February 14, 2025

Dear Investor,

February 14th, 2025

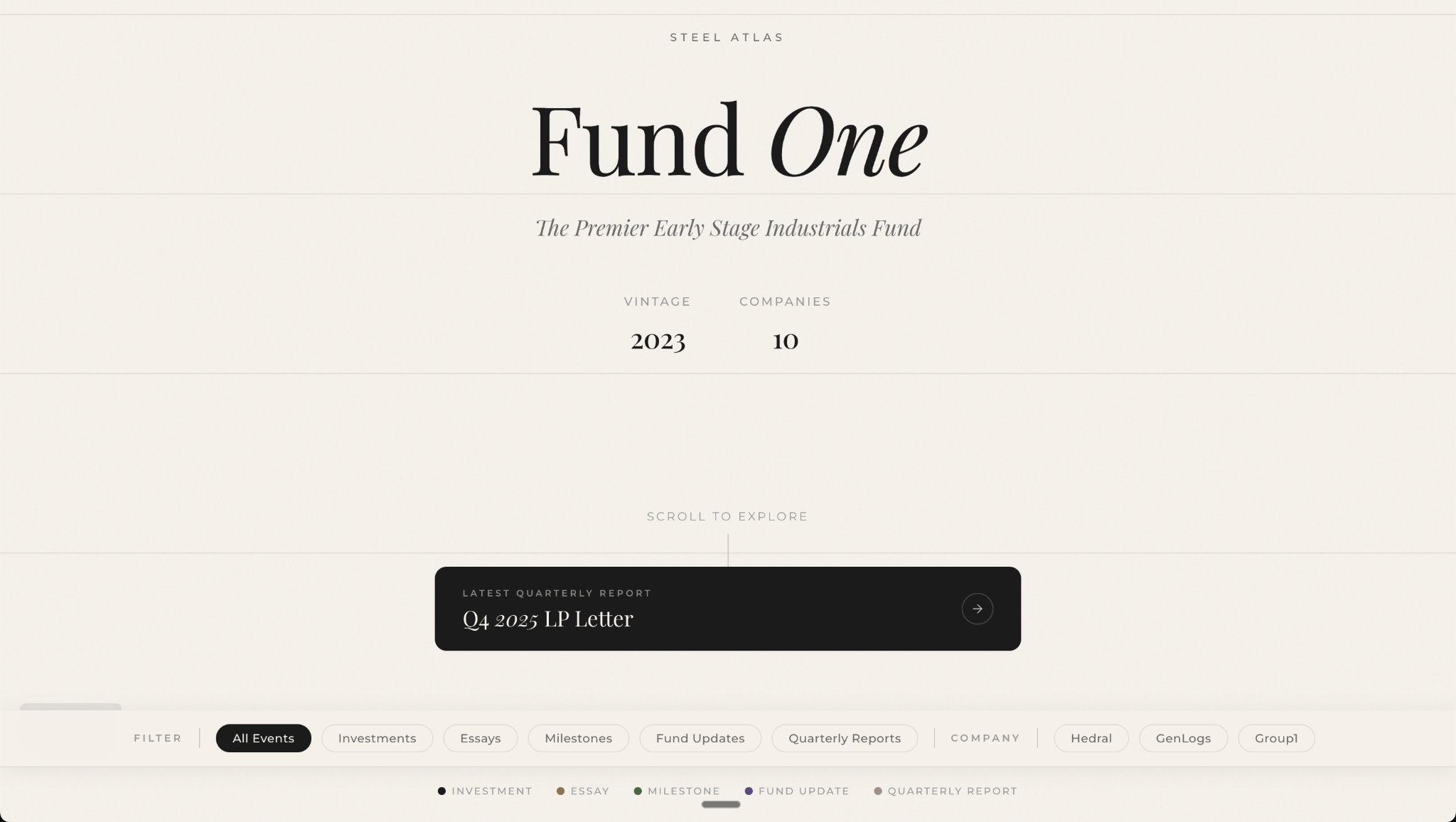

RE: Steel Atlas Fund I LLC, (the "Fund") -- 4th Quarter 2025 Report

In the secure portal, please find the unaudited financial statements, your capital history, unrealized and realized activity report, and capital statements for the fourth quarter of 2025.

For planning purposes, we expect our next capital calls to be sent quarterly for trailing fees of the fund. Our last capital call completed our 10 company portfolio.

We made our final 2 investments into Autonymy (Stealth) and Panthyon (Stealth) in Q4 2025. More below.

With that, we have a special surprise for you all. We have built our own custom timeline and reporting platform. We believe it is a beautiful artifact of the Steel Atlas Fund I journey (that still has its biggest moments ahead). Please enjoy it here (password = steelatlasfundone).

Please email us at steelatlas@hanoverpark.com for any fund-related questions.

Onwards and upwards,

Cameron & Talal

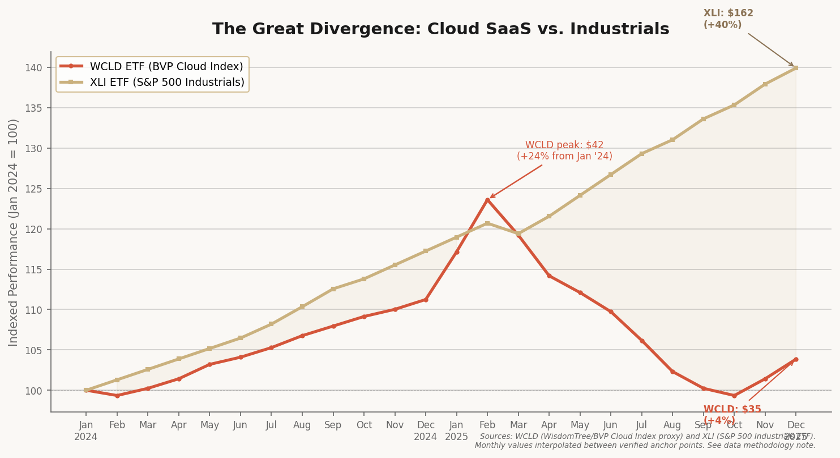

Something unusual happened in 2025. For the first time in over a decade, the technology sector and the industrial economy began moving in opposite directions.

The Bessemer Cloud Index — the benchmark for SaaS companies — fell 28% from its February peak. Salesforce dropped below its 2021 highs. Workday, Zoom, and a dozen other enterprise software companies traded at valuations not seen since before the pandemic. The financial press coined a term for it: SaaSmageddon.

The cause was not a cyclical downturn. It was structural. Foundation models (GPT-4, Claude, Gemini) had begun to do what SaaS companies charge $50,000 per seat to approximate: synthesize data, generate reports, automate workflows, and write code. The entire value proposition of the enterprise software layer (organizing and displaying information for human decision-makers) was being compressed by systems that could reason over that information directly. The marginal cost of software-based intelligence was collapsing toward zero.

However, something very different was happening in the physical economy.

While SaaS valuations contracted, industrial activity accelerated. The CHIPS Act deployed its first tranche of funding. The Department of Energy issued billions in loan guarantees for nuclear projects. Executive orders pushed to bring reactors online by July 2026. Tariffs and trade tensions accelerated the reshoring of manufacturing capacity. And an enormous wave of capital began flowing into the infrastructure needed to power AI itself — data centers, transmission lines, and the energy generation systems behind them.

The divergence was not a coincidence. It was a recomposition. The same force — near-zero-cost intelligence — that was compressing the value of software was simultaneously expanding the value of physical systems. AI both threatened SaaS and supercharged the demand for energy, manufacturing, logistics, and the physical infrastructure that keeps the world running.

It is not a coincidence that Steel Atlas made its first investment in May 2023, roughly six months after the release of ChatGPT. We saw the implications early: that the same wave of intelligence that was about to reshape software would reshape industry. Two and a half years later, we call this thesis the Steel Atlas Moment.

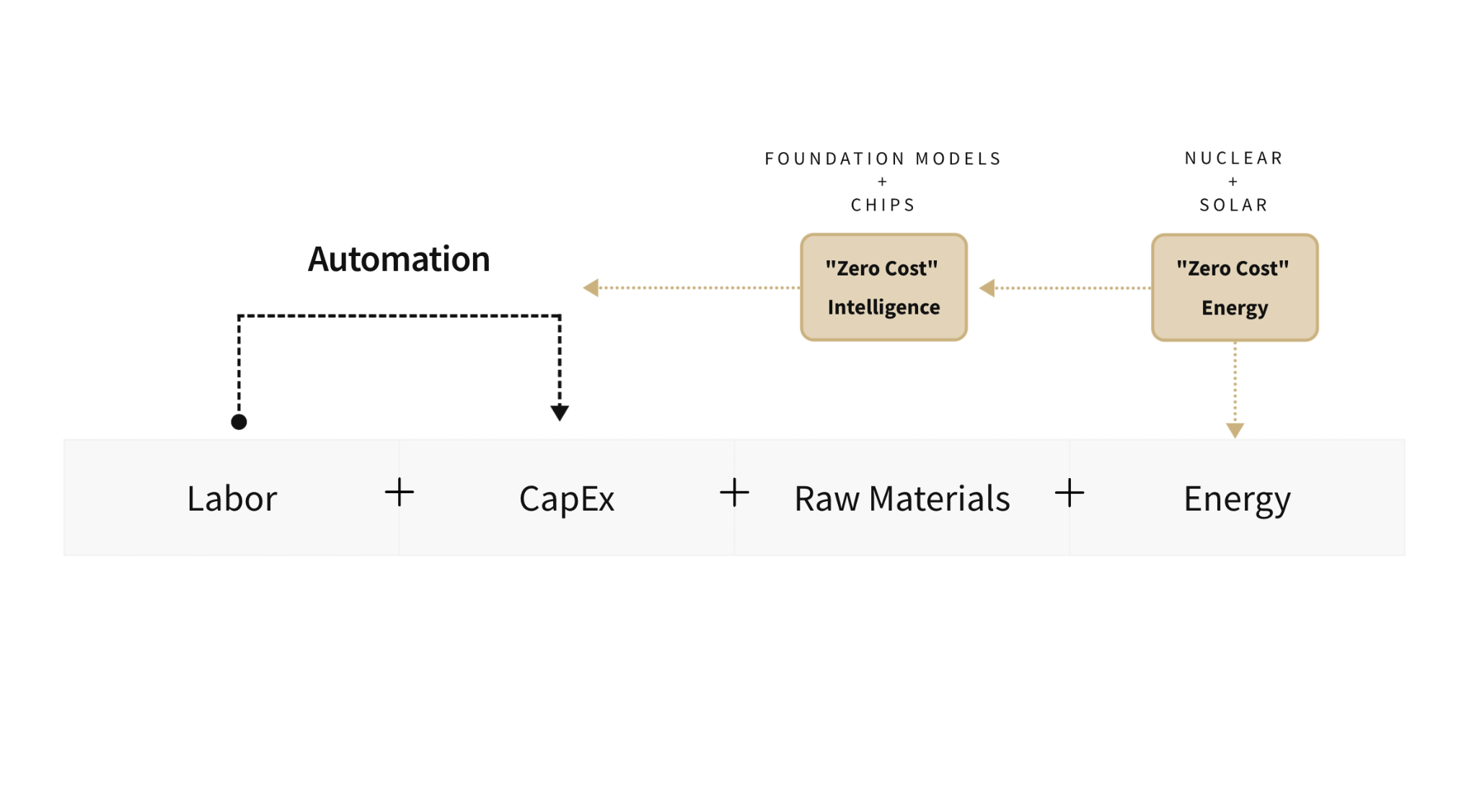

In our Q1 2025 letter, we introduced the Four Cost Model — a framework for understanding how every industrial process is composed of four input costs: Labor, Capital Equipment, Raw Materials, and Energy. We argued that two of these costs were undergoing historic compression: the cost of intelligence (which acts as a substitute for labor and a complement to capital equipment) and the cost of energy (driven by nuclear and solar at scale).

The thesis was straightforward. When you collapse two of the four input costs of any industrial process, you do not just make existing operations cheaper. You make previously impossible operations viable. You reopen factories that could not compete with Asian labor costs (Framework Automation). You finance equipment that banks deemed too complex to underwrite (Substrate Industries). You run refineries with half the engineering staff — not by cutting corners, but by compressing the time between detecting a problem and solving it from weeks to minutes (Panthyon). You build communication networks for environments so remote that fiber and fixed wireless were never options (Autonymy).

This is not theory. It is the portfolio we built.

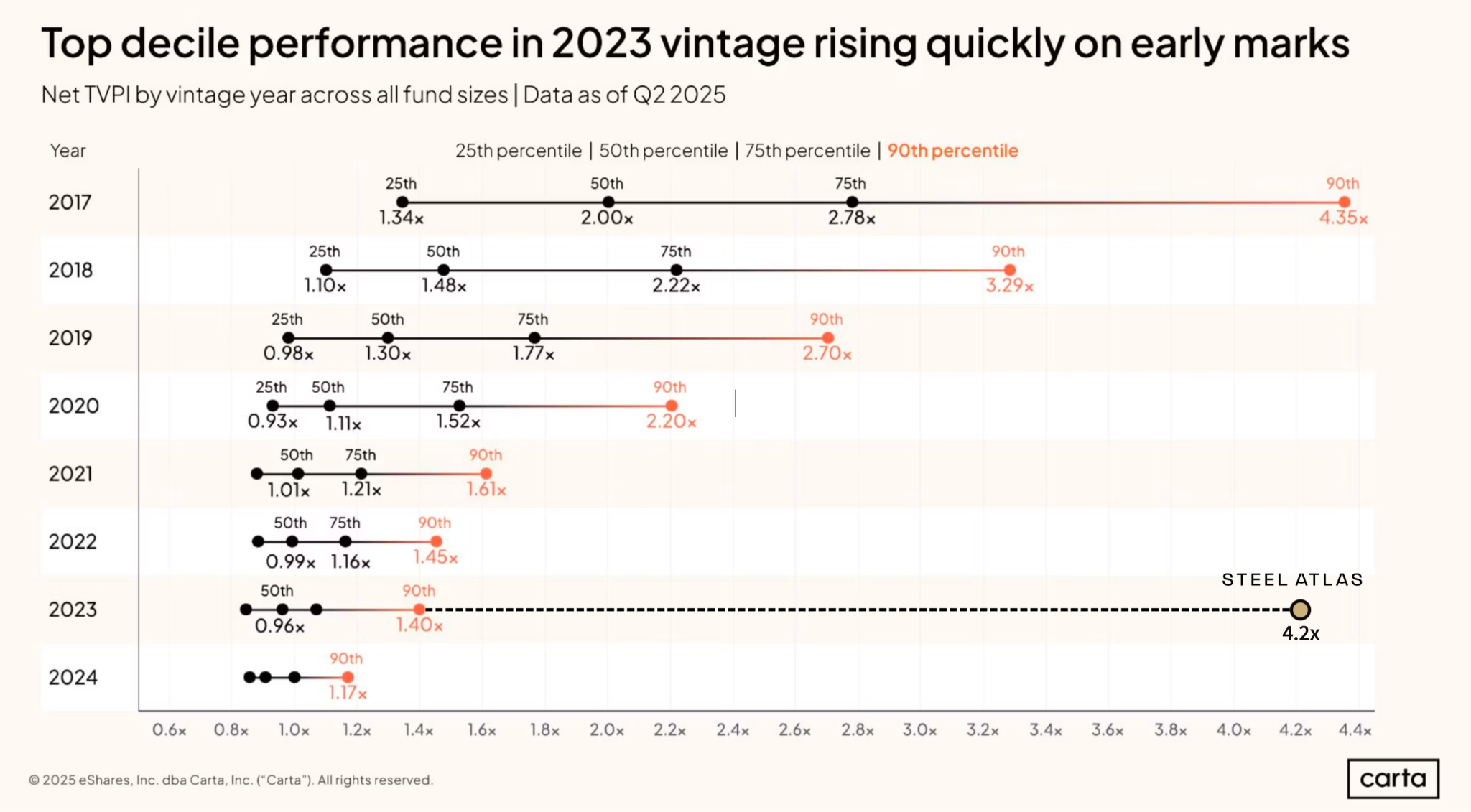

Fund I closed its final investment in December 2025, completing a portfolio of 10 companies. As of the AGM, the fund sits at 190% IRR and 4.2x TVPI — top decile performance in the 2023 vintage on Carta's benchmarks, across all fund sizes. More importantly, those returns are not driven by narrative. They are driven by revenue, customers, and technical milestones that are compounding faster than we projected.

But the performance is not the point of this letter. The point is what the portfolio reveals about where the industrial economy is heading, and what it means for the companies that will define it.

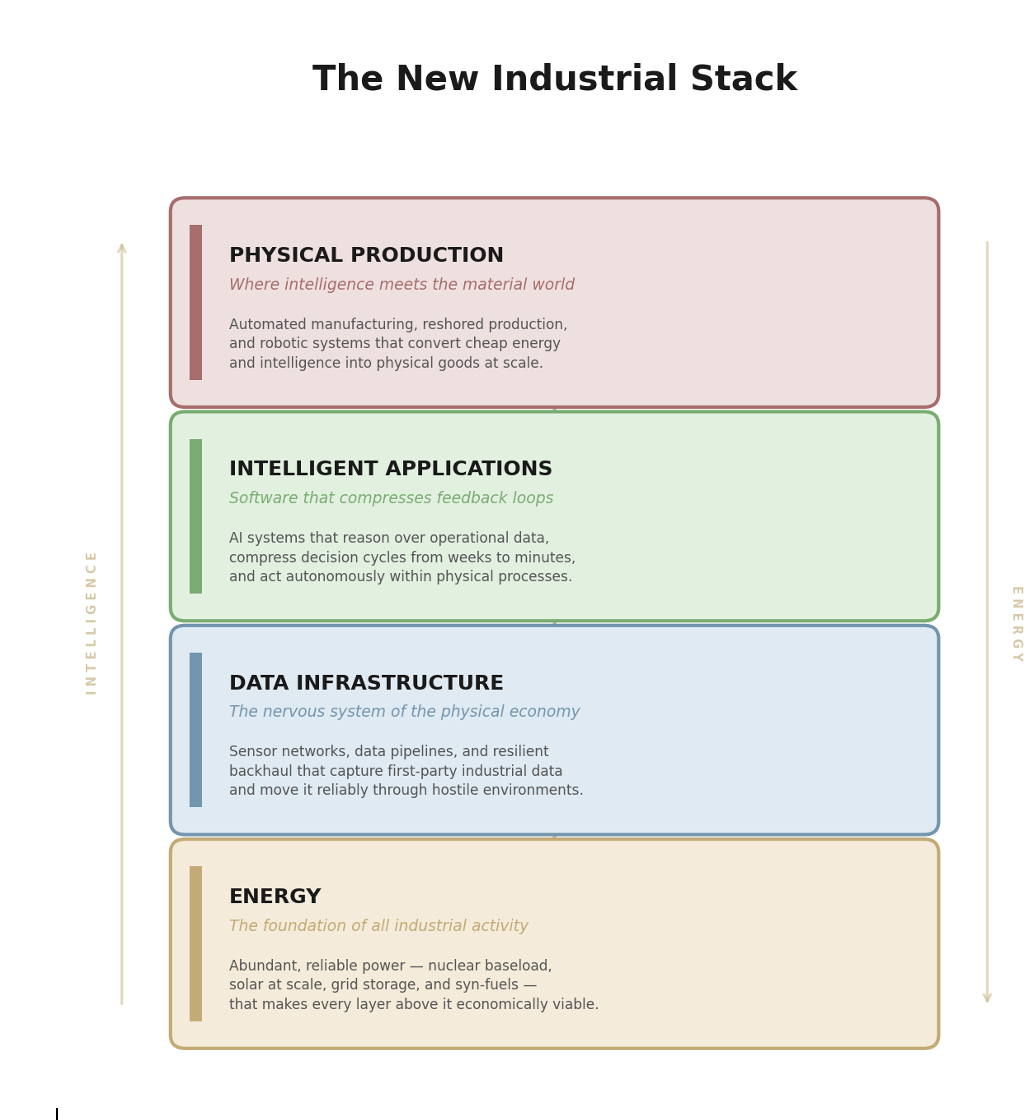

There is an old framework in technology investing that divides the world into infrastructure and applications. Chips, servers, and cloud platforms form the infrastructure layer. SaaS tools, consumer apps, and marketplaces sit on top. For decades, the infrastructure layer generated modest returns while the application layer captured most of the value.

The industrial economy is now developing its own version of this stack. But the layers are different. The foundation is not silicon and software. It is energy and data — the two inputs that every physical system requires to function and improve.

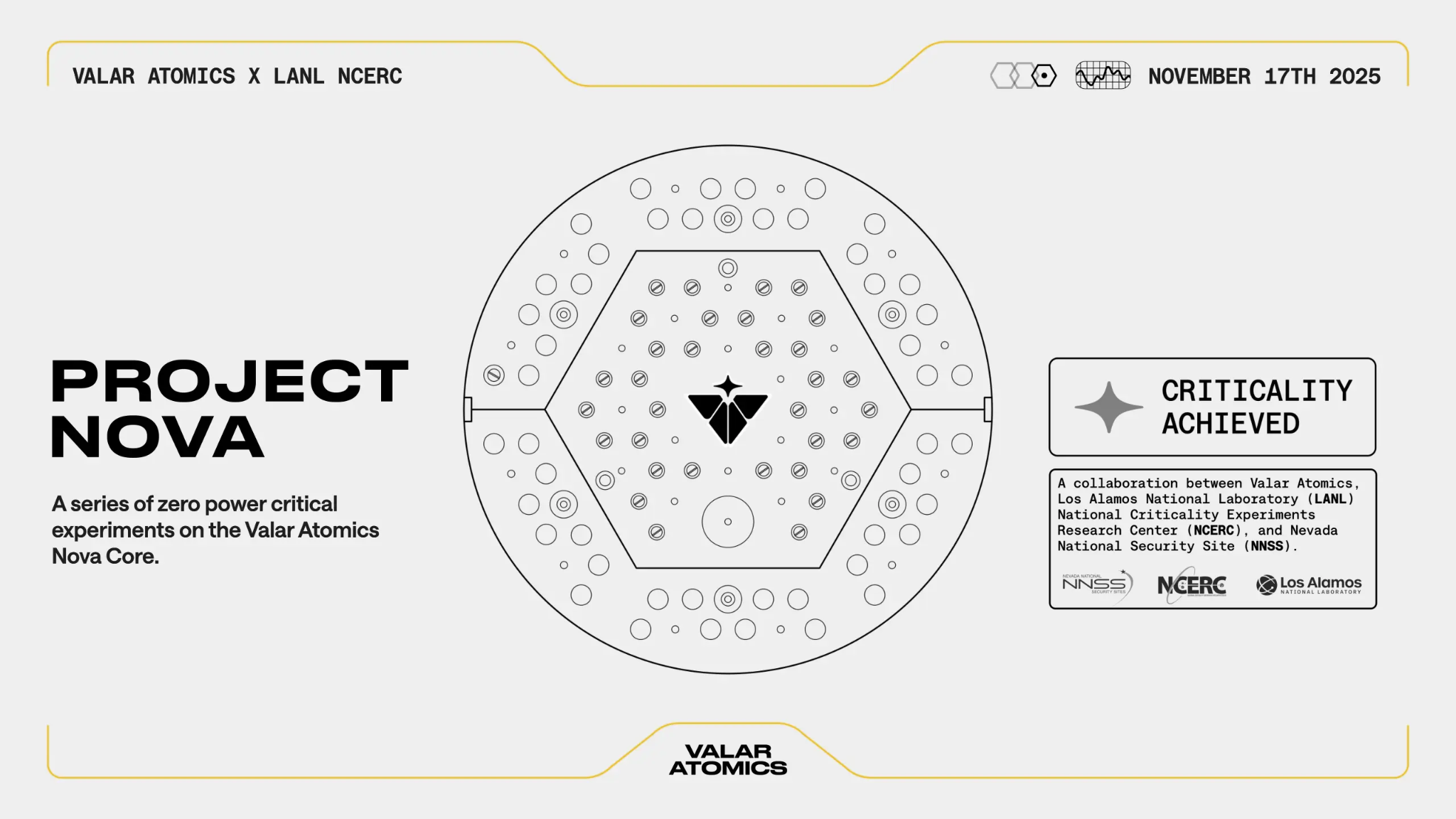

Energy forms the base layer. You cannot run a factory, power a data center, train an AI model, or produce synthetic fuels without abundant, reliable energy. Three of our portfolio companies operate at this layer. Transmutex is building commercially viable high-power cyclotrons that can breed nuclear fuel, transmute radioactive waste, and produce medical radioisotopes — three applications from a single technology platform. Their AI-operated cyclotron at the Paul Scherrer Institute surpassed expert human performance within four days. Valar Atomics became the first startup in history to achieve nuclear criticality, reaching zero-power critical on their Nova Core at Los Alamos in November 2025, and closed a $130M Series A. And Group1 is developing potassium-ion batteries, a critical mineral-free alternative for grid storage, that could reshape the raw materials and energy layers of the cost equation entirely.

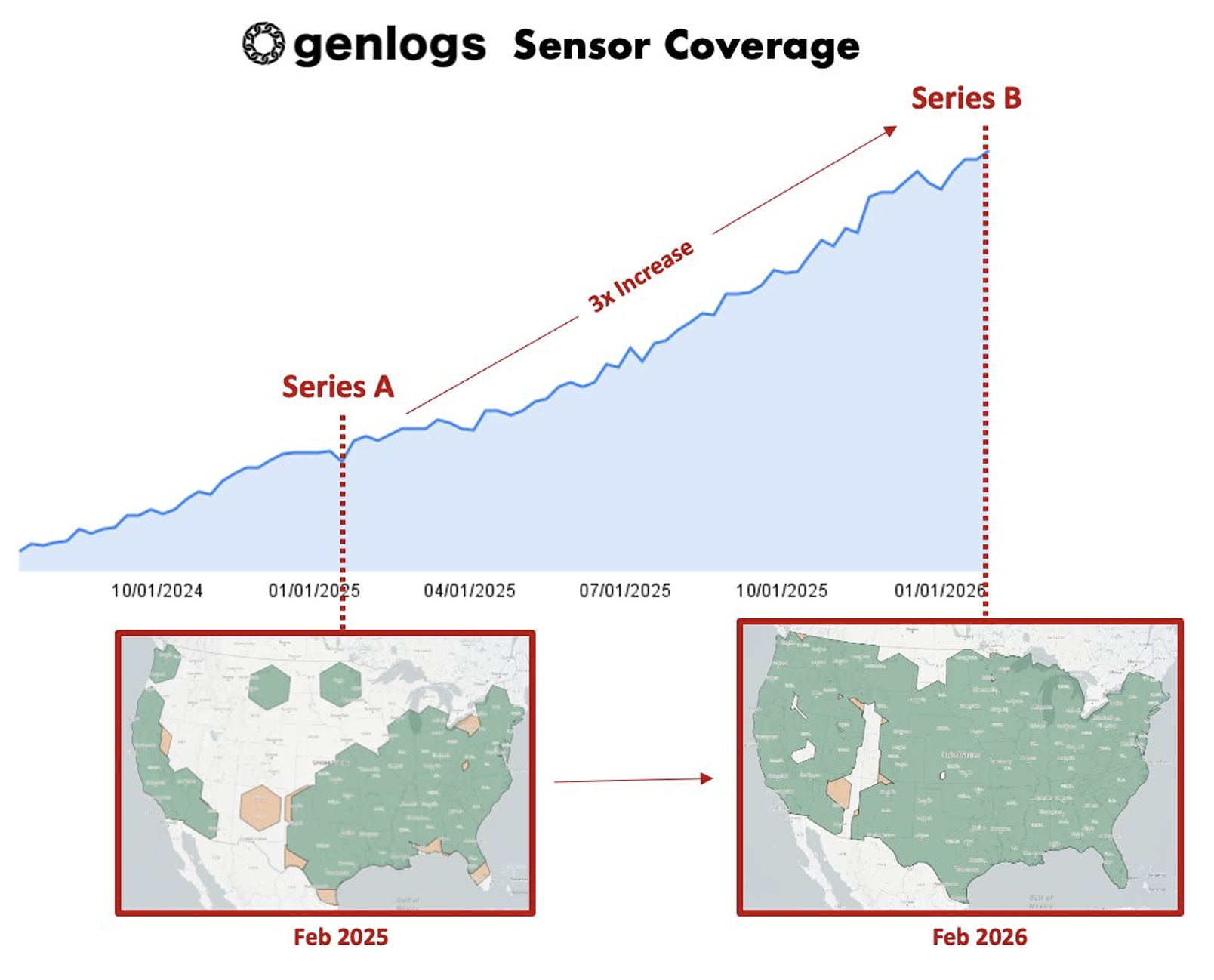

Data infrastructure forms the nervous system. In our essay "Data Gushers", we described how the most valuable industrial data companies share three traits: they tap latent infrastructure that already exists, deploy an integrated sensor package to capture first-party data, and build a sense once, sell many model that compounds value with every new data stream. The companies that capture industrial data, pipe it reliably through hostile environments, and structure it for decision-making will control the information advantage of the next industrial era. GenLogs tracks every long-haul truck in the United States using a proprietary sensor network (now at 280+ sensors) fusing satellite imagery, mobile ad-IDs, and traffic cameras into the most comprehensive freight intelligence platform ever built. They achieved zero churn and 188% net revenue retention on their first annual renewals.

Their Series B validates the thesis. ODIN Space deploys nano-sensors on satellites to detect sub-centimeter orbital debris, enabling the first data-driven insurance products for the space economy. This is coverage that is 10–100x cheaper than current alternatives. And Autonymy, our final Fund I investment, builds the data pipeline itself. Resilient, device-mountable mesh networks that bond cellular, satellite, and RF into a single pipe for environments where commercial networks do not reach.

The GenLogs-to-Autonymy connection deserves emphasis, because it illustrates how this portfolio was built. In our Q3 2025 essay, "Bonsai and The Art of Growing the Firm", we described how conviction is emergent. The stepping stones to great outcomes often look nothing like the outcome itself. GenLogs taught us firsthand how difficult it is to move terabytes of data from remote sensors on rural highways across unreliable networks. That operational experience, seen through their eyes, surfaced the data backhaul problem as one of the great horizontal opportunities in industrial technology. Autonymy is our answer.

Intelligent applications form the decision layer. Software that does not just display data but reasons over it, compresses feedback loops, and in some cases acts autonomously. The core value of this layer is cycle time compression: turning weeks of analysis into minutes of action, and turning manual review into continuous, autonomous operation. Hedral's AI structural engineering platform has grown to over $2M in revenue ($4M bookings), serving the Navy, Air Force, and data center operators. They have compressed structural analysis timelines from weeks to hours. Panthyon is building an agentic operating system for the 30,000 continuous-process plants that keep the global economy running. They have compressed the Management of Change workflow from weeks to minutes. Substrate Industries uses AI to underwrite industrial equipment at the machine level, offering instant credit decisions that replace the weeks-long, borrower-only models used by banks. Each model upgrade compresses the decision cycle further (lower loss rates, faster throughput) while inference costs stay flat. They sell results, not tokens.

Physical production is where it all converges. Framework Automation is reshoring American knitwear manufacturing using 3D whole-garment knitting machines orchestrated by a software platform that eliminates the labor-intensive linking and sewing steps. Their first factory — a 13,000 sq ft facility in Culver City — achieves cost parity with Asian mills at 70%+ machine utilization, before accounting for eliminated tariffs, freight, and inventory carrying costs.

This is the New Industrial Stack. This is how the industrial economy is being recomposed around two forces that are compressing simultaneously: intelligence and energy. The companies that sit at the intersection — capturing data from physical systems, moving it reliably, applying intelligence to compress feedback loops, and using cheap energy to power the result — will compound in ways that pure software companies cannot. For a deeper look at each investment, our published memos are available on our website: Hedral, Group1, GenLogs, Transmutex, Valar Atomics, ODIN Space, Framework Automation, Substrate Industries, Panthyon, and Autonymy.

The distinction matters because it explains the divergence we see in public markets, and the one we expect to accelerate.

SaaS companies are fragile to AI because their value was always derived from organizing information for humans. When AI can do that directly, the application layer compresses. But industrial companies that use AI to improve physical processes are anti-fragile to AI — each advance in foundation models makes their operations better, their data more valuable, and their unit economics stronger.

When a new model is released, Substrate's underwriting engine gets faster and more accurate. Panthyon's process engineering agents compress feedback loops further. Transmutex's cyclotron tuning improves. GenLogs extracts more intelligence from the same sensor data. The AI upgrade cycle is a headwind for SaaS and a tailwind for industrial-tech.

We practice this internally as well. At our December AGM, we shared two commitments about how we are scaling the firm. First, we hired Isabella Zimmerman as Chief of Staff. Isabella joins us from Citadel and Goldman Sachs, with prior experience in the Office of the CEO at Palantir, bringing deep expertise across finance and industrial technology operations. Her mandate is to strengthen fund operations, investor relations, and our ability to continue executing SPV co-investments into our top-performing companies — as we have done successfully with many of you in the past. Second, rather than hiring a CFO, we chose to use AI and automation tools combined with our AI-native fund administrator, Hanover Park, to manage financial operations. We believe it would be irresponsible to advocate for AI-enabled industrial operations while running our own firm on spreadsheets and manual processes. The best way to understand a technology's limitations is to depend on it yourself.

To bring it all home, we have built our own custom reporting platform just to demonstrate what is possible. You can explore that here (password = steelatlasfundone). The times are changing and we believe they are changing in our favor.

Fund I is complete. Every investment made with the conviction that the industrial economy is entering a structural transformation driven by near-zero-cost intelligence and abundant energy — a transformation that rewards companies who capture and move data through physical systems, apply intelligence to compress decision cycles, and build on energy infrastructure that scales.

The returns to date — 188% IRR, 4.4x TVPI — reflect the early innings of this transformation. GenLogs's Series B, Valar's $130M raise, and Transmutex's growing international partnerships are validation that the market is beginning to price what we saw early. But as we wrote in "Bonsai and The Art of Growing the Firm": the key is to continue building conviction after the initial investment. The work of compounding knowledge, relationships, and operational understanding within these companies is only beginning.

Fund II is now active, targeting the same concentrated, high-conviction approach that defined Fund I. The advantages of concentration and speed that produced these results do not scale linearly with capital. We would rather be a bonsai than a redwood. Small, intentional, one of a kind.

In our very first quarterly letter, in Q1 2024, we closed with a simple idea: that the companies building at the intersection of AI and the physical world would define the next generation of industrial champions. Seven quarterly letters later, we have a complete portfolio that embodies that thesis. The world has caught up to the conviction. Nuclear energy is bipartisan consensus. AI-enabled manufacturing is national policy. Freight intelligence is enterprise infrastructure. The tide we predicted is here.

Now we ride it.

Three commitments as we look ahead. First, we will keep you closely informed as the portfolio progresses: the quarterly letters, the shared memos, and the direct conversations that have defined this partnership from the beginning. Second, as discussed at the AGM, we are actively pursuing DPI and will execute on opportunities to return capital as they emerge. Third, we will continue improving the firm — our operations, our tools, our network, and our ability to compound advantage for our founders and our partners. The best is ahead.

Onwards and upwards,

Cameron & Talal

Data infrastructure for the world's most critical operations

Highlight: Closed oversubscribed seed round led by Accel.

Next Key Milestone: Deliver prototype hardware to pilot contracts.

Next Expected Round: Q4 2026

Autonymy is building the data infrastructure backbone that America's most critical operations depend on. They design and manufacture intelligent, multi-WAN edge devices that ensure resilient data orchestration in the world's most demanding environments: from defense operations to industrial facilities, energy infrastructure, and mining operations. Their technology replaces legacy radio systems with next-generation solutions built for reliability, ruggedization, and intelligent network orchestration at the edge. As robotics and autonomous systems reshape how critical work gets done, Autonymy is providing the foundational infrastructure that makes it possible.

Autonymy is building a small, device-mountable connectivity hub plus a software stack that creates resilient, mobile ad-hoc mesh networks (MANETs) across heterogeneous links (multiple 5G modems today, satellite and other radios as needed). The product gives operators fine-grained data-priority control and real-time observability at the edge, in packages simple enough for a 19-year-old field tech to deploy.

The strategy is to harden the system in critical industrial and defense use, then scale into construction, energy, and robotics where networks are brittle, environments change constantly, and integration budgets are limited. Hardware is deliberately commoditized and priced near cost; recurring software and support drive margin.

The founding team combines a decade of shared work at Anduril with deep, complementary technical roots. The CEO built and led the Lattice Autonomy Platform, the mission autonomy framework underlying Anduril's deployed robotic systems, and holds a PhD from MIT in computational engineering. The COO brings 15+ years of hardware production experience across Ford, Tesla, NIO, and Anduril, with a specific focus on taking early-stage prototypes through design verification, supplier qualification, and volume manufacturing.

The CBO led simulation and perception engineering at both Anduril and NIO, and now runs commercial strategy with a deliberate wedge-and-expand model targeting defense and industrial buyers. Together, they cover the full stack from network software and autonomy architecture to manufacturable hardware and go-to-market execution.

Autonymy's hardware is a compact "connectivity hub" that mounts on a host device (drone, robot, excavator, fixed node) and bonds multiple links while participating in a self-forming, self-healing mesh. It prioritizes critical flows (for example, terminal guidance or telemetry) over "nice-to-have" feeds (for example, secondary video), using operator-set policies exposed through a simple GUI or provisioning file. The same box works whether the node moves or stays put. This lets Autonymy serve highly dynamic fleets first, then spill into stationary private-network use cases where setup is onerous today.

Autonymy has three key forms of differentiation in their design. First, simplicity — the system must be deployable and configurable by non-experts in the field, which competitors routinely fail at. Second, data-prioritization done right — Autonymy treats prioritization as an operator-level control at the device, solving real operational bottlenecks like the common complaint that crews cannot stream from two drones at once because existing radios cannot arbitrate bandwidth sensibly. Third, observability — optional ingestion into an Autonymy timeseries and map layer enables queries such as, "show all field devices below 20% battery," with ingestion instrumented first on Autonymy's own infrastructure ("dogfood first").

The company will prove the product in industries through their customer network where the pain is clear (e.g. portfolio company GenLogs). Autonymy intends to avoid becoming a systems-integration consultancy. Their goal is to sell a product, keep field headcount lean, and work with integrators and OEMs for installs and pull-through. Customer success will not rely on an army of FDEs like Palantir or Cognition.

1. Defense robotics and comms kits that need resilient mesh across moving assets.

2. Construction and quarries seeking ad-hoc site Wi-Fi and device connectivity without private-5G heavy-lift.

3. Energy midstream operators with tens of thousands of edge sensors "duct-taped" together today. For example, a large Oklahoma operator cited ~50,000 field devices and interest in trials.

4. Industrial robotics and heavy equipment, selling both to operators (multi-OEM fleets) and OEMs seeking differentiation. One major OEM is already self-sufficient and thus its competitors are "desperate" for open fleet solutions.

Agentic operating system for industrial plant operations

Highlight: Closed Pre-Seed with Primary Venture Partners leading alongside Steel Atlas.

Next Key Milestone: Expand from single plant pilots to multi-facility contracts.

Next Expected Round: Seed in Q2 2026

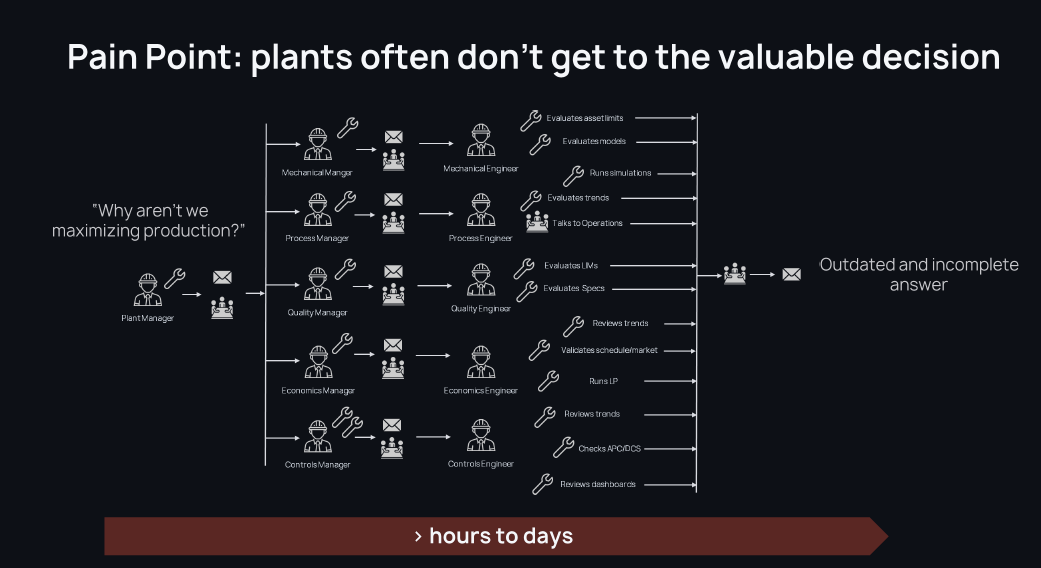

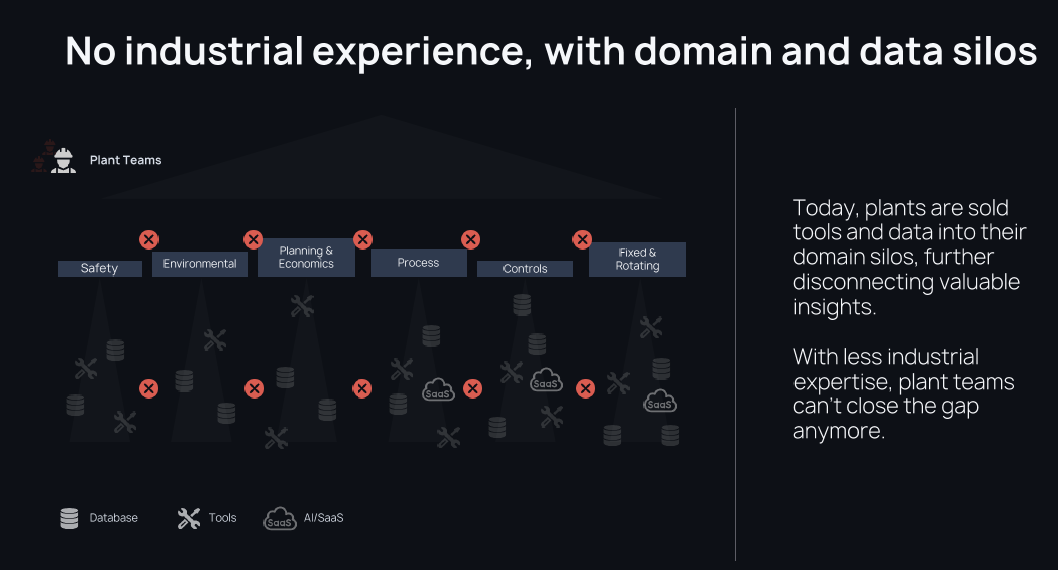

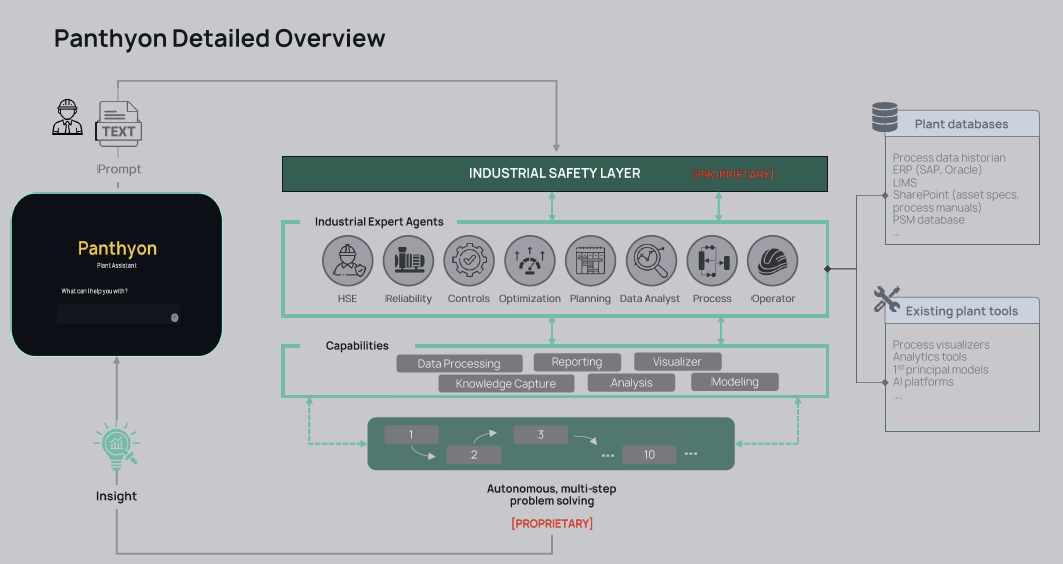

Panthyon is building an agentic operating system that helps plant engineers diagnose and resolve process issues in minutes instead of weeks. Panthyon's solution uses a suite of AI agents, each representing a plant engineer (process, mechanical, safety, operations, etc.), that can solve plant challenges and offer real-time support. The solution also incorporates industrial domain expertise to ensure the insights are validated for safe operational use. Plant experts simply type in their requests, and the industrial agents autonomously work to generate actionable insights, improving the plant's bottom line. Industrial plants have lost their operational experience. Previous experience has retired, existing plant experts are spread too thin, and new talent is scarce. Now, critical insights are missed resulting in $10s of millions lost as a result of production, safety, and reliability events annually.

At the heart of the global industrial economy are roughly 30,000 continuous-process plants (refineries, chemical complexes, cement mills, and steel works) that keep modern life running. These facilities are among the most complex systems humans operate: thousands of sensors and control loops working in concert, yet still reliant on a small cadre of engineers whose judgment holds the plant together. Each day, dozens of micro-failures ripple through pumps, valves, heat exchangers, and reactors. Any single issue may seem trivial, but collectively they erode billions in productivity and billions more in lost material and energy efficiency. Studies estimate over $150B in annual losses from unplanned downtime and slow response cycles alone.

When something changes (a compressor fouls, a feedstock shift, or a new emissions permit comes into effect) engineers must execute a Management of Change (MOC) process. This is the nerve center of plant operations: gathering fragments of information from time-series historians, SAP maintenance logs, Excel sheets, OEM manuals, and handwritten notes, then coordinating across process, mechanical, and environmental teams to decide what to do next. It is painstaking, high-stakes work that depends on tacit knowledge accumulated over decades. Knowledge that is now retiring faster than it can be replaced.

This bottleneck sits precisely where the industrial software stack is weakest. The last forty years digitized data collection but not decision-making. Systems like AspenTech and OSIsoft organized information, but they never helped engineers think. We are entering a new era in which industrial software is no longer about where data lives, but how judgment is applied. The old hierarchy of ERP → historian → control system is being restructured into a new cognitive stack: one that fuses data, simulation, reasoning, and execution into continuous loops.

Panthyon sits squarely in this new middle layer: the decision-intelligence layer of industry. The company is not building a dashboard or analytics tool, but rather designing an agentic reasoning system that sits between data and control, compressing the time between detection and action. Where legacy tools report what happened, Panthyon explains why it happened and what to do next.

The company's first product, internally called PlantGPT, acts as a mini process-engineering assistant. It ingests live telemetry, historical data, manuals, and prior incident records to answer complex process questions with transparent reasoning. Engineers can ask, "Why is throughput down five percent this week?" and receive not a probabilistic guess, but a traceable, deterministic explanation grounded in the plant's own context. In practice, this reduces hours of cross-disciplinary coordination to minutes.

What makes Panthyon distinctive is not only the interface but the feedback architecture behind it. Each solved incident becomes a structured problem-prompt and a reusable logic template that captures both the data pattern and the human rationale behind a decision. These templates feed back into the model, creating a compounding flywheel where institutional knowledge is captured, shared, and refined over time. The system learns from the best engineers at every facility, then distributes that learning to others, democratizing expertise.

Panthyon is currently live at pilot customers with full read-write access to the plant's systems. The company is proving the model at a single large chemical facility first. The pilot confirms that cycle times for MOC execution have compressed from weeks to minutes, and engineers are using the system daily to troubleshoot process questions. Word-of-mouth among plant operators has been strong. The company has now secured letters of interest from three additional facilities, each representing distinct operational contexts (polymers, specialty chemicals, energy). The next 90 days will focus on expanding from proof-of-concept at the pilot site to an operational integrated system at a second facility, establishing repeatability and refining the commercial model.

The founder has 12 years of experience as a process engineer at a major chemical company, including multiple years in operations and management of change roles. He has deep relationships across the industry and is already embedded within a network of plant operators and engineering contractors. Steel Atlas has committed to placing an advisor with nuclear and accelerated plant turnaround experience to guide buildout of the customer success model and help shape a repeatable enterprise playbook.

AI-powered equipment financing and logistics for industrial America

Highlight: Application volume grew 3,900% from November launch ($35K) to $1.4M in January; graduated from pilot to full e-commerce integration with first design partner.

Next Key Milestone: Begin lending from own balance sheet by April to build loan track record ahead of Q3 debt facility raise.

Next Expected Round: Q3 2026

Substrate Industries accelerates equipment OEMs' sales by offering a white-label buy-now-pay-later system. Substrate approves ~95% of customers for 3-72 month terms in <1 day and pays vendors 100% upfront. Setup takes just 20 minutes. Today, only giants like Caterpillar and Haas offer in-house financing. This unlocks 20-30% more sales and 4-8x faster close rates. By underwriting at the machine level (not just the borrower level) and wiring funds to vendors in days, Substrate eliminates weeks-long cycles, opaque fees, and high decline rates that plague the $1.3T US equipment-finance industry.

Substrate's first two months of live operations validated the core product loop while surfacing the operational complexity that will define its moat. The company went from first application in November to processing $1.4M in credit opportunity value by January, a trajectory shaped by deliberate sequencing: prove the integration model with a single design partner, expose every workflow gap, then scale.

Substrate went live in November with a limited pilot on Boom & Bucket, a Ritchie Bros-owned marketplace for heavy equipment (the world's largest auctioneer and marketplace for used heavy equipment, trucks, and industrial assets). The first financed transaction was a skid steer purchased by an off-grid North Carolina farm. Processing these initial applications manually exposed dozens of lender-specific edge cases (land deed requirements, unusual corporate ownership structures, bespoke document collection rules) that the team spent November and December encoding into software. This abstraction layer, translating heterogeneous lender requirements into a single API, is the core of Substrate's technical defensibility.

By late January, Substrate graduated from the manual pilot to a full e-commerce integration on Boom & Bucket's site, capturing 100% of the marketplace's financing volume. The company simultaneously onboarded six additional vendors: Garage, Revelation Machinery, Lucid Robotics, Grizzly, Unicorn Bio, and Flyby Robotics. The equipment network now spans ambulances, excavators, AI-powered bulldozers, drones, and cell culture benchtops, demonstrating the cross-category flexibility central to Substrate's underwriting thesis.

| Metric | Nov 2025 | Dec 2025 | Jan 2026 |

|---|---|---|---|

| Applications | 1 | 8 | 25 |

| Credit Opportunity Value | $35,000 | $330,036 | $1,338,850 |

The company doubled its headcount since December. Logan Murphy joined as Head of Operations, bringing direct experience as Senior Director at Ritchie Bros and CRO/first hire at Currency, a $100M+ annual revenue equipment finance lender at peak. The engineering team added Nikhil Kamath and Nathan Tablang as founding engineers, and Abby Healy joined to lead customer success and operations. Earlier in the quarter, Substrate hired the engineer who owned SpaceX's Starlink payments ledger and brought on Chris Geoffroy (ex-Ramp, Atalaya) as Head of Finance and Capital Markets. The fact that Substrate beat offers from OpenAI and multiple hot Series A/B companies at this stage is a strong signal on founder pull.

Substrate is on track to raise its debt facility by Q3. In December and January, the company designed its loan servicing architecture, selecting providers and integrating directly with JPMorgan Chase while building most infrastructure in-house. The target is to lend a few hundred thousand dollars from its own balance sheet by early April to build a loan track record and stress-test servicing infrastructure ahead of the facility raise.

Two workstreams are underway: completing state-by-state lending and broker licensing assessments with Scale (the company's loan platform legal partner), and finishing the Portfolio Servicing MVP, which includes opening bank accounts with JPM, establishing the required legal entities, and building the ledger and payment rails. This vertical integration, from origination through servicing, is where Substrate's long-term margin structure lives.

Substrate's near-term needs center on three areas: talent, customers, and market access.

Engineering. The team is hiring two roles: a senior engineer with experience building underwriting, lending, or fintech systems at scale, and a junior full-stack engineer with strong design and product instincts. Both roles are critical to re-architecting the admin dashboard and shipping the servicing MVP on time.

Head of Risk. As the company approaches its Q3 debt facility raise, it is actively searching for a Founding Head of Risk with 15+ years of experience, someone who has directly managed multi-billion-dollar SMB or secured consumer loan portfolios, wants to build a credit function from scratch, and has defended credit decisions to investment committees. Introductions appreciated.

Customer introductions. Substrate's ideal vendors are businesses that sell equipment or build software for equipment sellers and buyers (quoting tools, procurement platforms, ERPs, rental software). If you know operators in these categories, Substrate can help them grow sales and open a new revenue stream through embedded financing.

Trade shows and associations. The team is looking for relevant industry conferences and trade associations to get in front of equipment sellers. Recommendations welcome.

Automated knitwear manufacturing for America

Highlight: Bloomingdale's partnership secured with ~$200K/month in projected revenue.

Next Key Milestone: Achieve fully autonomous 24/7 production by July 1, 2026.

Next Expected Round: $40M+ Series A by end of summer 2026.

Framework Automation is building America's next great industrial company, reshaping today's $260B knitwear market with a software-defined manufacturing platform that fully automates production. Their platform eliminates inventory and supply chain risk while achieving cost parity with Asia today. The US currently produces most of the world's cotton and polyester. But these raw materials are shipped abroad and made into clothing due to lower labor costs. Using 3D-knitting, Framework is eliminating this labor arbitrage to bring on-demand clothing manufacturing to the US.

Framework closed a $4.5M Seed extension from CRV at a $45M post-money cap SAFE (our entry was $22M). With that, Framework closed the quarter with tangible production revenue taking shape and a clear path to full factory autonomy. They are transitioning from commissioning to recurring manufacturing operations, with the LA facility now running live orders and brand partnerships converting from sampling to paid production.

Framework secured its first major brand production contract with Bloomingdale's, which is expected to enter full production within two to three months. At scale, partnership will run approximately 2,000 to 3,000 cashmere pieces per month, translating to roughly $200K in monthly revenue. Because cashmere yarn constitutes a larger share of per-unit cost, gross margins on this contract are positive but lower than the company's target mix. The Bloomingdale's relationship is primarily valuable as a foundation of annualized recurring revenue and brand validation at scale.

Alongside Bloomingdale's, Framework is running additional production volume at significantly stronger unit economics. Approximately one-third of Bloomingdale's volume is being produced for other customers at $35 per piece against an estimated $12–13 cost basis, yielding healthy gross margins that better reflect the platform's long-term economics.

The most significant operational milestone ahead is the full installation of Framework's autonomous production system by July 1. Once complete, the factory will be capable of 24/7 unattended operation across the core knitting workflow. The autonomous system encompasses AMR (autonomous mobile robot) deployment, machine servicing, and automated yarn cone swapping, eliminating human intervention from the knitting process entirely.

The only remaining manual step will be editing and finishing (sewing, treatment). Framework is addressing this by building excess finishing capacity so that a single daytime shift can process the garments accumulated overnight. This is a deliberate architectural choice: finishing capacity is significantly cheaper to scale than knitting automation, and a one-shift finishing model keeps labor costs contained while the core production loop runs continuously.

The factory layout is being reconfigured to accommodate 26 total Shima Seiki machines, up from the current 11. The machines will be rotated 90 degrees and arranged in two rows with a central robotic rail system, using Kuka robotic arms for automated material handling and servicing. Framework has already requested quotes on 15 additional machines.

Framework's relationship with Shima Seiki is evolving from customer to strategic partner. With 11 machines installed today and 15 more on order, Framework is on track to become one of the largest single-year purchasers in Shima Seiki's history. Management's near-term goal is to secure exclusive distribution rights for Shima Seiki machines in the United States for the next five years.

The rationale is straightforward: if Framework commits to a $50M+ CapEx plan over the next three years (largely debt financed, possibly with portco Substrate), exclusivity ensures that no domestic competitor can replicate the production infrastructure. Management expects this agreement to be in place before the Series A fundraise, creating a powerful competitive moat to present to investors.

Longer term, Framework is evaluating a potential acquisition of Shima Seiki. The Japanese company's enterprise value has fallen below $200M and trades at roughly 0.4x book value, with cash and land alone worth more than the market capitalization. The family that founded the company retains approximately 17% ownership and maintains control as the largest block. Framework is building a direct relationship with the family, including an in-person visit planned for March. The acquisition path would likely involve a management buyout structure or a joint venture with a PE partner, with Framework providing the strategic rationale and operational exclusivity. We are advising on structuring this opportunity to complement the Series A process.

The lean team of just 6 (!) continues to operate at an exceptional level. Each member demonstrates deep domain expertise while contributing across multiple functions. Evan Bender, the founding manufacturing engineer, has been instrumental in driving factory buildout and was recently working until 2 AM on weekends to maintain the commissioning timeline. Sarah Choi continues to manage both operational and commercial workflows. We have no doubt this is the right team to build a massive, category defining company.

Framework is actively recruiting for a machine learning team to build the design-to-knit-instructions pipeline. Today, Framework's thesis is that the industry will shift from being inventory-constrained to being design-constrained as on-demand production scales. The next step is to remove the design constraint itself by automating the translation from generative AI design outputs into machine-executable knitting instructions. This capability would complete the full-stack vision: custom sizing, custom design, and automated production under one platform.

Management is also recruiting mechanical engineering talent with credentials from high-performance engineering environments (SpaceX, Tesla, Anduril, or equivalent). We have facilitated introductions between Framework and Steel Atlas portfolio company Autonymy's engineering team to accelerate this pipeline.

Framework is preparing a Series A raise targeted for the end of summer 2026, timed to coincide with the autonomous production system being operational for one to two months. The fundraise narrative will center on three proof points: (1) fully autonomous 24/7 manufacturing, (2) recurring brand revenue, and (3) exclusive access to Shima Seiki machines in the US.

Management is targeting $40M or more in capital. We believe the valuation should reflect the infrastructure moat and vertical integration potential, and the company may be able to command a premium given the autonomy demonstration and strategic positioning around the Shima relationship.

Investor interest is already strong. Multiple firms have proactively asked whether Framework would accelerate the timeline. Management is deliberately holding the line on timing to maximize leverage. Target investors for the lead include Thrive Capital, Founders Fund, and other top-tier multi-stage firms. We are actively facilitating introductions and hosting informal dinners to build these relationships ahead of the formal process.

Framework's long-term vision extends well beyond contract manufacturing. With autonomous production at cost parity with the lowest-cost global mills, the company is positioned to forward-integrate into direct-to-consumer and owned-brand models over a five-year horizon. The combination of custom sizing (enabled by 3D body scanning), generative AI design, and zero-waste 3D knitting creates a vertically integrated platform that no incumbent can replicate.

The immediate priorities for the coming quarter are:

Real-time supply chain intelligence for logistics, insurance, and government

Highlight: Ended FY25 at $8.9M live ARR (up from $654K), and delivered a record Q4 with $3.3M net new ARR, including a $1.45M Amazon deal.

Next Key Milestone: Hit $2.5M net new ARR for Q1 2026.

Next Expected Round: $100M+ Series C by Q1 2027.

GenLogs is the real-time intelligence layer for American freight. The company tracks every long-haul truck in the United States using proprietary sensors, satellite imagery, mobile-ad IDs, and traffic cameras to create the most comprehensive freight intelligence platform ever built. GenLogs serves brokers, shippers, carriers, insurance companies, and government entities with unmatched visibility into the $10T annual flow of goods across American highways.

GenLogs closed what was arguably the most competitive Series B in the supply chain space this year. Battery Ventures led a $60M round at a $375M valuation. In addition, of that $60M, $30M of secondary was transacted to provide liquidity for an early fund that was winding down its position. The combined structure allowed GenLogs (and its investors) to take only 8% dilution while putting $30M of primary capital on the balance sheet. Ryan ran a disciplined process: only 10 venture firms were invited to pitch on leading the round, and Battery won due to Marcus Ryu's experience building a $10B public company in insuretech (Guidewire). His vast knowledge and experience will be instrumental in building GenLogs into an even larger multibillion dollar/year business.

The round closed in record time (under 14 days). Post-close, inbound interest has been overwhelming. JLL ($15B commercial real estate firm) reached out unprompted wanting to license truck intelligence data for their industrial network strategy tools. BlackRock's North American real estate team flagged it as a gap in their portfolio. JP Morgan as well. Canadian law enforcement contacted GenLogs asking for cross-border investigative support and a pilot. The signal is that the data GenLogs is generating has applications well beyond freight brokerage, and the market is starting to figure that out.

FY25 was a defining year. The company grew ARR nearly 14x, from $654K to $8.9M, against a board plan of $8.2M. The company did all of this during the 47th month of the Great Freight Recession, the longest bear market in US trucking history. Q4 alone added $3.34M of net new ARR, 81% from 21 new logos, 19% from 11 expansions. Enterprise ACV rose to $250K and NRR finished the year at 135%.

The competitive contrast is stark. Roper Technologies (parent of DAT Freight & Analytics) reported its Network Software segment grew only 2.5% for the full year. Greenscreens.ai, acquired by Triumph for $160M at $8M ARR (a 20x multiple), has been rebranded as Triumph Intelligence and has been flat since acquisition: ACVs fell from $43K to $39K in Q4, and NRR reverted to 96%. While Triumph Intelligence was flat in Q4, GenLogs added $2.7M of new revenue. There are no excuses entering 2026.

The headline deal was Amazon at $1.45M, GenLogs' first seven-figure contract, closed through early executive sponsorship and disciplined value selling tied to Amazon's acute legal exposure on freight accidents and theft. JB Hunt expanded from $400K to $700K. CH Robinson from $400K to $500K. Walmart, signed in September, was already upsold twice by year-end. GEICO closed at the end of January as the fifth-largest customer by ARR. RXO is expected to close in February at $450-550K. GenLogs now counts 80+ paying customers across five verticals and has five of the top ten US freight brokerages on contract: CH Robinson, JB Hunt, Uber/Echo, Schneider, and soon RXO.

On the P&L side, Q4 landed largely on plan. COGs came in below forecast due to lower maintenance and travel costs. The company implemented several accounting improvements flagged during Series B diligence, including spreading lease expense over term (vs. as-paid) and taking depreciation expense for the first time. All key SaaS efficiency metrics (ARR per headcount, burn multiple, magic number) came in better than plan, driven by top-line outperformance.

One data point worth highlighting: CH Robinson reported that their critical incident rate fell 85% in the year after deploying GenLogs. Their carrier sourcing team told Alex Birmingham directly that they use GenLogs every day, have stopped 15 thefts using the platform, and routinely recommend it to peers. CH Robinson and JB Hunt (both GenLogs customers) have outperformed RXO and Landstar (non-customers) in stock performance over the trailing twelve months. That correlation is becoming a selling point in C-suite conversations.

GenLogs has deliberately diversified its customer base across five verticals: logistics/freight brokerage, insurance, shippers, government, and emerging use cases. The enterprise sales team has grown from 3 to 12 AEs, and the company has established specialized customer success operations for each segment.

Freight Brokerage: GenLogs is the de-facto intelligence layer for brokers, helping them match available trucks to loads in real-time. The company is displacing legacy solutions from Highway and others by offering richer data, faster updates, and integrated fraud detection. Several brokers report that GenLogs is now central to their daily operations and competitive differentiation.

Insurance & Risk Management: InsurTech partnerships are maturing. GenLogs is working with Travelers and other carriers to build data-driven underwriting models and post-loss investigation workflows. Early results show that GenLogs data can reduce fraud detection investigation time by 40%+ and help carriers price risk more accurately. This vertical is expected to become a major revenue driver in 2026.

Shippers & Logistics Providers: Large shippers (3PLs, food & beverage companies, retailers) are using GenLogs to monitor their supply chains in real-time, detect disruptions early, and optimize routing. One major shipper partner stopped 15 thefts using GenLogs during 2025, justifying a multi-year contract. Deployment at this tier is typically 6–12 months long, but lock-in is strong once operational.

Government & Public Sector: The USDOT pilot expanded from a $25K POC to a $250K paid contract. GenLogs is now the primary data provider for federal freight intelligence initiatives. Three state agencies and two local law enforcement departments are in paid pilots or contracts totaling $75K+ annually. The government pipeline has grown to $5M+ in qualified opportunities over the next 18 months, representing a greenfield expansion of the company's addressable market.

GenLogs is moving beyond a freight-tracking platform to a full-stack supply-chain intelligence engine:

Carrier Compliance Suite: This product consolidates fraud detection, compliance verification (safety ratings, licensing, etc.), and historical performance data. The suite is designed to replace legacy systems like Highway with a superior all-in-one solution. Early feedback from beta customers is strong, and the company expects formal launch in Q1 2026.

Computer Vision & Fleet Analytics: GenLogs is applying deep learning to its historical archive of 2B+ images to extract fleet age, maintenance condition, and behavioral patterns. These models enable new insights for insurers, equipment suppliers, and lending partners. The company is already selling specialized reports to heavy-duty parts distributors and truck refinancers.

Market Expansion: The GenLogs TAM is far larger than just freight brokers. Ports, railroads, intermodal terminals, and warehouse operators all face similar visibility problems. GenLogs is exploring vertical-specific solutions for each, with pilots already underway at two major port authorities.

GenLogs enters 2026 as a category-defining company. The freight intelligence market has coalesced around their platform, the sensor network creates a defensible moat, and the expansion into insurance and government validation is opening new revenue streams. The company is simultaneously proving strong unit economics while maintaining 100%+ growth — a rare combination in logistics tech. With $30M in fresh capital and a clear path to profitability, GenLogs is positioned for sustained growth and eventual scale exit.

High-temperature gas reactors and advanced nuclear energy

Highlight: Raised $130M Series A led by Snowpoint Ventures with Palmer Luckey (Anduril), Shyam Sankar (Palantir CTO).

Next Key Milestone: Produce 100 kWt of thermal power at Ward250 in Utah by July 4, 2026.

Next Expected Round: $300M Series B by early Q2 2025.

Valar Atomics is pioneering a new path to commercial nuclear energy by combining proven High-Temperature Gas Reactor (HTGR) technology with a novel business model to enable rapid deployment and economies of scale. The company partners with national labs, government agencies, and strategic industrial customers to accelerate development of modular reactor systems capable of delivering both electricity and process heat at scale.

Valar closed a historic $130M Series A in Q4 2025, led by Snowpoint Ventures (founded by former Palantir executives). This is the largest Series A for a nuclear company in history. For context, Steel Atlas invested $1.25M in Valar roughly one year earlier at a $30M post-money valuation, securing a 5x+ markup reflecting the company's trajectory before federal policy began to price the opportunity. The Series A values Valar at $500M+ post-money, reflecting validation from a top-tier investor and the deepening conviction across the venture and strategic communities that Valar has solved the key technical and regulatory barriers to commercial nuclear deployment.

Valar Atomics achieved a historic milestone in November 2025: the company became the first startup in history to achieve nuclear criticality. The Nova Core prototype reached zero-power critical at Los Alamos National Laboratory, marking the first privately-developed advanced reactor to demonstrate controlled nuclear fission. This achievement validates the core physics of Valar's design and unlocks the pathway to operational deployment.

The Department of Energy named Valar one of 11 companies selected for the Advanced Reactor Pilot Program, an accelerated pathway designed to achieve demonstration of advanced reactors outside traditional NRC licensing. This program, backed by Executive Order 14301, aims to have selected reactors at criticality by July 4, 2026. Valar has committed to meeting this timeline and is on track to do so. Secretary of Energy Chris Wright visited Valar's facilities in July 2025, underscoring the administration's reliance on Valar to deliver near-term progress on nuclear energy goals.

Valar was also selected for the Department of Energy's Advanced Fuel Line Pilot Program, tasked with rebuilding US capacity for TRISO fuel and high-assay low-enriched uranium (HALEU) production. This vertical integration is strategically critical: Valar can now control both the reactor hardware and the fuel supply, removing a major constraint in the nuclear supply chain. The DOE is providing cost-shared support for pilot-scale fuel production infrastructure at Valar's Utah facility.

Additionally, Valar is pursuing the US Army's Janus Program, which seeks to deploy small, transportable reactors to remote military installations by 2028. Valar's modular design aligns perfectly with the Janus specifications, positioning the company for significant defense revenue in parallel with civilian markets.

Valar broke ground in late Q3 2025 on its San Rafael Energy Research Center in Emery County, Utah. The facility will host the first operational prototype of the company's modular reactor line, serving as a testing and qualification hub for future commercial deployments. The location provides access to skilled labor, existing nuclear infrastructure, and supportive state policy. Valar plans to begin construction of a high-temperature test loop by mid-2026, with the goal of achieving operational criticality at the site by end of 2026.

Valar is positioned at the intersection of energy security, climate policy, and industrial reindustrialization. The company's reactors can provide clean, reliable baseload power for data centers, industrial heat for refineries and chemical plants, and synthetic fuel production. The addressable market spans utilities, industrials, and government — easily a $100B+ opportunity over the next decade. With $130M in capital, a clear technical path to commercialization, and strong government backing, Valar is positioned to become one of the defining energy companies of the next generation.

Orbital debris detection enabling satellite insurance

Highlight: Completed US TopCo flip, with Nano Sensors entering production for 2026 launch.

Next Key Milestone: Sign Starcloud Heads of Terms and execute first Lloyd's of London insurance policy (targeted Q1 2026).

Next Expected Round: Series A in Q2 2026.

ODIN Space solves the exponentially growing threat of orbital debris, where untrackable materials travel at 10x rifle speeds destroying billion-dollar satellites. With proprietary Nano Sensors developed by CEO Dr. James New during his tenure at NASA, ODIN detects previously invisible sub-centimeter debris. In partnership with Lloyd's of London, ODIN's sensors are enabling the first data-driven satellite insurance products that are 10–100x cheaper than current alternatives. With only 3–5% of satellites insured today, ODIN is unlocking mass-market satellite insurance, representing a $10B+ annual revenue opportunity by 2030.

ODIN's commercial momentum accelerated meaningfully in Q4, with the first commercial agreement finalized with Arkisys, a satellite operator deploying a multi-satellite constellation. The contract structure is: $50,000 per satellite for hardware (with 50% upfront, 50% on delivery) and $30,000 annually per satellite for data services. Estimated build cost is $25,000 per unit, yielding positive working capital and healthy gross margins from day one.

On the government side, ODIN finalized a €230,000 contract with the European Space Agency (ESA) to design and test XL Sensor panels. Upon successful completion, ESA has outlined an automatic follow-on phase valued at €2M for a dedicated CubeSat mission. The combined Arkisys and ESA contracts represent nearly $500K in committed revenue — the company's first tangible proof of commercial demand.

The Nano Sensor underwent significant miniaturization during Q4, achieving a thickness of under 3mm with a self-adhesive backing, enabling "peel-and-stick" integration onto satellite panels. The new design reduces mass, simplifies installation, and demonstrates that orbital debris sensing can become a non-intrusive standard component. Demonstrations at the SmallSat conference validated demand: multiple operators immediately requested sample units for integration on existing satellites.

ODIN's newly contracted systems engineer (formerly with NASA, ESA, and UK Ministry of Defence) is developing standardized integration documentation for satellite OEMs. This initiative aims to eliminate friction in component adoption and provide pre-approved mechanical, electrical, and data interface specifications. The engineer is also designing a benchtop verification rig for pre-launch testing, strengthening ODIN's reputation as a reliable subsystem partner.

ODIN completed incorporation of ODIN Space Inc. in Delaware, with registration in Orange County, California. This US entity is critical for government and defense contracts. The company is pursuing SAM.gov registration and CAGE code assignment to qualify for federal procurement. ODIN has brought in advisor Rob Zitz, a former senior US intelligence official, to facilitate defense introductions.

On the team front, ODIN appointed Steve Young, President of Satellite Missions at ICEYE, as Senior Board Advisor. Young's track record scaling ICEYE provides deep government and commercial network access. ODIN is also recruiting a VP of Sales with established relationships across satellite operators and insurers, with target hire by year-end 2025.

ODIN continues coordination with Willis Towers Watson (WTW) to structure new "collision-only" satellite insurance policies leveraging ODIN data. This model, validated with major underwriters, is designed to re-open the stagnant space insurance market by offering affordable, named-peril coverage. The Arkisys and ESA contracts provide the real-world validation data necessary for underwriting these new products, and ODIN expects the first insurance products to launch in H1 2026.

ODIN enters 2026 with the strongest commercial and technical positioning of its history. Contracted revenue from Arkisys and ESA, coupled with early government interest from the US defense community, demonstrates that orbital debris detection has moved from academic interest to commercial necessity. With strong cash runway exceeding 18 months and clear path to Series A, ODIN is positioned to scale deployment of its sensors across the global satellite fleet and establish itself as the de-facto standard for orbital safety and insurance underwriting.

Accelerator-driven systems for nuclear fuel and medical isotopes

Highlight: Pharma giant Bayer submitted a draft LOI for 100,000+ dose/year Ac-225 supply agreement; NNSA clearance obtained, unlocking LANL technical review for March 2026.

Next Key Milestone: Secure written pharma commitments (Bayer, BWXT Medical) and complete LANL three-day technical evaluation in March.

Next Expected Round: $105M Series B led by Guggenheim Partners (targeting Q2 2026)

Transmutex, founded in 2019 in Geneva, is reinventing nuclear energy for a safer, cleaner future. The company is building first-commercially-viable, ultra-high-power accelerator-driven systems (ADS) for breeding domestic fuel, transmuting radioactive waste, and producing advanced medical radioisotopes. Unlike traditional fission reactors, Transmutex's systems can use multiple fuel types (including thorium) by harnessing a particle accelerator to drive a safer, non-self-sustaining reaction.

Transmutex achieved a historic breakthrough in Q4 2025: the company's AI-operated cyclotron control system at the Paul Scherrer Institute reached zero-power critical — the first time machine learning feedback control has been applied to full-scale high-energy accelerator systems. The AI system surpassed expert human performance within four days, setting accuracy standards that would take human operators weeks to establish. This demonstration validates Transmutex's core thesis: that AI-driven accelerator optimization can make systems safer, more efficient, and more reliable than manual operation.

In parallel, the fuel-fabrication team successfully produced and sintered the first thorium fuel pellet after an eight-month delay caused by customs export reviews. The pellet demonstrated full structural integrity under reactor-relevant conditions and will serve as the prototype for upcoming irradiation tests. For Indian stakeholders, this proof is critical to validating domestic thorium fuel production.

The cleanup of a contaminated hot cell at PSI was completed in one week versus PSI management's one-year estimate, unlocking additional hot cells at minimal cost. This operational capability has attracted interest from URENCO, which lacks hot-cell capacity and is exploring shared research infrastructure with Transmutex.

URENCO, Europe's uranium enrichment consortium, evolved its partnership with Transmutex into multiple workstreams. The company commissioned a €25,000 feasibility study analyzing hybrid fuel combinations and has opened discussions on AI optimization of centrifuge operations. URENCO has also agreed to help secure HALEU supply for Transmutex's future START reactor.

TÜV NORD, Germany's premier nuclear safety authority, requested a case study demonstrating how Transmutex's AI models could accelerate and standardize safety-case evaluations. Early results matched human expert conclusions, establishing a strong basis for extended cooperation and creating a potential pathway for regulatory acceleration.

The most unexpected breakthrough was the medical-isotope initiative. Transmutex signed an MOU with CHUV Hospital (Lausanne, ranked 15th globally) to co-develop Terbium-149 production using accelerators. The isotope, proven in mice to destroy up to 40% of cancer types, was previously producible only at CERN. CHUV leadership provided formal letters of support and outlined plans for an isotope-production facility by 2028–2029. The economics mirror the trajectory of Novartis's Lutetium-177 (now a multi-billion-dollar platform), suggesting Terbium-149 could become a similarly transformative therapy. PSI has secured 50M CHF in federal grants for isotope research, creating a shared development pathway.

Germany: Transmutex achieved formal approvals from the RWE board (Germany's largest utility) and the mayor of Gundremmingen to sign an MOU for site access and collaboration. RWE committed ~€50M in cost share via infrastructure, grid access, and site use. The district manager's resistance to "nuclear-waste language" due to local political sensitivities led Transmutex to reframe the initial MOU around medical applications, with federal-level engagement to secure support. The company submitted a memo to Germany's SPRIN-D innovation agency proposing a research program on waste transmutation, targeting federal selection by year-end 2025.

India: Progress has been delayed by government-to-government coordination issues, but Transmutex is engaging India's largest utility directly — a 70-GW predominantly coal-based enterprise that recently created a nuclear engineering division focused on thorium reactors. This industrial entry point bypasses diplomatic formalities and aligns with India's long-standing thorium ambitions. The company expects a productive India engagement in Q1 2026.

United States: Following NDA execution with Los Alamos, Transmutex transmitted its full technical dossier to Los Alamos and Argonne for review. Argonne formally endorsed the fuel-cycle and recycling modules. Security clearances are pending, which will unlock in-person technical collaboration.

Transmutex is raising a $105M Series B with Guggenheim Partners advising. The proceed will fund construction of the German facility, completion of the medical-cyclotron site, and advancement of the full-scale START reactor program. The company is entering its most consequential 90-day stretch, with major technical milestones, government partnerships, and fundraising converging simultaneously. Success across these fronts would establish Transmutex as the global leader in advanced nuclear and isotope production, with a viable path to multi-billion-dollar value creation.

Potassium-ion batteries for critical-mineral-free energy storage

Highlight: MOU signed with Michigan Potash (MPSC), developer of the US' largest potash and salt production facility (backed by $1.26B DOE-LPO).

Next Key Milestone: Convert MPSC MOU into binding terms (LOI target: January) and formalize SBIR Phase 2 award ($1.25M).

Next Expected Round: Strategic Bridge or M&A

Group1 is commercializing potassium-ion batteries (KIBs), a critical-mineral-free alternative to lithium-ion. Unlike LIBs which rely on scarce lithium, cobalt, and nickel sourced from geopolitically unstable regions, KIBs use abundant potassium with "drop-in" compatibility to existing manufacturing infrastructure. The technology addresses two national priorities: energy independence and critical-mineral security.

In July 2025, Group1 faced a critical liquidity crisis with only three weeks of runway remaining. A bridge financing process was launched under severe time pressure. By late July, Group1 successfully closed $750K in senior convertible notes, structured with a 2x–10x sliding return depending on exit valuation. Steel Atlas participated with a $50K+ commitment, deployed in tranches tied to operational milestones. Steel Atlas took a board seat (Cameron Porter) to provide active operational oversight.

The global battery industry entered sharp realignment in Q4 2025. Western automakers including Porsche's Cellforce and Mercedes-Benz halted next-generation battery programs. Silicon anode commercialization slipped to 2028+. Meanwhile, China restricted exports of LFP (lithium iron phosphate) cathode materials to the US, effectively cutting off the world's most mature and cost-efficient lithium battery chemistry from American supply chains. This policy shift validated Group1's pursuit of potassium-ion as a domestic, critical-mineral-free alternative. Group1 is now the leading American company pursuing potassium-ion at scale, offering a fully domestic, lithium-free alternative with clear strategic value for national resilience and defense applications.

Group1 was formally invited to join the Department of Energy's Energy Storage Research Alliance (ESRA), the flagship "Beyond Lithium" roadmap initiative led by Dr. Shirley Meng. This inclusion places Group1 within a select cohort shaping the next decade of US energy storage research and policy direction. The company is near-certain to receive a $1.25M SBIR Phase 2 award, supporting 18 months of continued development alongside the University of Texas at Austin and Stony Brook University.

On the industrial side, Group1 secured letters of support from Schneider Electric, Orbia, and Cabot — three global materials and infrastructure players. The partnership with Schneider Electric is deepening, centered on high-density battery backup systems for data centers and industrial UPS deployments.

Through our board seat, Steel Atlas is taking an active operational role in Group1. Our priorities are: (1) advancing commercial engagements with Schneider Electric and other strategic partners, and (2) running a managed M&A process to provide an alternative to Series A financing if near-term commercial milestones are not achieved. Given Group1's technical achievements and strategic positioning in critical minerals, the company is an attractive acquisition target for players throughout the value chain — from American potassium producers to UPS system developers for data centers. With $1.25M in government funding and strong industrial partnerships, Group1 is positioned for significant upside, whether through venture growth or strategic acquisition.

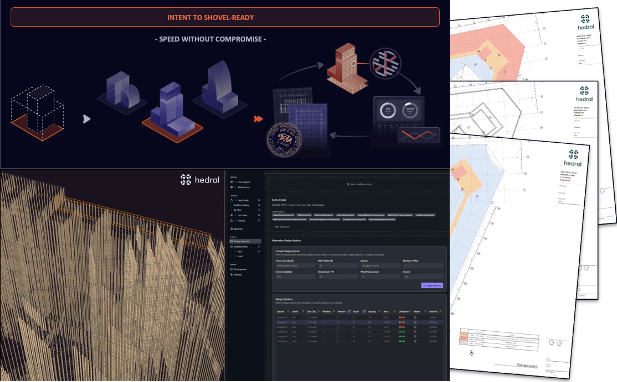

AI structural engineering for faster, cheaper, greener construction

Highlight: Tripled bookings YoY to ~$4M; secured 7-figure Navy contract earning $50-60K/mo with 8-figure vehicle in preparation.

Next Key Milestone: Acquire legacy structural engineering firms to grow bookings.

Next Expected Round: $20M Series A by Q1 2026.

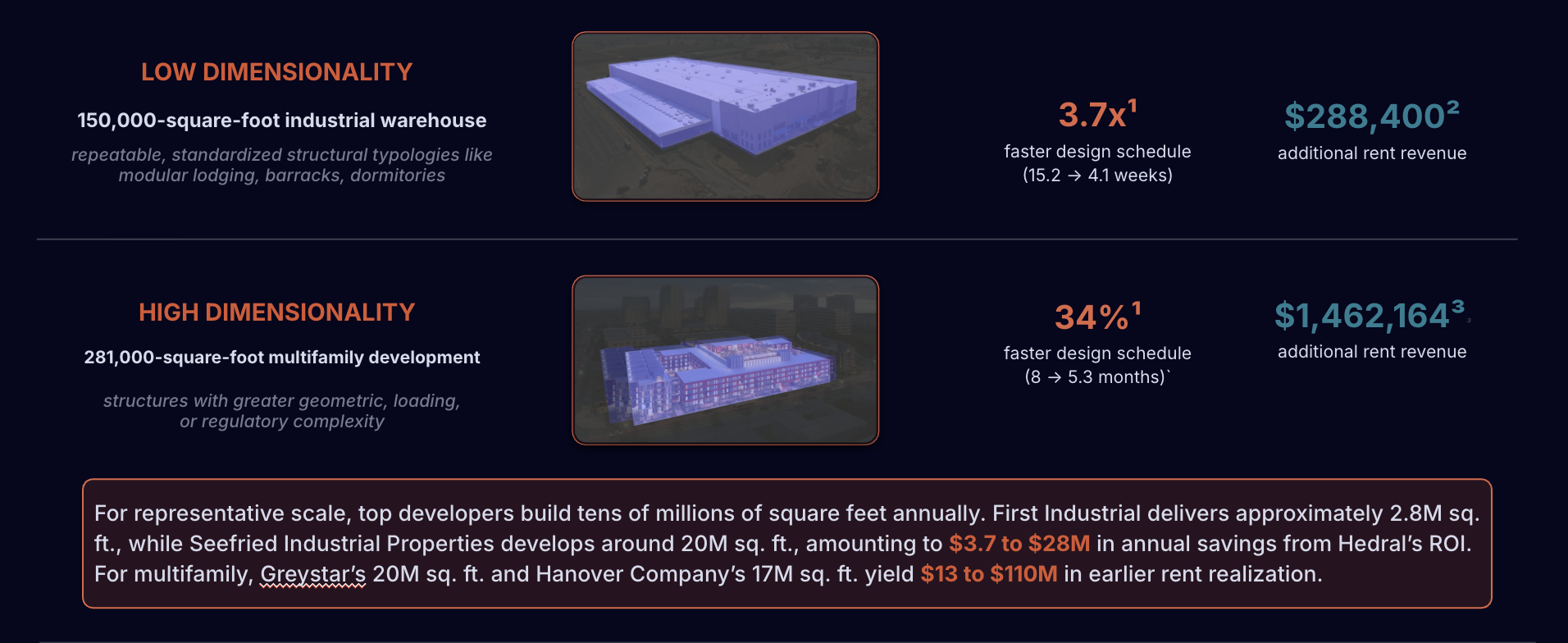

Hedral is an AI structural engineering firm based in New York that enables real estate developers to build faster, cheaper, and with lower environmental impact. Hedral automates the creation of stamped drawings and 3D building models, delivering designs 10x faster than legacy firms. The company is automating the multi-hundred-billion-dollar market for construction design and engineering, starting with structural analysis and positioning for full stack buildout.

Hedral achieved $2M+ in annual revenue run-rate at Q4 2025, with $4M+ in bookings representing strong contract commitments for 2026. The company completed its first industrial project in Texas, which has now generated repeat customer engagements and referrals. Hedral is now the "engineer of record" for over 2M square feet of federal infrastructure projects (Navy and Air Force), demonstrating credibility within high-stakes, high-precision environments where Hedral's automation excels.

Hedral took a decisive step toward internationalization in Q4, with the leadership team conducting an extensive MENA market visit. The trip centered on Egypt and Saudi Arabia, aligning with Hedral's strategy to embed itself within regions undertaking massive infrastructure modernization. Hedral met with Orascom Construction Industries (Egypt's largest construction company) to explore partnership. In Saudi Arabia, Hedral opened early dialogues with Aramco, focusing on upcoming infrastructure and federal projects tied to Vision 2030.

A key initiative has been reactivating engagement with Nesma Partners, one of Saudi Arabia's leading construction and development firms. Under the leadership of new hire Urszula Solarz, Hedral is scoping a proof-of-concept deployment to demonstrate Hedral's full-stack design-to-construction optimization workflow. Success would establish Hedral as a technical partner for large-scale, mixed-use and industrial development projects across the Kingdom.

Hedral's active portfolio now spans multifamily residential developments, industrial facilities, and mixed-use projects across California, Texas, and New York. Notably, the company has deepened its role in advanced energy and nuclear projects, signing design contracts with Aalo Atomics and executing an MOU for EPC collaboration with Steel Atlas portfolio company Transmutex. This positions Hedral within the emerging ecosystem of modular and advanced reactor construction.

Hedral continues to operate as a lean, interdisciplinary team bridging classical engineering practice and advanced computation. The team includes licensed engineers and computational specialists from world-class firms such as Foster + Partners, Zaha Hadid Architects, Grimshaw, HOK, AECOM, Thornton Tomasetti, Autodesk, and Amazon. This hybrid composition remains a central differentiator, allowing Hedral to merge design fidelity with automation-grade scalability.

Following a period of quiet execution, Hedral remains on track for a public out-of-stealth announcement in Q1 2026 timed with a Series A close. The team is developing case studies, visual collateral, and marketing materials in preparation for external visibility, particularly aligned with MENA expansion efforts and federal project milestones. Hedral's long-term positioning centers on becoming the digital backbone of next-generation engineering delivery: an intelligent geometry and coordination layer that replaces traditional, manual project management with algorithmic precision. With a growing portfolio of high-stakes infrastructure projects, strategic partnerships in both the US and MENA, and engineer-of-record authority, Hedral is approaching a phase of validated scale and global recognition.