown (maybe even more than those that are built). And Steel Atlas is growing. We are growing like a bonsai, twisting and turning into new opportunities as a natural extension of where we have been. This essay is our articulation of how. We will start by sharing an experiment that shows why greatness cannot *just* be planned to gain an intuition for how conviction emerges. We will deepen this understanding through the story of how MongoDB is actually an extension of Dilbert (the comic strip). This will show us why experience matters and you can't just be a blind person describing the color blue if you want to have real conviction. And finally, we will bring it all together by going out on a couple limbs we are excited about — from radioisotope production / productization to bandwidth constraints and data backhaul.

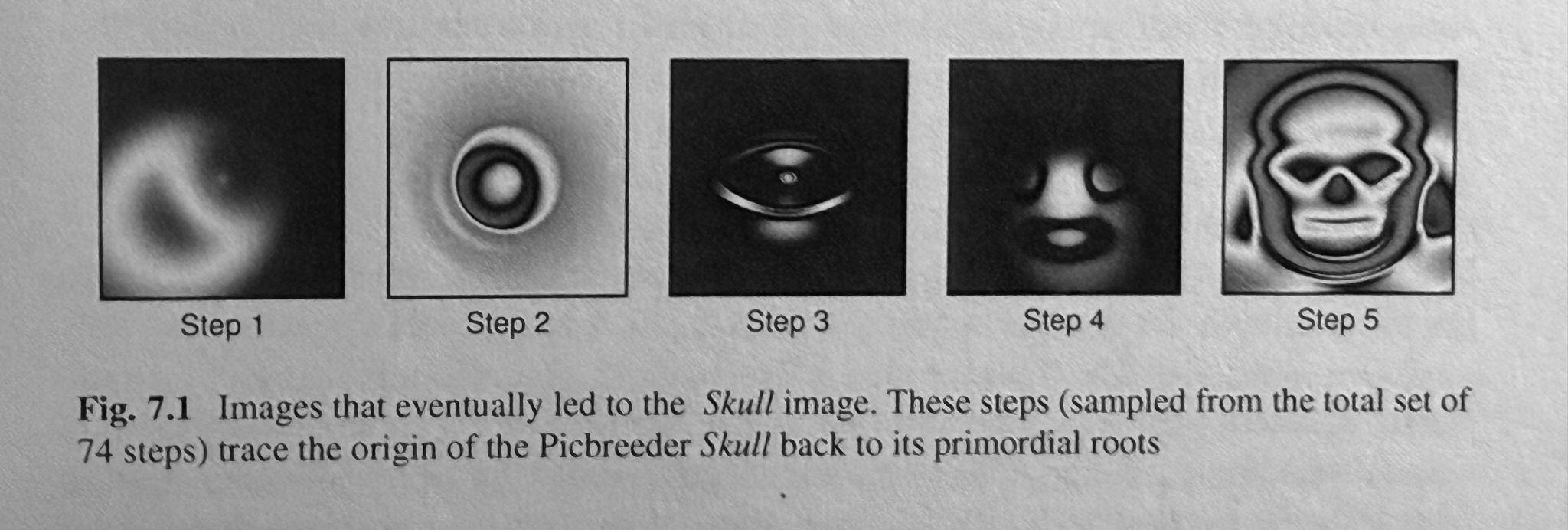

In 2015, I had just dropped out of Princeton where I was studying Computer Science to play for a team in Major League Soccer. At the time, I was a devout rationalist. I liked plans. I liked efficiency. I liked the idea that there were heuristics for things, ways to objectively measure progress towards something great. Knowing this, my mom gifted me a new book by two computer scientists focused on artificial intelligence, Kenneth Stanley and Joel Lehman called Why Greatness Cannot Be Planned; The Myth of the Objective. In it, they make the case that in complex domains, objectives may actually be getting in the way of achieving the exceptional. To demonstrate this, they developed a program called Picbreeder where you can "evolve" images. Each initially random image has a "genome". The program then generates ~15 permutations of that image based on its genome. You pick the most "interesting" one. And the process repeats until you produce an image you are satisfied with.

The above is an evolutionary lineage of a skull image discovered on Picbreeder. So what's interesting about it? Early images just look like blobs. The middle ones maybe have some abstract patterns. Only right at the end of the evolution does it look anything like a skull. With that, the authors propose a thought experiment. Imagine a government program whose objective is "Evolve a skull image on Picbreeder." To execute the government program, scientists dutifully develop a "skull-ness" metric that rates an image from 1 to 10 on how skull-like it is. At each generation, the government program keeps only the images that increase skull-ness and discards the rest. Can you see the problem? All the actual stepping stones to producing the skull score near zero on skull-ness. The key insight is simple. In complex spaces, the stepping stones to remarkable outcomes often look nothing like the outcome itself. Going back to our bonsai, if you only optimize for an end-goal, you prune away the weird intermediate forms you need to grow something great. It's been 10 years and I have not stopped being able to see that skull. It haunts the tech industry. My first meeting with it was Kevin Ryan, CEO of AlleyCorp. If you wanted to optimize for co-founding the leading company for a novel database architecture, where should you start? If you guessed Dilbert comics, congrats! You should start working on the skull-ness metric our fake government program needs.

Here are a few more classics: To build the default infrastructure for online video, start by paying women on Craigslist to upload dating videos to your dating site (Youtube). To control the internal chat systems for Silicon Valley, start by failing at building MMO games (Slack). To reinvent online gaming, start with physics education software (Roblox). But the real takeaway from all these stories is not just that heuristics fail us in complex spaces (like venture capital). It's that conviction is emergent and, once found, should be followed. After witnessing Dilbert sell out of their merch when they advertised it online, Kevin quit his corporate job, searched for the company (DoubleClick) he thought was going to scale online advertising, and became its CEO. At DoubleClick, Kevin and MongoDB co-founder Dwight Merriman witnessed how Oracle was expensive and failing to deal with the velocity of web-scale work loads. That gave them the conviction to keep doubling down on MongoDB for seven years before the company made meaningful revenue (read more on the story from Sequoia). Now DoubleClick's ~$3B sale to Google pails in comparison MongoDBs market cap of ~$30B. So where do we at Steel Atlas get our conviction, especially if you can't just plan for where it will take you?

Boiled down, conviction is how much more you believe something than others. When correct, it's how far ahead of the crowd you are. To get conviction though, we often joke that you can't be a blind person trying to describe the color blue. A blind person can learn all the right things to say about the wavelength of blue light, how it relates to the color red, what emotions it's associated with in culture. But there is a difference between describing and experiencing blue. We believe it's that seemingly squishy difference between describing and experiencing where real conviction emerges. And it is with that difference in mind that we intentionally structured Steel Atlas. Kevin's journey from Dilbert to MongoDB is about actually experiencing the future frustrations of others and having a willingness to step into the seeming unknown based on those experiences. When we thought about starting Steel Atlas, we had a decadal view of the geopolitical shifts and technological tailwinds behind the industrial economy. But this view needed grounding. We believed we needed to see blue, over and over again to be successful, to beat the crowds. This is why Steel Atlas is structured in such a unique way relative to most early stage funds. We are very concentrated. Our first fund will end up being 10 companies. Our second will be ~12. This means that we only make about one investment per quarter. Importantly though this gives us time. Time that we spend visiting ports and pipe factories, research facilities and reactors. Below is one of the most advanced machine tool shops in the world at CERN.

We travel across the world to do this (United Airlines is the real winner in this game). And we have spent time building high-trust relationships with the people that own and operate these industrial assets because we want to see through their eyes and experience what they experience. This is where our conviction comes from and why we are willing to go out on limbs that others might not. We went out on a limb in our first fund. We put 25% of it into nuclear companies at a time when it was not clear the US would ever approve a new reactor. One year ago, we even spoke on Bloomberg predicting what would unfold if Trump were elected in terms of nuclear energy. We said we expected de-regulation to drive investment and expedite timelines. As of today, nuclear companies are pushing to turn on reactors per Trump's executive orders by July 2026. One of them is our portfolio company Valar Atomics, a ~2 year old company that has already demonstrated a thermal version of their reactor and just closed a $130M Series A.

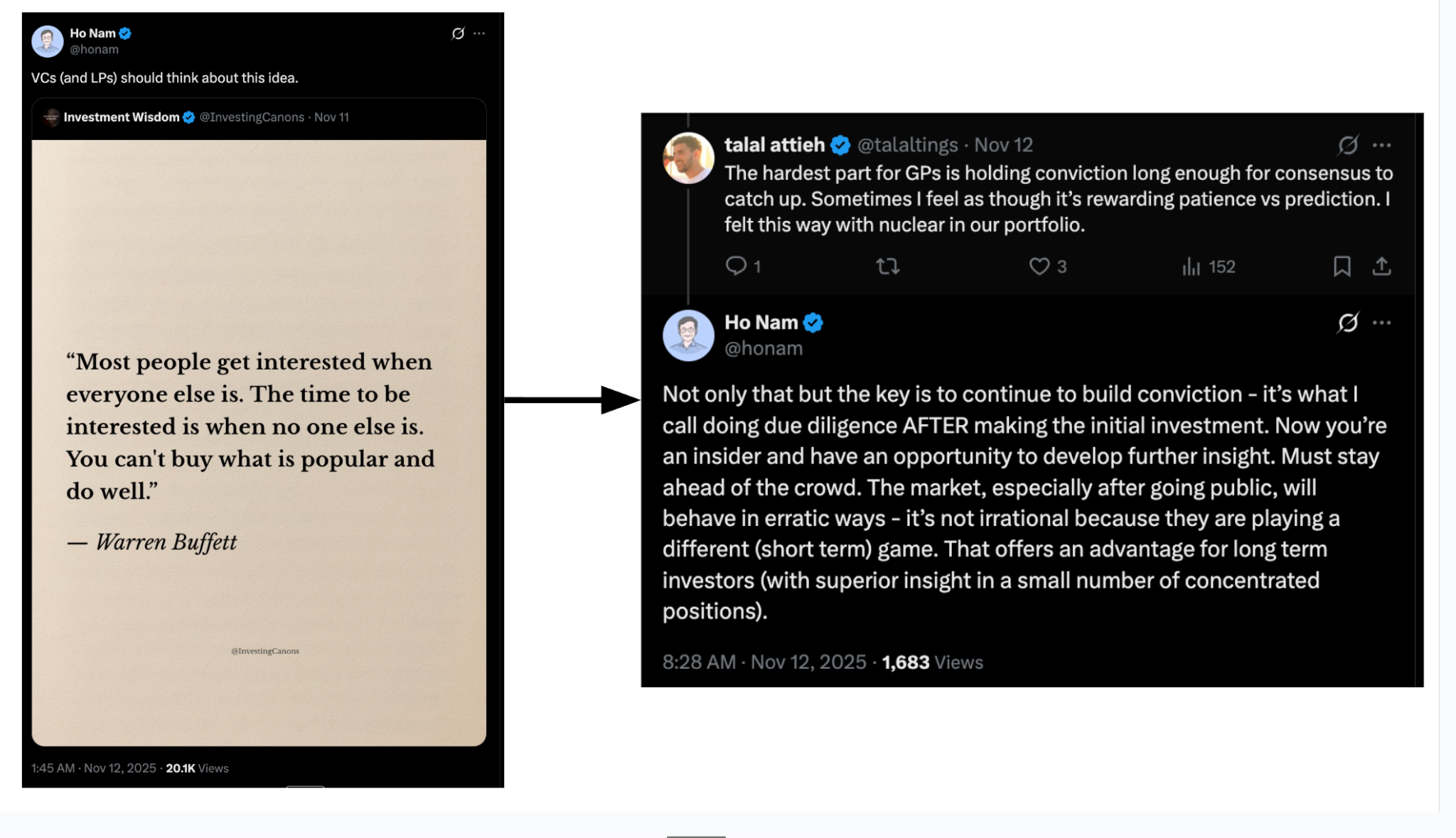

Importantly though, conviction is not static. The crowd is always chasing (or running away). As Ho Nam, the co-founder of Altos Ventures known for his ~$400M investment in Roblox that started out of $86M fund, said in an exchange with Talal on X, "... the key is to continue to build conviction - it's what I call doing due diligence AFTER making the initial investment." At IPO, Altos owned ~24% of the now ~$70B Roblox.

It's nice to make bets and have them pay off. But if you are too hands off they really are just bets. Investing means not only taking an active role in the outcome but consistently reflecting on what you got right and what you got wrong. What could you have known that you didn't? What did you think you knew that wasn't true? This is the work that builds confidence. A high conviction investor without earned confidence is just a gambler. Concentration allows you to stay close to your companies and do this work. New, growing companies experience the frontier of problems (like data backhaul in remote areas). They try new technologies. Some work. Some don't. They build things that in the future everyone should be able to buy. They source things from places they would rather not have to (like Russian radioisotopes). They develop new business models in one sector that may apply in others. This is the fertile ground of opportunity. But to see it (to see blue), you need to be close with those that are in it — seeing through their eyes. You need to feel what the industry is growing into. Ultimately, it is this experience that lets us keep on going out on our limbs into fertile territory.

When we led GenLogs' seed round in November of 2023, they were making a bold claim. By covering the entire US highway system with sensors to track trucks, they would develop the most advanced supply chain intelligence platform to serve brokers, shippers, carriers, insurers, hedgefunds, state / local law enforcement, the federal government and more. After all, every year, ~4M trucks move more than $10 trillion of goods across the US. Two years later, GenLogs is closing in on full coverage. It took more than just heroic logistics and sales to get these installed. It was a technical feat as well. Terabytes of data flow off these sensors. Sensors in remote areas with limited bandwidth across. Sensors that are subject to storms and power outages. Every missed truck is potentially lost value. GenLogs had to design their hardware platform in house. The critical component being the radio communication systems that not only determine whether those valuable images arrive on GenLogs servers but that monitor the health of the entire sensor system so they can be reset, patched, or repaired by the GenLogs Sensor Deployment team if needed. Although GenLogs sensor deployment is large today, it is only growing — expanding into ever more remote areas and countries with more bandwidth constraints necessitating communication systems that potentially utilize a changing array of radio spectrum (satellite, cell, wifi, etc) based on availability. And GenLogs won't be alone in this. We believe that they are showing the path to massive terrestrial sensor deployments across industrial use cases. More companies will face the same challenges as them. Unless integrated hardware and software products come out, each new company that follows in GenLogs' path will face the challenges associated with either 1) building in-house sensor communication systems or 2) adopting off-the-shelf systems that are too complex for non-experts to configure with integration costs that make resilient connectivity difficult. GenLog's had the expertise to build in-house. Others won't be so lucky. These companies will miss out on critical data when links drop and could struggle as they develop software to manage data prioritization policies and device health monitoring. Whether we are looking at companies developing early wildfire warning systems, mining revenue prediction platforms, or drones for the front lines, all of them want robust, integrated, communication systems. Developing the next generation of these could be one of the great horizontal opportunities in industrial technologies.

When we invested in Transmutex alongside USV and At One Ventures, it was clear that by developing the first commercially viable, ultra high power cyclotron you could position yourself as a critical player throughout the nuclear supply chain. Using these systems countries could breed domestic fuel supplies to avoid importing enriched uranium from Russia as well as massively minimize their long-term radioactive waste burden from scaled nuclear energy deployment. But that was not all. Transmutex's systems can be used to produce the next generation of advanced cancer therapeutics based on unstable radioisotopes. It thus exposed us to the global radioisotope supply chain. Right now, we heavily rely on Russia and China for high value isotopes through Rosatom's isotope arm (Isotope JSC) and the China Isotope & Radiation Corporation (CIRC). We procure medical nuclides like Lu-177, I-131, and Ac-225 to industrial Co-60 sources for sterilization. Western healthcare, defense, and energy systems are reliant on our adversaries for these scarce materials. We are living through the risk this creates with rare earth elements today which sit at the center of the US / China trade war. It's not hard to imagine radioisotopes playing a similar role in the future as isotopes themselves become gating inputs to advanced nuclear medicines, radioisotope thermoelectric generators (RTGs), and next-generation reactor systems. If rare earths were the leverage point for the last cycle of industrial policy, isotopes may be the leverage point for the next one. If we can secure and scale western isotope supplies, on the other side of that transition is a whole family of radioisotope-enabled products. That looks like nuclear medicines built on beta and alpha emitters — multi-billion-dollar drugs. Large RTGs (think of them like long lasting batteries) placed on the seabed alongside repeaters could bypass the shore-feed power thereby avoiding the thermal limits of today's undersea data cables and unlocking higher bandwidths between countries without requiring them to lay down new cables. These are just some of the possibilities that an abundant supply of radioisotopes could unlock.

You have to be constantly pruning, training your tree. This is the work of growing a firm, especially as it scales. For there is a certain sameness that comes with size, whether you are looking at big trees or big firms (can you remind me the difference between BlackRock and Blackstone?). A government bureaucracy looks very similar to a corporate one after all. If you want to continue to grow something one of a kind, you always have to be pruning, honing your conviction.

In bonsai, when you prune in one place, it drives more resources to another (potentially a useful lens for things like DOGE). By following, shaping, and supporting specific branches, you can grow something one of a kind. Although I find the big redwoods and sequoias magnificent, we want to be like one of Kunio Kobayishi's bonsai (all featured throughout this essay). All of Kobayishi's trees have a real presence. Even though the branches could have been grown in any direction, they seem as if they could not have been any other way. They have conviction about what they are and where they are going. And so do we.

Equipment financing and logistics for the reindustrialization of America

Highlight: Closed oversubscribed seed round and Neo Accelerator. Next Key Milestone: Full deployment of the underwriting engine and vendor API network in early 2026. Next Expected Round: Q2 2026

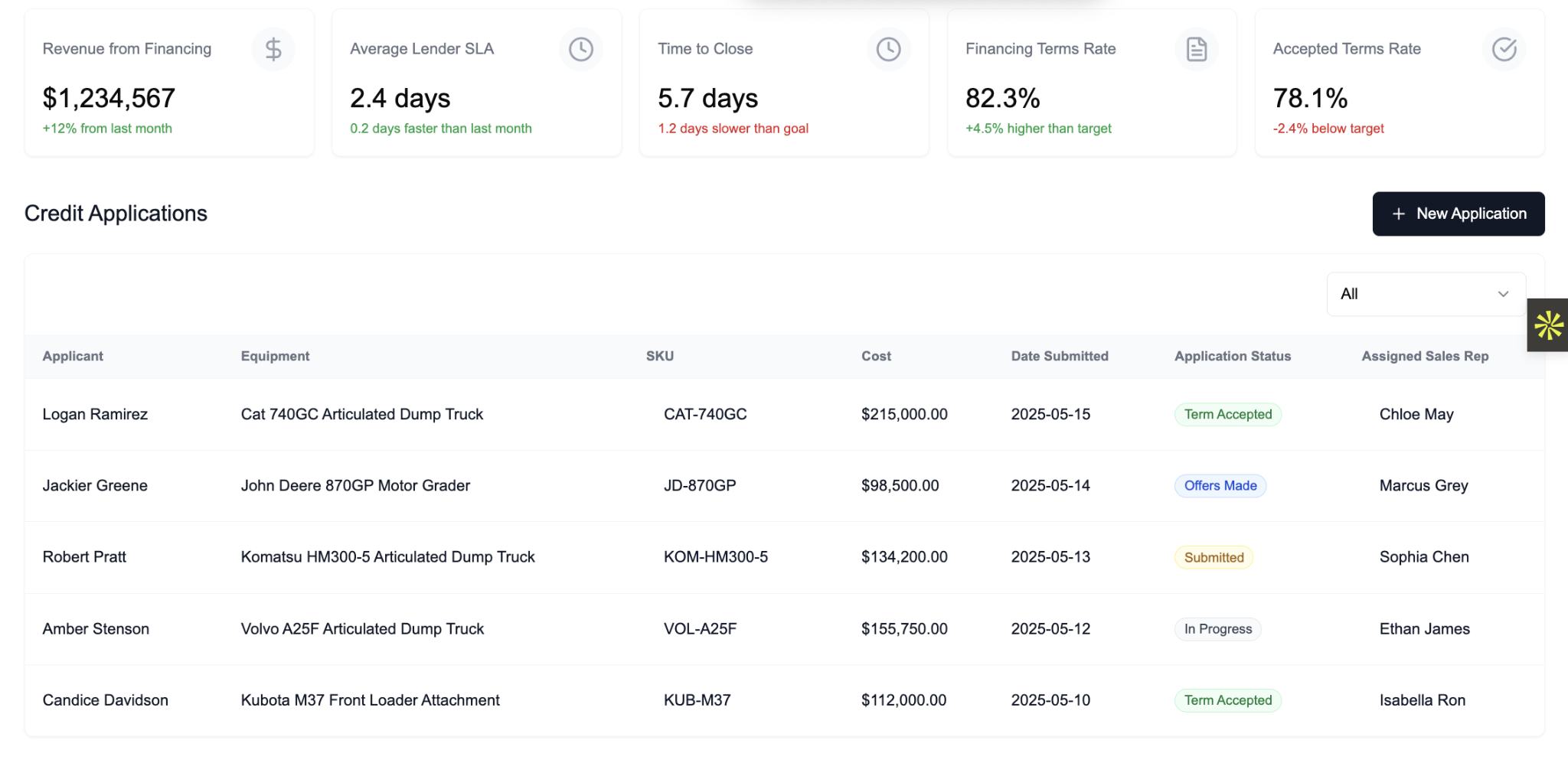

Substrate Industries accelerates equipment OEMs' sales by offering a white-label buy-now-pay-later system. Substrate approves ~95% of customers for 3-72 month terms in <1 day and pays vendors 100% upfront. Setup takes just 20 minutes. Today, only giants like Caterpillar and Haas offer in-house financing. This unlocks 20-30% more sales and 4-8x faster close rates. By underwriting at the machine level (not just the borrower level) and wiring funds to vendors in days, Substrate eliminates weeks-long cycles, opaque fees, and high decline rates that plague the $1.3T US equipment-finance industry.

Substrate builds the missing financing and logistics layer for industrial equipment in America. The company's vision unfolds in two phases. Phase I, the Digital Substrate, is an OEM-embedded financing engine that approves customers in under a day, pays vendors 100% upfront, and prices loans at the machine level rather than the borrower level. Phase II, the Physical Substrate, extends that intelligence into a shared refurb, logistics, and resale network — owning the full lifecycle from first sale to second life. Together, they form an integrated system for how industrial equipment is financed, moved, and monetized.

A Broken Market

Reindustrialization requires capital investment in machinery, but the US equipment-finance market is structurally misaligned with the economic reality of assets. Since the 2008 financial crisis, Basel II/III and post-crisis capital rules have treated the residual portion of a lease as 100% risk-weighted with no collateral recognition. The supplementary leverage ratio and liquidity coverage requirements further penalize long-dated assets. The result: banks exited leasing or rewrote programs into full-payout loans that assume zero residual value. For a manufacturer, this translates into a massive cost gap. A German shop can lease a $200,000 CNC machine for roughly $1,600 per month over its useful life. An American shop often faces $6,000-plus monthly payments on short, full-payout leases that misprice depreciation. The issue is not operator risk but regulatory design. Equipment financing drifted away from asset economics because the capital structure of banks could no longer hold residuals.

A Barbell of Friction

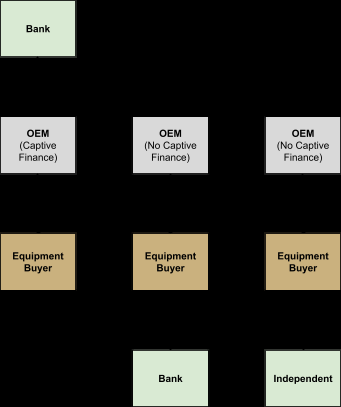

This distortion produced a barbell market. At one end, bank platforms such as Wells Fargo Equipment Finance or US Bank offer the cheapest rates but are slow, document-heavy, and restricted to perfect credits. At the other, independents and private-credit lenders approve quickly and handle complex "story credits" but at high coupons and fees. Large OEMs like Caterpillar or Deere operate full captive arms, while most mid-tier OEMs white-label bank programs or direct customers to independents. Smaller builders have no financing at all. The result is a landscape where buyers must choose between price and speed, and OEMs lose sales because they cannot extend affordable credit. For most equipment purchases, the financing process remains opaque, slow, and detached from the true economics of the machine.

Complexity That Kills Scale

Industrial equipment is inherently heterogeneous. A single Haas CNC model can be configured thousands of ways — different envelopes, spindles, tool changers, and software packages — each with unique earning power and resale value. Traditional underwriting depends on borrower credit rather than asset performance because no scalable system exists to evaluate each configuration. The diversity that makes machines productive for manufacturers makes them unmanageable for financiers. Underwriting more equipment types used to require hiring more analysts. As a result, lenders cannot price the machine's useful life, utilization, or remarketing path. This forces short tenors, high rates, and low residuals, choking modernization across the small- and mid-market industrial base.

What Stakeholders Want

For OEMs, every sale is a financing problem. They want faster close rates, larger baskets including automation and service, funding within days, no operational overhead, and better telemetry on their installed base. For buyers, the wish list mirrors that: lower all-in cost, certainty and speed, integrated insurance and service, and one counterparty across brands. The gap is not demand — it is infrastructure. The market needs a new financing layer with the data access of an OEM, the independence of a non-bank lender, and a software cost curve that scales across equipment categories.

The Digital Substrate

Substrate's first phase delivers this new layer. The platform embeds directly inside OEM quote flows, offering instant credit decisions and automated payouts within 24 to 48 hours. By pricing at the machine level, Substrate aligns payments with actual depreciation and utilization. OEMs can offer "buy now, pay later" terms to nearly all customers without building a captive finance arm. This OEM integration grants Substrate a structural data advantage: configuration details, install notes, service histories, and eventually telemetry streams. Over time, this dataset trains an AI-based underwriting engine that outperforms borrower-only credit models. The company earns revenue from SaaS fees tied to OEM size and a 1-2% origination take rate on financed volume. Because model development and platform costs amortize across OEMs and equipment categories, each additional asset type lowers marginal cost. Substrate's cost of underwriting decreases as its diversity increases — the inverse of the current system. That inversion allows it to price capital more accurately, fund vendors faster, and give buyers longer, cheaper terms.

From Digital to Physical

Once underwriting intelligence matures, Substrate's digital rails enable a physical network. The Physical Substrate aggregates OEM-certified refurb partners, regional consolidation hubs, middle-mile logistics, insured storage, and a vendor-backed resale marketplace. Equipment can be redeployed, upgraded, or liquidated with predictable economics instead of dumped at auction. A single counterparty manages financing, delivery, insurance, and resale. Recoveries rise sharply: early cancellations can be redeployed to new buyers; upgrades flow to late adopters at pre-set floors; and failed machines are salvaged for OEM parts channels. The physical layer closes the loop, feeding real-world data back into underwriting and creating a compounding advantage over fragmented independents. This network only works with cross-OEM scale. Substrate's Phase I integrations supply the volume to amortize refurb centers and logistics lanes across multiple brands (mills, robots, compressors, lasers) achieving density no single captive could. The long-term result is a Carvana-like national infrastructure for industrial assets, but built in partnership with OEMs rather than against them.

Market Potential

The US machinery subsector (NAICS 333) shipped roughly $450B of equipment in 2024. Assuming 25% addressability, about $100B of annual volume fits Substrate's model, with a $25B secondary market on top. Even limited penetration yields venture-scale economics in Phase I. Phase II multiplies that upside with marketplace and ancillary revenue from insurance, warranty, and service. Phase I alone can sustain a $100M+ revenue business under a $30M entry valuation. Phase II extends the reach to hundreds of millions in revenue potential, backed by durable data moats and OEM cooperation.

Founder and Execution

Kelvin Yu, Substrate's founder and CEO, combines rare fluency in AI, industrial policy, and venture execution. His background spans In-Q-Tel, Anthropic, the US House of Representatives, and Princeton Computer Science. Within months, he secured design-partner LOIs representing about $50M in annual financing volume and built a lender network covering $1K to $20M tickets. His writing on techno-industrial policy circulates widely among OEMs and investors, reinforcing credibility with partners.

Yu's strategy mirrors how winners of the AI land grab operate: own the workflow, capture proprietary data, and tie model improvements directly to business outcomes. As foundation models advance, Substrate's residual pricing and fraud filters improve automatically while inference costs stay flat. The company sells outcomes (lower loss rates and faster throughput) rather than metered AI tokens. Each model upgrade translates into better margins, not higher cloud bills. Substrate's mission aligns with the core challenge of reindustrializing America: access to efficient capital. When small and mid-sized manufacturers can finance modern equipment at near bank-cost with approvals in days, clusters grow and technology diffuses faster. Aligning payments with true residual value drives broader adoption of automation, robotics, and precision machinery.

Bringing automated knitwear manufacturing back to America

Highlight: First 3D knitting machine arrived at 13K sq ft facility in LA. Next Key Milestone: Begin live production and sampling runs for potential launch partners including Ralph Lauren, Skims, and Revolve. Next Expected Round: Seed Extension Q4 2025

Framework Automation is building America's next great industrial company, reshaping today's $260B knitwear market with a software-defined manufacturing platform that fully automates production. Their platform eliminates inventory and supply chain risk while achieving cost parity with Asia today. The US currently produces most of the world's cotton and polyester. But these raw materials are shipped abroad and made into clothing due to lower labor costs. Using 3D-knitting, Framework is eliminating this labor arbitrage to bring on-demand clothing manufacturing to the US.

Framework entered Q3 executing on its transition from design to production. The company established its first operational facility in Los Angeles, built a world-class engineering team, and laid the groundwork for scaled, automated knitwear manufacturing in the United States.

Facility Commissioning

Framework took possession of its first factory in Culver City in Los Angeles. The 13,000 sq ft site is purpose-built for automation and throughput, with electrical capacity sufficient for multiple banks of whole-garment knitting machines and integrated dyeing and finishing systems. Once fully ramped, this facility supports up to $7.5M in annual production capacity, equivalent to roughly 350,000 finished units per year.

The LA location was chosen for proximity to brand partners, engineering talent, and investors. Longer term, Framework plans to replicate this factory model in Texas or the Carolinas to capture lower energy costs and proximity to raw cotton. The LA site serves as the technical reference plant for process validation and customer demonstrations. By the end of the quarter, the lease was finalized, basic remodeling completed, and the first equipment deliveries scheduled for late September. Utilities and electrical systems were already aligned with operational needs, allowing Framework to begin sampling immediately upon machine installation.

Equipment and Supply Chain

Framework finalized most of its capital equipment purchases during Q3. The first 3D whole-garment knitting machine arrived at the end of September, marking the start of live sampling and production runs. These machines, sourced from Shima Seiki, form the backbone of Framework's software-defined manufacturing system: automated, zero-waste, and capable of producing complete garments from yarn in one step.

Upstream, the company secured a strategic supply relationship with a major spinning and dyeing mill in Turkey, providing access to high-quality yarns on one-week lead times. This arrangement delivers the flexibility typically associated with vertical integration while avoiding large capex commitments. Turkey's low air-freight rates fit within Framework's total-cost model and maintain pricing competitiveness with Asia. Together, these partnerships anchor Framework's vertically integrated supply chain: cotton sourced domestically, yarn finished in Turkey, and knitting, finishing, and fulfillment in Los Angeles. This structure provides cost control and supply continuity at each stage of production.

Team Expansion

Q3 marked Framework's most significant period of hiring to date, adding core technical and operational depth.

Evan Bender – Founding Manufacturing Engineer. Evan built the engineering and manufacturing organization at Sheertex (backed by Founders Fund and H&M), scaling from zero to hundreds of machines and hundreds of millions in revenue. He is one of the most experienced engineers in North America in industrial-scale knitwear automation.

Sarah Choi – Operations Lead. Sarah previously served as Chief of Staff and BizOps Lead at Stensul, a Series B SaaS company. Her earlier roles at BMO Capital Markets and Great Hill Partners bring financial and organizational discipline critical for scaling operations.

Sam Strongin – Machine Learning and Robotics Engineer. Sam holds a master's degree in computer vision and spent six years at the Air Force Research Lab conducting classified AI and robotics research. He now focuses on automation, predictive maintenance, and dynamic scheduling within Framework's factory orchestration system.

These hires followed two critical additions in late June: Emily Keller (Knitwear Production), a 15-year veteran of Shima programming at Tailored Industry, and Mustafa Tornaci (Textile and Materials), former managing director of a large Turkish knitwear mill with a master's in textile engineering. Together, the team spans manufacturing engineering, AI, and textile science, positioning Framework to integrate advanced automation with deep domain expertise in apparel production.

Software and Hiring Pipeline

Recruiting for full-stack software engineers remains active, with a goal of adding three LA-based hires in the coming quarter. Five strong candidates are already in process. These engineers will expand Framework's software orchestration layer, which translates design files into production-ready machine instructions, optimizes real-time scheduling, and tracks each garment from yarn selection to shipping. This digital backbone differentiates Framework from traditional contract manufacturers. The company is building a vertically integrated system that merges design, production, and fulfillment under one digital platform. Future releases will automate cost quoting, SKU versioning, and ERP synchronization with brand customers.

Customer Pipeline

Framework continues to see strong inbound interest from major apparel brands. Sampling commitments are already secured from Skims, Revolve, Bloomingdale's, Theory, Cuts, and Azazie, all of whom are waiting for the first production runs out of Los Angeles. The company also met with Ralph Lauren's Head of Product Innovation, who confirmed the brand's lack of any scalable domestic knitwear partner. Ralph Lauren expressed strong interest in Framework's platform, viewing it as strategically aligned with its "Made in America" initiatives leading up to the Los Angeles 2028 Olympics. Once Framework begins sampling, Ralph Lauren is prepared to initiate trial runs pending competitive costing. We expect this to begin in Q4. Early traction with these brands validates Framework's thesis that major labels are ready to near-shore production if cost parity and flexibility can be achieved. The company expects several sampling agreements to convert into paid pilot orders before year-end.

Supply Chain and Operations

In parallel with facility setup, Framework completed vendor qualification and procurement planning for its first production wave. The Turkey yarn and dyeing partnership is operational and performing within target cost bands. Domestic suppliers for packaging, warehousing, and logistics have been identified to maintain rapid fulfillment. Framework's manufacturing flow links yarn storage, dyeing, knitting, finishing, and distribution under one roof, transforming traditional batch-based processes into a single continuous flow with the Shima machines at the center. Each machine can produce a finished garment in 50-70 minutes with no manual labor, no cutting or sewing, and near-zero waste. The goal is to automate yarn from entry into the factory, sorting and picking yarns using AutoStore automation, all the way to treatment, washing and drying without a single human involved. This configuration allows Framework to offer customers true on-demand production at scale. Instead of purchasing finished inventory months in advance, brands will purchase undyed yarn and pay the balance only when garments are produced and shipped. This model cuts inventory holding costs by up to 80% and enables near-100% sell-through rates.

Strategic Outlook

Framework enters Q4 focused on commissioning its Los Angeles factory and validating full system performance. Immediate priorities include:

1. Machine installation and commissioning to begin sampling for pilot partners.

2. Hiring three additional software engineers to complete the factory orchestration platform.

3. Establishing baseline economics using live production data to confirm cost models and throughput assumptions.

4. Expanding customer sampling to move from prototypes to recurring production orders.

Real-time supply chain intelligence powering logistics, insurance, and government

Highlight: USDOT pilot expanded to a $250K paid contract, marking GenLogs' first federal revenue. Next Key Milestone: Convert the pilot into a multi-year USDOT contract in early 2026. Next Expected Round: $30M Series B by Q4 2025

GenLogs is a supply chain & logistics technology company that uses proprietary data + AI to track and analyze US long-haul freight in real-time. In the US, there are 27K brokers tasked with moving $1T of goods each year by placing loads from shippers on one of the 4M trucks operated by 500K individual carriers. Today, brokers attempt this market matching without the single most important piece of data for doing it efficiently: the location of each of these trucks at any point in time. Vast amounts of data are being generated by the trucking industry daily, including mobile-ad-IDs and electronic logging devices. The issue is that this data is anonymized and thus not linked to a specific truck. The same problem applies to satellite imagery and traffic camera data that only reveal the presence of a truck at a certain time and place without identifying the specific vehicle (DOT number, carrier name, etc). GenLogs has developed a proprietary approach for solving this problem scalably and without need for permission from individual truck owners. By deploying only sensors across the US to act as virtual gates, GenLogs is able to generate a distinct ID for each truck that passes a sensor that can be used to deanonymize the previously mentioned datasets. This breakthrough allows GenLogs to passively track all trucks in real-time using a fusion of disparate datasets, including satellite data, mobile ad IDs, and public traffic cameras. Using this data, GenLogs is developing best in class tools for the trucking industry.

Q3 marked a structural inflection point for GenLogs. Despite the freight market's continued weakness, the company entered the quarter with fantastic momentum across every major vertical (freight, insurance, and public sector) and exited it with expanding recurring revenue, deepened federal validation, and an increasingly defensible sensor network. The business has shifted from proving product-market fit to scaling execution.

Sales and Market Expansion

Revenue grew 36% quarter-over-quarter, adding $1.4M in ARR. The customer base increased by 25 accounts to a total of 65, backed by a $30M qualified pipeline spanning freight brokers, insurers, shippers, and government entities. Beyond ARR, GenLogs booked $570K in non-recurring revenue, mainly from sensor deployments at ports and other infrastructure sites, bringing total contracted value to $6.6M. GenLogs ended the quarter with $13.6M in cash after burning $1.1M, implying a burn multiple of 0.6x, an unusually efficient ratio for a company scaling at this pace.

The team has deliberately diversified beyond mid-market brokers to larger shippers and insurers, a transition accelerated by new enterprise AEs and a channel strategy led by the CRO. Strategic partnerships with SONAR and AWS are expanding reach and integration depth. With SONAR it's through embedded capacity data within its freight analytics interface and AWS via inclusion in its partner network to co-market joint solutions and allow customers to fund GenLogs subscriptions via AWS credits.

Product Progress

The company enters Q4 with the most complete version of its platform to date. The upcoming Carrier Compliance Suite (now in late-stage testing) consolidates fraud detection, verification, and compliance workflows at a time when legacy competitors like Highway are struggling. Its launch is expected to meaningfully expand ACVs and accelerate replacement cycles from legacy systems. Parallel R&D efforts are enhancing fleet characterization by applying computer vision and machine learning across GenLogs' two-billion-image (and growing) historical archive. These models enable richer analytics on fleet age, behavior, and maintenance trends, feeding into new data products for insurers, creditors, and equipment suppliers. The company's TAM has expanded well beyond freight brokerage into adjacent $1B+ information markets such as heavy-duty truck repair, parts distribution, and warehouse operations.

Sensor Network Expansion

Sensor growth remained a cornerstone of GenLogs' compounding advantage. The network expanded 32% during Q3, from 280 to 371 sensors, comprising 330 GenLogs-owned Trident units and 41 third-party cameras. Coverage now extends across nearly 90% of all active for-hire carriers in the US. The company remains on track for 600 operational Tridents by 2026.

Public Sector Breakthrough

GenLogs' government business matured from pipeline to revenue in Q3. The company recorded its first public-sector dollars and secured validation at the federal level. A $25K proof-of-concept with the US Department of Transportation (USDOT) evolved into a 90-day, $250K paid pilot. This is the most strategically important federal engagement in the company's history. The pilot serves as the foundation for a potential seven- or eight-figure annual contract in 2026. At the state and local level, GenLogs closed its first law-enforcement contract and has two state deals pending signature, totaling $44.5K in near-term revenue. The pipeline has grown to $9.6M, representing over two dozen qualified agencies. To accelerate adoption within the constraints of public funding cycles.

Strategic Outlook

The management team now views GenLogs as a multi-vertical intelligence company rather than just a freight-tech platform. The core dataset — real-time, verified truck observations — supports use cases across logistics, insurance, infrastructure, and law enforcement. Each incremental sensor adds not only coverage but compounding informational advantage, expanding the company's addressable market and deepening its moat. Internally, leadership is reinforcing operational rigor. Q3 saw the hiring of Matt Bujnicki as VP of Finance and expansion of the enterprise sales team. All business lines, including the public sector, are now managed through Salesforce with consistent forecasting methodology, replacing spreadsheet-based tracking. This operational unification allows the company to present an integrated forecast and pursue synchronized sales across verticals.

GenLogs closed Q3 as a stronger, more diversified company. ARR doubled since spring, burn efficiency improved, and the company converted government pilots into paid contracts while expanding private-sector traction. The freight downturn that once tested the model has instead hardened it. With over 370 sensors, a validated federal foothold, and a rapidly scaling product suite, GenLogs now stands as the de-facto intelligence layer for North American trucking and is preparing to extend that dominance into adjacent data markets and public infrastructure intelligence in 2026.

Pioneering high-temperature gas reactors and advanced nuclear fuel production

Highlight: Valar raises stealthy ~$57M Series A on $200M pre-money valuation. Next Key Milestone: Complete TRISO fuel sourcing. Next Expected Round: $300M Series B by early Q2 2025

Valar Atomics is pioneering a breakthrough in energy by combining proven High-Temperature Gas Reactor (HTGR) technology with a novel business model to create synthetic, net-zero fuels. Led by Isaiah Taylor, an autodidact and serial entrepreneur, and supported by Chief Nuclear Officer Mark Mitchell, a leading expert in TRISO-fueled reactor design, Valar's integrated approach removes traditional barriers to large reactor-deployments via a business model that enables single-sites with hundreds of reactors. With the potential to disrupt both energy and industrial sectors in need of high temperature heat, Valar is poised to deliver clean, competitively priced synthetic fuels at scale — unlocking a trillion-dollar opportunity in the global energy market.

Series A Funding

During Q3, Valar closed a stealth Series A financing round of $57.79M on a $257.79M post-money valuation, led by Snowpoint Ventures, the fund founded by former Palantir executives. For context, Steel Atlas invested $1.25M in Valar roughly a year earlier at a $30M post-money valuation, securing an early position in the company's trajectory before federal programs validated its approach. You can find the 5.8x (500%+ IRR) markup reflected in the financials delivered to you. A second tranche of the Series A, projected at roughly $60M, is expected to close in Q4. The proceeds will fund the company's TRISO fuel line development, Utah facility buildout, and continued advancement of the DOE pilot and Janus programs (described below).

DOE Nuclear Reactor Pilot Selection

Valar Atomics' inclusion in the President's Accelerated Nuclear Program and the Department of Energy's Reactor Pilot selections marked a significant leap in federal validation during Q3. The program, unveiled under Executive Order 14301, establishes an explicit national goal: achieve advanced reactor criticality by July 4, 2026. The DOE followed by naming 11 companies (including Valar) for its New Reactor Pilot Program, aimed at deploying advanced reactors on an accelerated timeline outside national labs. The two initiatives form the centerpiece of the administration's plan to rebuild domestic nuclear manufacturing, compress regulatory cycles, and restore the US industrial base for energy resilience. Valar's selection reflects both technical readiness and policy alignment. Its helium-cooled, TRISO-fueled reactor design was engineered for manufacturability and short build cycles — precisely the characteristics prioritized under the DOE's new authorization pathway, which operates within DOE oversight rather than through a full NRC licensing process for early pilots. This shift redefines how private nuclear projects reach first power, enabling iterative development and real-world testing.

In July, Valar hosted US Secretary of Energy Chris Wright at their Los Angeles headquarters for a detailed review of progress toward the July 4 milestone. The Secretary emphasized the administration's intent to secure "cheap, reliable American energy," and Valar demonstrated the hardware-level progress of its WardZero prototype. The meeting underscored the administration's reliance on companies that can produce measurable physical results rather than extended paper studies.

Valar completed five months of heat and pressure testing on the WardZero prototype and two maintenance outages designed to validate component durability under high-temperature operation. These tests informed design refinements now being integrated ahead of full-scale qualification at the Utah facility. The company's pace of iteration reflects its intention to prove readiness within the DOE's accelerated pilot window. The transition to Utah marks the shift from engineering prototype to pre-deployment qualification.

Department of Energy Advanced Fuel Line Pilot Selection

In parallel with its reactor recognition, Valar was selected in September for the DOE's Advanced Fuel Line Pilot Program, joining three other firms tasked with rebuilding US capacity for high-assay low-enriched uranium (HALEU) and TRISO fuel production. This initiative addresses one of the most acute vulnerabilities in the US energy supply chain: dependence on foreign enrichment and fabrication. Valar's inclusion provides a critical vertical integration advantage. By developing its own TRISO fuel line, the company secures control of the core input to its modular reactor systems while positioning itself as a supplier to other advanced reactor developers. The project includes technical collaboration with the DOE and cost-shared support for pilot-scale fabrication infrastructure. This development deepens Valar's strategic moat. Fuel independence ensures reliable material supply for future defense and industrial customers while aligning with the federal mandate to localize critical manufacturing. For Valar, this dual capability (hardware + fuel) creates the foundation for a vertically integrated nuclear manufacturing enterprise that we envisioned when investing at Seed. The combination of the Reactor Pilot and Fuel Line Pilot programs places the company within the government's top tier of advanced nuclear developers positioned to reach deployment readiness by 2026 - an unmatched timeline in nuclear globally.

US Army Janus Program

The US Army's Janus Program emerged this quarter as the most direct commercialization pathway for Valar's test modular reactor (WardZero) that was originally a prototype reactor thought to be too small to commercialize. Jointly managed by the Army and DOE, Janus seeks to deploy small, transportable reactors (each below 20MW) to power forward operating bases and remote installations by 2028. The program's specifications align precisely with Valar's prototype reactor architecture: a high-temperature gas reactor capable of delivering both electricity and process heat in a containerized form factor. Valar has confirmed its intention to bid under Janus, positioning its system as mission-ready for defense applications requiring mobility, resilience, and low logistics demand. The WardZero prototype, which has demonstrated thermal output and pressure stability under DOE oversight, provides a direct technical basis for qualification. The company's selection under the DOE Fuel Line Pilot further strengthens its bid, as Janus requires reactors paired with reliable domestic fuel production. If selected, Valar could achieve first field deployment within two years of reactor criticality. Even prior to contract awards, its participation in the Janus process reinforces the credibility of its design and expands its visibility within the federal energy ecosystem. The company's trajectory now parallels that of earlier dual-use technology firms, developing first for government validation before scaling to industrial markets.

Utah Facility Groundbreaking

In late September, Valar broke ground on its first full-scale facility at the San Rafael Energy Research Center in Emery County, Utah. The site will host the company's first operational prototype and serve as a long-term testing and qualification hub for commercial modules. The groundbreaking, attended by Utah Governor Spencer Cox, other state officials, DOE representatives, and local industrial partners, marks the physical transition from laboratory development to deployment infrastructure. The Utah location provides access to skilled labor, existing nuclear research infrastructure, and supportive state policy. Valar plans to construct a high-temperature test loop and containment systems capable of handling the operational conditions of its modular reactor line.

Orbital debris detection enabling affordable satellite insurance

Highlight: ODIN secured its first commercial agreement with Arcusys and ESA. Next Key Milestone: Completion of the European Space Agency's €230k XL Sensor contract, unlocking an automatic follow-on contract of €2 million + ODIN as qualified supplier for future missions. Next Expected Round: Series A in Q2 2026

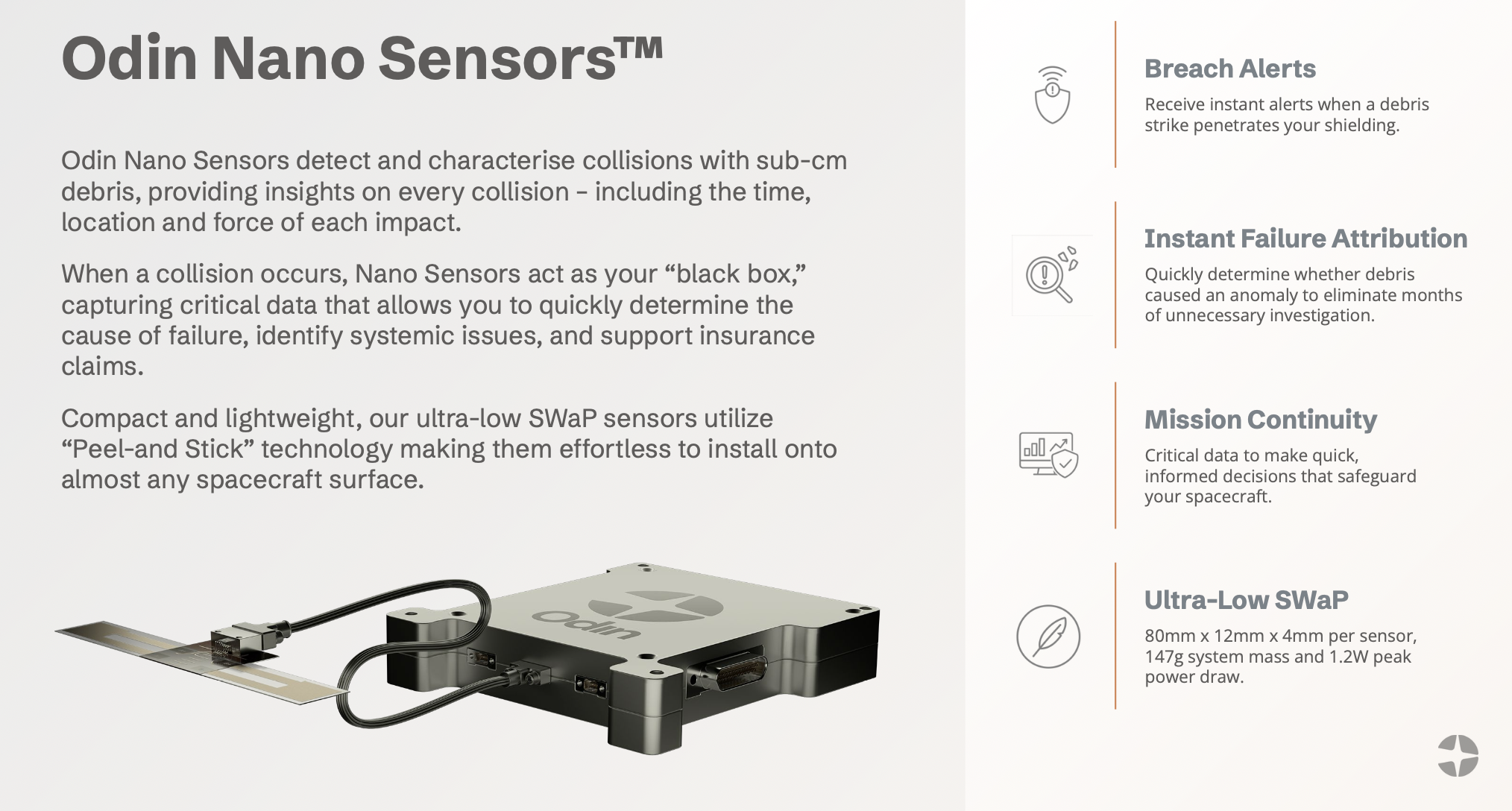

ODIN Space solves the exponentially growing threat of orbital debris, where untrackable materials travel at 10x rifle speeds destroying billion-dollar satellites and constellations. With their proprietary Nano Sensors developed by CEO, Dr. James New during his time at NASA, ODIN detects previously invisible sub-centimeter debris. In partnership with Lloyd's of London, ODIN's sensors are enabling the first data-driven satellite insurance products that are 10-100x cheaper than current alternatives. With only 3-5% of satellites insured today due to high premiums, ODIN is unlocking mass-market satellite insurance, representing a $10B+ annual revenue market opportunity by 2030.

ODIN Space entered the third quarter with a clear mandate following the close of its seed round earlier in the year: convert early customer traction into signed commercial contracts, advance technical integration of the Nano Sensor platform, and expand the team to accelerate go-to-market readiness. Across Q3, the company delivered meaningful progress on all three fronts, establishing commercial validation, government engagement, and technical credibility that position it well heading into year-end.

Commercial Traction

The single most significant milestone of the quarter was ODIN's first commercial agreement in principle with Arkisys, a satellite operator deploying a multi-satellite constellation. Negotiations are in the final stage, with pricing well above prior expectations. The hardware portion of the contract is structured at $50,000 per satellite, with 50% payable upfront and 50% upon delivery. Estimated build cost, inclusive of new cabling and connectors, is roughly $25,000 per unit, giving ODIN positive working capital and healthy gross margins from the outset. In addition to hardware, Arkisys will pay $30,000 annually for data services derived from ODIN's Nano Sensors. These services include diagnostics, debris-impact alerts, and telemetry analytics that enable the operator and its insurer to assess orbital risk in real time.

The Arkisys contract structure represents an important design choice for ODIN's business model. Rather than a cancellable subscription, the company is structuring multi-year fixed contracts (typically three years) with annual payment options. This allows ODIN to record forward revenue and reduce churn risk while providing customers payment flexibility. Steel Atlas advised ODIN to itemize the service components within the data offering to enable future expansion of pricing as new analytical features come online. That modular pricing framework is now being embedded in the commercial contract template, with legal drafting underway by ODIN's space-sector counsel.

On the government side, ODIN finalized and commenced execution of a €230,000 contract with the European Space Agency (ESA) to design and test its XL Sensor panels. This eight-month project represents the first formal government validation of ODIN's large-format debris detection hardware. Upon successful completion, ESA has outlined an automatic follow-on phase valued at approximately €2M for a dedicated CubeSat mission integrating ODIN's technology. The long-term ambition, under discussion, is a constellation of debris-mapping satellites for ESA, a potential multi-tens-of-millions program. Work under the initial contract began in July and remains on schedule. Together, the Arkisys and ESA projects give ODIN nearly half a million dollars in contracted or committed revenue, its first tangible proof of commercial and institutional demand. Management now targets $1M in contracted revenue as a baseline for the upcoming Series A.

Technology Progress

The company's core Nano Sensor continued to evolve rapidly through the quarter. The engineering team successfully miniaturized the sensor stack to under three millimeters in thickness and introduced a self-adhesive backing, allowing simple "peel-and-stick" integration onto satellite panels. The new design reduces mass, simplifies installation, and demonstrates ODIN's core thesis that orbital debris sensing can become a non-intrusive standard component. Early demonstrations at the SmallSat conference in Utah validated this assumption: multiple operators immediately asked to install the sample units on existing satellites, reinforcing the market's appetite for low-friction integration.

In parallel, ODIN's newly contracted systems engineer (formerly with NASA, ESA, and the UK Ministry of Defence) has begun developing standardized integration and qualification documentation for satellite OEMs. This initiative aims to eliminate the friction that often delays component adoption by providing operators with pre-approved mechanical, electrical, and data interface specifications. The engineer is also designing a benchtop verification rig that enables a "tap test" on integrated sensors prior to launch, ensuring full functionality. These small but critical steps strengthen ODIN's reputation as a reliable subsystem partner within the conservative aerospace supply chain. The XL Sensor program with ESA runs on a separate but complementary track. The larger dual-panel format expands data capture capability, laying the groundwork for future "ODIN Scout" satellites — stand-alone spacecraft that can survey orbital lanes and detect debris ahead of high-value assets like space stations or large constellations. Management, guided by Senior Board Advisor Steve Young, sees potential for these Scouts to serve as forward reconnaissance for billion-dollar orbital infrastructure projects such as Voyager's planned commercial stations. Each Scout could command multi-million-dollar contract values while leveraging the same core sensing IP. Beyond hardware, ODIN has initiated integration discussions with Gamma Space, a provider of deployable drag-sail systems used for satellite de-orbiting. Embedding ODIN sensors within these large drag surfaces would enable continuous data collection during de-orbit maneuvers, creating passive "data harvesters" that generate debris field maps as satellites re-enter. The concept could extend ODIN's coverage to thousands of orbital descents per year and produce a high-margin secondary data product for sale to agencies and insurers.

Team Expansion

ODIN made strategic hires and additions this quarter that materially strengthened its technical and commercial execution. The most visible was the appointment of Steve Young, President of Satellite Missions at ICEYE, as Senior Board Advisor. Young's two-decade track record in scaling ICEYE from startup to global radar-imaging leader brings deep commercial and government network access. He has already facilitated technical collaboration between ODIN and ICEYE's engineering teams and helped shape the company's tiered customer segmentation strategy.

Operationally, ODIN added a Sales Operations Manager who previously held commercial operations roles at ICEYE and Nature Analytics. Initially contracted part-time, she has proven instrumental in building the company's CRM infrastructure, refining pipeline processes, and coordinating marketing materials. She joins full-time in October. On the technical side, ODIN brought in systems engineer Steve Ringler on contract to build the integration documentation suite and lead space-qualification testing. Both hires demonstrate management's disciplined approach to balancing capability growth with capital efficiency. The next key role in recruitment is a VP of Sales with a proven book of relationships across satellite operators, insurers, and brokers. ODIN has a long list of roughly thirty candidates and expects to make the hire before year-end. The timing aligns with completion of new branding, website launch, and marketing collateral, ensuring the incoming executive can immediately convert awareness into sales activity.

US Expansion

During Q3, ODIN completed incorporation of ODIN Space Inc. in Delaware, with a physical registration in Orange County, California. This US entity is a critical bridge to government and defense contracts, as well as to insurers operating from US jurisdictions. The company is now pursuing registration on SAM.gov and assignment of its CAGE code to qualify for federal procurement (crucial for US space companies). To accelerate US business development, ODIN has brought in advisor Rob Zitz, a former senior US intelligence official with deep defense contacts. Zitz is already facilitating introductions within the US Department of Defense and intelligence community to explore applications of ODIN's sensors in space-situational awareness and asset protection.

The corporate "flip" to a US top-co structure is managed by Dentons. Tax assessments and National Security Investment Act clearance are expected before year-end. Once complete, all SAFEs from the seed round will convert into the new Delaware parent, simplifying future US fundraising and government contract eligibility.

Market Engagement and Pipeline

ODIN's commercial pipeline now spans three tiers of customers:

Tier 1 – large infrastructure and space-station projects such as Voyager, where ODIN's XL Sensors and potential Scout satellites would provide high-value orbital intelligence services.

Tier 2 – established satellite constellations including ICEYE, Spire, and EnduroSat, which can adopt the Nano Sensor as a subsystem across multiple spacecraft.

Tier 3 – early-stage startups and CubeSat operators that provide rapid-cycle deployments and data volume, seeding the insurance dataset and building market references.

This segmentation enables ODIN to tailor contract structures and pricing. Smaller operators will receive discounted terms in exchange for early data rights, while Tier 1 customers represent long-cycle, high-margin strategic wins. The company's target remains to convert one customer in each tier within the next six months. Management has also begun leveraging Steve Young's insight into ICEYE's customer base. Several governments, including Poland and Greece, are negotiating large imaging-satellite purchases from ICEYE. ODIN is using these touchpoints to approach the same buyers, positioning its sensors as a requirement within those procurements. ICEYE has confirmed that if an end customer requests ODIN sensors, they will integrate them without hesitation — a potentially powerful demand-pull dynamic. At quarter-end, ODIN had closed $3.25M for its seed round, with strong inbound interest from additional investors but a deliberate decision to limit dilution. Current cash provides a runway exceeding 18 months at planned burn, and with revenue now under contract, ODIN is comfortably capitalized to reach Series A.

Operational Highlights

On the insurance ecosystem front, ODIN continues close coordination with WTW (Willis Towers Watson) to structure its first "collision-only" policies leveraging ODIN data. This model, validated in previous reference calls with WTW executives, is seen as the bridge product that could re-open the stagnant space insurance market by offering affordable, named-peril coverage. Progress on the ESA and Arkisys fronts provides the real-world validation data necessary for underwriting these new products.

Accelerator-driven nuclear systems for fuel production and medical isotopes

Highlight: Unlocking path multi-billion dollar potential revenue stream with medical isotope production. Next Key Milestone: Identify potential pharmaceutical offtakers for isotope production. Next Expected Round: $100M Series B by Q2 2026

Transmutex, founded in 2019 in Geneva, is reinventing nuclear energy for a safer, cleaner future. Transmutex's innovative approach addresses the core concerns associated with nuclear energy, notably waste, safety, and proliferation. Transmutex's technology is a significant advancement in carbon-free energy generation that is deployable around the world. Unlike traditional fission systems, Transmutex's system can use multiple types of fuels, including thorium, by using a particle accelerator to drive a safer, non-self-sustaining reaction. Applications of this technology are extensive including; efficiently breeding new fuel to replace uranium enrichment, enabling a new thorium-based fuel cycle for national security, burning the existing stockpile of long-lived nuclear waste to lower long term costs, and scalably producing medical radio-isotopes for cancer treatments. Transmutex has also developed simulation software with applications beyond nuclear energy.

The past quarter marked a decisive step for Transmutex in maturing its accelerator-driven reactor program. Each front showed both progress and friction typical of early industrial diplomacy. The team in Switzerland achieved technical breakthroughs that demonstrate the core physics of its waste-to-fuel cycle. At the same time, the company opened an entirely new vertical in medical isotopes that could generate near-term revenue and long-term strategic leverage with regulators, utilities, and national labs.

Technical Achievements at PSI

The Paul Scherrer Institute collaboration continues to anchor the company's credibility. During the quarter, the AI-enabled cyclotron control experiment that began at 72 MeV was extended to cover the full 800 MeV beamline. The experiment is scheduled for April 2026 and will include federal health authority oversight. This marks the first attempt to apply machine-learning feedback to a full-scale high-energy accelerator system, establishing a key differentiator in both operational reliability and licensing efficiency.

The fuel-fabrication team achieved a major milestone by successfully producing and sintering the first thorium fuel pellet. The thorium shipment, delayed six months by export bureaucracy and customs reviews for its low-level radioactivity, finally arrived in Switzerland in late August. The resulting pellet demonstrates full structural integrity under reactor-relevant heat and pressure and will serve as the prototype for upcoming irradiation tests. For Indian stakeholders, this proof is critical to show that Transmutex can execute thorium fuel fabrication domestically once regulatory frameworks are aligned.

Another operational highlight was the cleanup of a contaminated hot cell at PSI. The Transmutex team completed the work in one week versus the one-year estimate by PSI management, unlocking access to additional hot cells at minimal cost. This demonstrated capability has attracted interest from URENCO, which lacks hot-cell capacity and could partner with Transmutex for shared research infrastructure. The only technical setback was the cancellation of the planned spallation demonstration in liquid lead due to space and cost constraints, estimated between 30 and 70M CHF. The company is evaluating conducting this experiment in Germany using the planned medical cyclotron site instead.

Strategic Partnerships and New Markets

The partnership with URENCO, the European uranium-enrichment consortium owned by the UK and Dutch governments and utilities including RWE, evolved into multiple parallel workstreams. URENCO commissioned a €25,000 feasibility study to analyze combining uranium-233 with depleted uranium stocks to create hybrid fuel suitable for conventional reactors, potentially reducing the need for new uranium mining. The parties also agreed on a pathway to secure HALEU supply for Transmutex's future START reactor and opened discussions to apply Transmutex's AI systems to documentation, process audit, and centrifuge operation optimization.

A separate collaboration emerged with TÜV NORD, Germany's premier nuclear safety authority. The agency requested a case study demonstrating how Transmutex's AI models could accelerate and standardize safety-case evaluations. Early results matched the conclusions of TÜV's human experts, establishing a strong basis for extended cooperation.

The most unexpected breakthrough this quarter came from the medical-isotope initiative with CHUV Hospital in Lausanne, ranked 15th globally. Transmutex signed an MOU with CHUV to co-develop Terbium-149 production using high-power accelerators. The isotope, proven in mice to destroy up to 40% of cancer types, currently can be produced only at CERN. Transmutex now employs the scientist who led the original Terbium-149 experiments there. CHUV leadership, including the directors of the Nuclear Medicine Center and Medical Service, provided formal letters of support and outlined plans for a dedicated isotope-production facility. The economics mirror the trajectory of Novartis's Lutetium-177, which became a multi-billion-dollar therapy platform. Terbium-149, sharing similar chemistry but higher energy, could supersede it in efficacy and cost efficiency. PSI has recently secured 50M CHF in federal grants for isotope research, opening a shared development pathway toward industrial-scale production by 2028-2029. This medical-isotope vector not only creates a near-term commercial opportunity but also strengthens Transmutex's regulatory legitimacy by demonstrating socially beneficial nuclear technology.

United States: Los Alamos and ARPA-E

Following the NDA execution with Los Alamos, Transmutex transmitted its full technical dossier to Los Alamos, including the SPRIN-D status report and updated modeling for neutron economy, waste transmutation yields, and accelerator reliability. Argonne reviewed the fuel-cycle and recycling modules and formally endorsed the data. We are still waiting (due to security clearances) to move forward with these engagements in person in the US.

Germany: RWE Alignment and Regulatory Strategy

In Germany, the company achieved formal approvals from the RWE (largest utility in Germany) board and the mayor of Gundremmingen to sign an MOU for site access and collaboration, supported by the federal innovation agency SPRIN-D. RWE committed roughly €50M in cost share via infrastructure, grid access, and site use. This framework anchors Transmutex's German operations near one of the most significant decommissioned nuclear sites in Europe. Local politics remain the gating variable. The district manager of Gundremmingen has resisted signing any agreement containing nuclear-waste-related language, citing upcoming elections and public sensitivity. The near-term workaround has been to limit the MOU scope to medical applications, excluding explicit reference to transmutation or waste processing. Similar local pushback has stalled even low-level nuclear-medicine projects in Bavaria for years, some eventually relocating abroad. To counter this structural friction, Transmutex is working with SPRIN-D (the German Federal Innovation Agency that invested in Transmutex) to elevate the project to the federal level. The company submitted a concise two-page memo proposing a research program to prove that accelerator-driven transmutation can shorten waste half-lives and ease repository requirements. This memo will be evaluated as part of Germany's national innovation agenda, which will select ten priority projects for federal support before year-end. If chosen, the project would give Transmutex political cover to operate under federal mandate rather than local discretion. The team expects to finalize the medical MOU with RWE and Bavaria by year-end while continuing parallel lobbying for federal endorsement.

India: Diplomatic Scheduling, Utility Engagement

Progress in India has been delayed by coordination issues between the Indian government and the Swiss embassy. A planned August meeting with Dr. Saraswat of NITI Aayog and the Swiss ambassador was postponed multiple times, now tentatively reset for October. No material setbacks have occurred, but forward movement requires a government-to-government framework between India and Switzerland. Meanwhile, Transmutex plans to engage India's largest utility, a 70-GW predominantly coal-based enterprise that has recently created a nuclear engineering division focused on thorium reactors. This initiative aligns with India's long-standing thorium ambitions and offers an industrial rather than diplomatic entry point. The forthcoming India trip aims to solidify this relationship to maintain momentum independent of bilateral formalities.

Potassium-ion batteries for critical-mineral-free energy storage

Highlight: Steel Atlas taking board seat. Next Key Milestone: Formalize the SBIR Phase 2 award and identify potential acquirers. Next Expected Round: Series A or M&A

Group1 is commercializing potassium-ion batteries (KIBs) which are poised to become a significant player in the energy transition, offering an attractive alternative to lithium-ion batteries due to their cost-effectiveness, resource availability, and environmental benefits. Unlike traditional lithium-ion batteries, which rely on critical minerals sourced from regions of geopolitical instability, KIBs utilize potassium, a more abundant and cheaper alternative. This reduces supply chain vulnerabilities. Group1's KIBs are critical-mineral-free and "drop-in" compatible with existing LIB infrastructure, ensuring a capital efficient path to scale. KIBs are on path to having energy density on par with LFP-based LIBs, comparable cycle life, faster charging, and superior low-temperature performance.

Bridge Round

In July, the company faced a critical liquidity event with only three weeks of runway remaining. A bridge financing process was launched under severe time pressure. By late July, Group1 successfully closed $750K in senior convertible notes, structured with a 2x-10x sliding return depending on exit valuation (2x at $10M or less, 10x at $100M or more). Steel Atlas participated with a $50K+ commitment, deployed in tranches tied to operational milestones. Following the raise, the board was restructured to reflect a tighter governance model. Previous investor Valhalla assumed three board seats with one being assigned to Steel Atlas (Cameron Porter). This bridge stabilized the company through the quarter and positioned it to secure non-dilutive federal funding and strategic partnerships while preparing for a structured Series A process or M&A.

Macro Situation

The global battery industry entered a sharp realignment this quarter. Western automakers including Porsche's Cellforce and Mercedes-Benz formally halted next-generation battery programs, while most silicon anode commercialization timelines slipped to 2028 or later. Meanwhile, Chinese EV manufacturers advanced at record speed, integrating superior chemistry, form factor innovation, and vehicle intelligence: eroding the West's technological lead. In a significant policy shift, China formally restricted exports of LFP (lithium iron phosphate) cathode materials to the US, effectively cutting off the world's most mature and cost-efficient lithium battery chemistry from American supply chains. This move further validated Group1's pursuit of potassium-ion as a domestic, critical-mineral-free alternative. Against this backdrop, Group1 stands out as the leading American company pursuing potassium-ion chemistry at scale, offering a fully domestic, lithium-free alternative with clear strategic value for national resilience and defense applications. The company's technology now sits at the intersection of two major policy priorities: energy independence and critical-mineral security.

Government and Strategic Relationships

Group1 was formally invited to join the Department of Energy's Energy Storage Research Alliance (ESRA), the flagship "Beyond Lithium" roadmap initiative led by Dr. Shirley Meng. This inclusion places Group1 within a select cohort shaping the next decade of US energy storage research and policy direction. The company is also near certainty to receive a $1.25M SBIR Phase 2 award, supporting 18 months of continued development alongside the University of Texas at Austin and Stony Brook University as subcontractors. On the industrial side, Group1 secured letters of support from Schneider Electric, Orbia, and Cabot, three global materials and infrastructure players. The partnership with Schneider Electric is deepening, centered on high-density battery backup systems for data centers and industrial UPS deployments.

Go Forward

Given Group1's cash position, we are taking an active role in the company on a go forward basis. Through this oversight we will be prioritizing commercial engagements as well as running a managed M&A process to provide an alternative to Series A financing in the event they do not achieve the necessary commercial milestones. Given their technical achievements, Group1 is a strategic acquisition target for players throughout the value chain from American potassium producers to UPS system developers for datacenters.

AI structural engineering for faster, cheaper, greener construction

Highlight: Hedral entry into MENA market (discussions with Nesma, Aramco, Orascom). Next Key Milestone: Secure and execute the first live MENA pilot project to establish proof-of-concept for regional scaling. Next Expected Round: $15M Series A by Q1 2026

Hedral is an AI structural engineering firm based in New York that enables real estate developers to build faster, cheaper, and with lower environmental impact. Today, Hedral is already the most efficient structural engineering firm in the world, delivering stamped drawings and 3D building models to developers 10x faster than legacy firms. Hedral's core technology automates the creation of the drawings and models that takes traditional firms weeks to months to produce manually. This is positioning Hedral to roll-up the fragmented, multi-hundred-billion-dollar market for construction design and engineering.

Geographic and Strategic Expansion

Hedral took a decisive step toward internationalization this quarter, with the leadership team conducting an extensive MENA market visit in September. The trip centered on Egypt and Saudi Arabia, aligning with the company's strategy to embed itself within regions undertaking massive infrastructure modernization. Hedral met with the largest construction company in Egypt, Orascom Construction Industries (OCI), to explore a partnership. In Saudi Arabia, Hedral opened early dialogues with Aramco, focusing on upcoming infrastructure and federal projects tied to Vision 2030.

Customer and Partnership Development

A key initiative this quarter has been reactivating engagement with Nesma Partners, one of Saudi Arabia's leading construction and development firms. Under the leadership of new hire Urszula Solarz, Hedral reinitiated discussions for a pilot project that will serve as a foundational case study for future adoption in the region. The project is being scoped as a proof-of-concept deployment to demonstrate Hedral's full-stack design-to-construction optimization workflow in a live environment. Success here would establish Hedral as a technical partner for large-scale, mixed-use and industrial development projects across the Kingdom.

Across the US, Hedral continues to grow its base of architecture, engineering, and construction customers as an engineer of record. We hope it deepens its reputation for high-precision computational design and AI-assisted coordination in large, multi-stakeholder projects even while in stealth. Hedral continues to operate as a lean interdisciplinary team bridging the gap between classical engineering practice and advanced computation. The team includes licensed engineers and computational specialists from world-class firms such as Foster + Partners, Zaha Hadid Architects, Grimshaw, HOK, AECOM, Thornton Tomasetti, Autodesk, and Amazon. This hybrid composition remains a central differentiator, allowing Hedral to merge design fidelity with automation-grade scalability.

Current Project Portfolio

Hedral's active portfolio now spans multifamily residential developments, industrial facilities, and mixed-use projects across California, Texas, and New York. Notably, the company continues to expand its footprint in federally funded infrastructure, now exceeding 2M square feet of projects for the US Navy and Air Force. These are mission-critical environments that demand extremely tight coordination and digital precision (areas where Hedral's technology excels). The company also continues to deepen its role in advanced energy and nuclear projects. It has signed design contracts with Aalo Atomics and executed an MOU for EPC collaboration with Steel Atlas portfolio company Transmutex, positioning Hedral within the emerging ecosystem of modular and advanced reactor construction.

Following a period of quiet execution, Hedral remains on track for a public out-of-stealth announcement in Q1 2026 timed with a splashy Series A. The team is developing case studies, visual collateral, and marketing materials in preparation for external visibility, particularly aligned with the MENA expansion efforts and upcoming federal project milestones. Hedral's long-term positioning continues to center on becoming the digital backbone of next-generation engineering delivery: an intelligent geometry and coordination layer that replaces traditional, manual project management with algorithmic precision. With a growing portfolio of high-stakes infrastructure projects, strategic partnerships in both the US and MENA, and EOR-level authority, the company is approaching a phase of validated scale and global recognition.